Is homeownership worth it ?how to prepare for it ?

Let’s get one thing straight: the “American Dream” narrative is a marketing masterpiece. We’re told that buying a house is the finish line of adulthood, a golden ticket to stability, and a foolproof way to get rich. But if you’ve ever sat in a basement at 2:00 AM while a pipe mimics a geyser, you know that homeownership isn’t a dream—it’s a job.

Is it worth it? Absolutely. But only if you stop treating it like a milestone and start treating it like a tactical financial maneuver. If you walk into this without a map, the “hidden” costs won’t just surprise you; they’ll bankrupt you. Here’s the real talk on how the process actually works and how to survive it with your sanity intact.

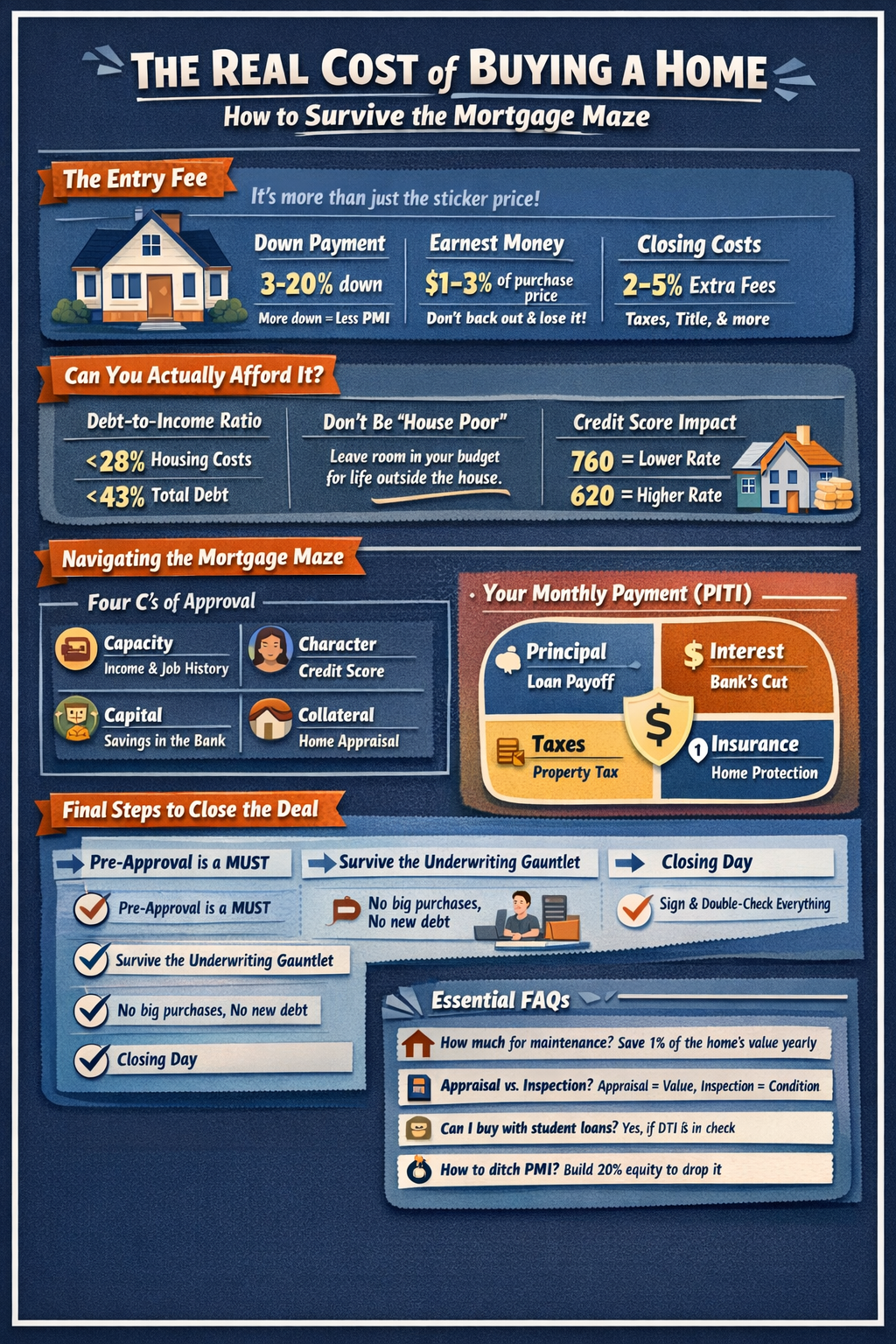

The “Entry Fee”: What You’ll Pay Just to Get the Keys

Most people fixate on the sticker price of the house. They see “$400,000” and think that’s their number. It isn’t. The cash you need to move your boxes through the front door goes way beyond that big number.

The Down Payment Myth

You’ve heard you need 20% down. If you have it, great—you’ll skip the Private Mortgage Insurance (PMI) and your monthly bill will look a lot sexier. But for most of us, 20% of a modern home price is a mountain of cash. You can get in with as little as 3% (Conventional) or 3.5% (FHA). Just don’t forget: the less you put down, the more you pay the bank in interest every month. You’re trading upfront cash for long-term debt.

Earnest Money: The “Skin in the Game”

Think of this as your “I’m not a window shopper” deposit. When a seller accepts your offer, you hand over 1% to 3% of the purchase price. This money sits in a safe account (escrow) and eventually pays for your closing costs. If you get cold feet and back out for no reason? The seller keeps it. It’s the ultimate “don’t waste my time” fee.

The Five-Percent Surprise (Closing Costs)

Closing costs are the silent killers of home deals. We’re talking taxes, title fees, attorney costs, and appraisal fees. These usually add another 2% to 5% to your bill. On a $400k house, that’s $20,000 you didn’t think you needed. If you aren’t ready for this, your deal will fall apart on the one-yard line.

Can You Actually Afford It? (Beyond the Bank’s Math)

Banks are in the business of lending money. They use formulas to decide what they can lend you, but they don’t care if you have enough left over for groceries or your Netflix subscription.

The Ratios that Rule Your Life

Lenders look at your Debt-to-Income (DTI) ratio. Ideally, they want your house payment to stay under 28% of your gross pay. When you add in your car, your student loans, and that credit card you used for the Taylor Swift tickets, they want your total debt under 43%.

Don’t Be “House Poor”

This is a trap. Just because a lender says you’re approved for a $600k mortgage doesn’t mean you should take it. If your mortgage eats up every spare cent you have, you won’t own the house—the house will own you. Leave room for a life outside those four walls.

Your Credit Score is a Price Tag

Your score isn’t just a grade; it’s a direct reflection of how much your life will cost. A 760 score vs. a 620 score can be the difference between a 6% interest rate and an 8% rate. Over 30 years, that’s hundreds of thousands of dollars. Before you browse Axcessrent, fix your credit.

Navigating the Mortgage Maze

At its core, a mortgage is a simple trade: the bank buys the house for you, and you pay them back with interest. If you stop paying, they take the collateral—your house.

Lenders judge you on the Four C’s:

- Capacity: Do you have a steady job and a history of making money?

- Character: What’s your credit history look like? Do you pay people back?

- Capital: Do you have enough cash in the bank to handle a rainy day?

- Collateral: Is the house actually worth what you’re paying? (The Appraisal).

Pick Your Poison: Loan Types

- Fixed-Rate: Your payment stays the same for 15 or 30 years. It’s boring, predictable, and the safest bet for most people.

- FHA: Perfect for folks with “okay” credit or small down payments.

- VA: If you’ve served in the military, this is your best friend. Zero money down and better rates.

The Monthly Bill: More Than Just a Mortgage

People forget that the bank isn’t the only person you’re paying. Your monthly check is a four-part harmony called PITI:

- Principal: Paying off the loan.

- Interest: The bank’s cut.

- Taxes: Your local government’s share.

- Insurance: Protecting the structure.

Pro-Tip: Don’t fall for the “Interest Rate” marketing. Always look at the APR. The interest rate is just the cost of the money; the APR includes the lender’s fees. It’s the “all-in” price of the loan.

The Final Stretch: How to Cross the Finish Line

- Pre-Approval is Non-Negotiable: If you don’t have a pre-approval letter, you’re just a tourist. Sellers won’t even look at your offer.

- The Underwriting Gauntlet: This is the most stressful part. A human (the underwriter) digs through your bank statements to make sure you aren’t a fraud. Do not buy a car, a couch, or even a fancy coffee machine on credit during this phase. 3. Closing Day: You’ll sign more papers than you ever thought possible. Check your Closing Disclosure (CD) three days before. If the numbers don’t match your original estimate, ask why.

Is it Worth It? The Verdict

Homeownership is a long game. It’s one of the few ways regular people can build massive wealth over time. But it’s only a “dream” if you respect the math. Budget for the reality, not the fantasy.

Frequently Asked Questions (FAQ)

Should I wait for interest rates to drop before buying?

You can’t time the market. If you find a house you love and the payment fits your budget, buy it. You can always refinance later if rates drop, but you can’t go back and buy today’s house at yesterday’s price.

How much should I save for maintenance?

Expect the unexpected. A good rule of thumb is the 1% rule: save 1% of your home’s value every year for repairs. If your home is worth $300k, set aside $3,000 a year. Trust me, the HVAC system knows exactly when your bank account is low.

What’s the difference between an appraisal and an inspection?

An appraisal is for the bank; it tells them the house is worth the money they’re lending you. An inspection is for you; it tells you the roof is leaking and the electrical panel is a fire hazard. Never, ever skip the inspection.

Can I buy a house with student loan debt?

Yes. Lenders look at your monthly payment, not the total balance. If your DTI ratios are in check and you have steady income, student loans won’t stop you from getting a mortgage.

What is PMI and how do I get rid of it?

Private Mortgage Insurance (PMI) protects the lender if you put down less than 20%. It’s a monthly fee that does nothing for you. Once your home equity hits 20% (either by paying down the loan or the house increasing in value), you can usually ask the bank to drop it.