Best Secured Credit Cards 2026: Build Credit Fast (Even with Bad Credit)

Secured credit cards are the fastest way to build or rebuild credit, requiring only a $200-$500 refundable deposit. Compare the 9 best secured cards of 2026, learn how they work, and discover which one gets you to a 680+ credit score fastest. Most users see 60-100 point increases within 12 months.

Bad credit doesn’t have to be permanent.

If you’ve been turned down for a regular credit card—or if you’re building credit from scratch—secured credit cards are your fastest path forward.

They’re not glamorous. They require upfront cash. But they work.

According to Experian’s 2025 credit data, people with secured credit cards who make consistent on-time payments see an average credit score increase of 60-100 points within the first 12 months. Some users even hit 680+ scores—enough to qualify for prime interest rates—after just 9 months of responsible use.

| Quick Answer: A secured credit card works exactly like a regular credit card, except you put down a refundable deposit ($200-$500) that becomes your credit limit. The bank holds your cash as collateral while you build credit through on-time payments. After 6-12 months of good payment history, most issuers upgrade you to an unsecured card and return your deposit. Approval is nearly guaranteed regardless of credit score. |

What You’ll Learn

- The 9 best secured credit cards of 2026 (with detailed comparisons)

- Exactly how secured cards work (5-step process from application to upgrade)

- How much and how fast secured cards build credit (real timeline data)

- Which banks offer secured cards (and which don’t)

- 5 common mistakes that destroy your credit instead of building it

- How to combine secured cards with rent reporting for 2x faster results

What Is a Secured Credit Card? (The Complete Definition)

A secured credit card is a credit card backed by your own money.

You put down a refundable security deposit—typically $200 to $500—and that becomes your credit limit. The bank or credit union holds your cash as collateral. If you don’t pay your bill, they keep it to cover what you owe.

Example: You deposit $300 with the card issuer. Your credit limit is $300. You charge $50 for groceries, then pay it back before the due date. The $300 stays locked up as collateral. Rinse and repeat.

The catch? Your money is locked up while you have the card active. But you’re building credit history the entire time.

The payoff? After 6-12 months of responsible use, most banks upgrade you to an unsecured card and return your deposit—often with a higher credit limit than you started with.

Key point: Unlike prepaid debit cards or charge cards, secured credit cards report to all three major credit bureaus (Experian, TransUnion, Equifax). This is what makes them effective credit-building tools.

Secured cards are especially important if you have a thin credit file—fewer than 5 active credit accounts. About 62 million Americans fall into this category, making it difficult to get approved for loans or good interest rates.

Secured vs. Unsecured Credit Cards: What’s the Difference?

Understanding the differences helps you know when to graduate from secured to unsecured cards:

| Feature | Secured Card | Unsecured Card |

| Deposit Required | Yes ($200-$2,500) | No |

| Who Can Get One | Anyone (even with bad credit or no credit) | Good to excellent credit (typically 670+) |

| Builds Credit | Yes (reports to all 3 bureaus) | Yes (reports to all 3 bureaus) |

| Interest Rates | Higher (20-27% APR typical) | Lower (15-24% APR for good credit) |

| Credit Limit | Equals your deposit amount | Based on creditworthiness ($1,000-$25,000+) |

| Get Deposit Back | Yes, when you close account or upgrade | N/A (no deposit required) |

| Rewards Programs | Limited (some offer 1-2% cash back) | Extensive (cash back, points, miles, bonuses) |

Bottom line: Secured cards are training wheels. Unsecured cards are the real thing. You use secured cards to prove you’re creditworthy, then graduate to unsecured cards for better terms and higher limits.

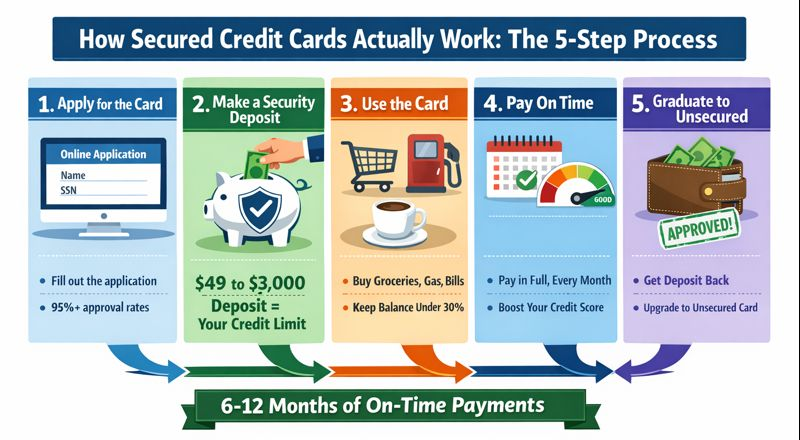

How Secured Credit Cards Actually Work: The 5-Step Process

Here’s exactly what happens from application to getting your deposit back:

Step 1: You Apply for the Card (5-10 Minutes)

Pick a secured credit card from the options below and fill out an online application. Most secured card applications take 5-10 minutes and require:

- Full name and Social Security number

- Current address (at least 6 months)

- Annual income (including part-time work, benefits, alimony)

- Employment information

- Bank account details for the security deposit

Approval odds: Nearly guaranteed. Because the bank has zero risk—they’re holding your deposit as collateral—approval rates for secured cards are 95%+, even with bad credit scores (300-550 range).

Step 2: You Make a Security Deposit

Once approved, you fund your secured account. Most cards offer flexible deposit amounts:

- Minimum: $49-$200 (depends on card)

- Maximum: $2,500-$3,000 (some cards higher)

Your deposit equals your credit limit. Deposit $500 → get $500 limit. Some cards (Capital One Platinum Secured) may give you a higher limit than your deposit based on creditworthiness.

Step 3: You Use It Like a Normal Credit Card

Once your card arrives (7-10 days), use it for everyday purchases:

- Buy gas, groceries, coffee

- Pay monthly bills (phone, utilities, subscriptions)

- Shop online or in-store

Critical rule: Keep your credit utilization under 30% of your limit. If you have a $500 limit, never carry more than $150 at any time. Lower utilization = faster credit score growth.

Step 4: You Pay Your Bill On Time Every Month

This is where credit building happens—or gets destroyed.

What helps your score:

- Paying on time (35% of your FICO score)

- Keeping balances low (30% of your score)

- Paying in full (avoids interest charges and shows responsible use)

What hurts your score:

- Missing a payment (drops your score 60-110 points)

- Maxing out the card (high utilization tanks your score)

- Only making minimum payments (racks up 20-27% APR interest)

Real example: Someone with a 520 credit score gets a secured card. They charge $100/month, pay it off in full every month. After 6 months, their score jumps to 610-640. After 12 months? 660-680.

Step 5: You Graduate to Unsecured (6-12 Months)

After 6-12 months of good payment history, most banks will automatically:

- Review your account for upgrade eligibility

- Convert your secured card to an unsecured card

- Return your security deposit (via check or statement credit)

- Sometimes increase your credit limit beyond your original deposit

Or you can close the secured card and apply for a better unsecured card elsewhere. Either way, you get your deposit back (minus any unpaid balance).

The 9 Best Secured Credit Cards of 2026 (Ranked)

Not all secured cards are created equal. Here are the best options based on fees, rewards, upgrade paths, and real user outcomes:

1. Discover it® Secured Credit Card – Best Overall

Why it’s #1: The only secured card with cash back rewards AND automatic upgrade reviews starting at 7 months.

- Deposit: $200 minimum, $2,500 maximum

- Annual fee: $0

- Rewards: 2% cash back on up to $1,000 in quarterly gas/restaurant purchases, 1% on everything else

- Welcome bonus: Cashback Match—Discover matches ALL cash back earned in year 1 (can be worth $100-$300)

- Upgrade timeline: Automatic review at 7 months, most users upgrade by month 8-9

- Credit bureaus: Reports to all three (Experian, TransUnion, Equifax)

Catch: Must fund deposit via bank account (no cash or money order). $200 minimum may be stretch for some budgets.

Bottom line: If you can afford the $200 deposit, this is the best secured card available. The Cashback Match alone makes it worth it. According to NerdWallet’s 2026 credit card analysis, Discover it® Secured consistently ranks as the #1 secured card for credit building.

2. Capital One Platinum Secured – Best for Low Deposit

- Deposit: Starting at $49, $99, or $200 (based on creditworthiness)

- Annual fee: $0

- Credit limit: $200 regardless of deposit amount

- Best for: People who can’t afford $200 upfront

5 Common Mistakes That Destroy Your Credit Instead of Building It

Even with a secured card, these mistakes can sabotage your progress:

Mistake #1: Maxing Out Your Card

Just because you have a $300 limit doesn’t mean you should use all $300. High utilization (over 30%) severely damages your score.

Better approach: Use 10-20% each month. Pay it off. Repeat. Learn more about optimal credit utilization ratios.

Mistake #2: Only Making Minimum Payments

You’ll pay interest. A lot of it. Secured cards often have 20-27% APR. On a $200 balance, that’s $40-50/year in interest.

Better approach: Pay in full every month. If you’re struggling with debt, read our guide on how to pay off credit card debt fast.

Mistake #3: Closing It Too Soon

Length of credit history matters. Close your secured card after 4 months? You lose that history.

Better approach: Keep it open for at least 12 months, even after you get an unsecured card.

Mistake #4: Not Checking Your Credit Reports

Sometimes your secured card isn’t reporting properly, or there are errors on your credit report dragging down your score.

Better approach: Check your free credit reports every 4 months. Fix any errors immediately.

Mistake #5: Ignoring Rent as a Tradeline

Most people don’t realize rent can be reported to credit bureaus. If you’re already renting, this is free credit building you’re missing. Learn more about how rent reporting works.

Credit Building Timeline: What to Expect Month by Month

Building credit with a secured card doesn’t happen overnight. Here’s the realistic timeline:

| Timeline | What Happens | Expected Score | Action Items |

| Month 1 | Application, approval, deposit made, card arrives | 520-550 (starting point) | Make 1-2 small purchases, pay in full before due date |

| Months 2-3 | First report hits credit bureaus, account shows on reports | 540-570 (+20-30 pts) | Continue on-time payments, keep utilization under 30% |

| Months 4-6 | Consistent payment history building, credit mix improving | 590-620 (+70-100 pts total) | Consider adding rent reporting to accelerate growth |

| Months 7-9 | Discover starts upgrade reviews, Capital One may increase limits | 640-660 (fair credit) | May qualify for unsecured cards or small personal loans |

| Months 10-12 | Strong payment history, likely upgraded to unsecured | 670-690 (good credit) | Qualify for competitive rates on auto loans, better credit cards |

The Bottom Line: Secured Cards Work (If You Use Them Right)

Secured credit cards aren’t glamorous. You’re literally paying to build credit.

But they work.

The formula is simple:

- Deposit $200-500

- Use the card for small purchases monthly

- Pay in full every month

- Wait 6-12 months

- Upgrade to unsecured, get deposit back

Your credit score climbs. You qualify for better cards. You get your money back.

Is it worth it? If you’ve got bad credit that needs fixing or no credit, absolutely.

But there’s an even faster way:

| Combine a Secured Card with Rent Reporting for Maximum Impact While your secured card builds one tradeline, AxcessRent adds another by reporting your rent payments to all three credit bureaus. Users who combine both strategies see 100-150 point increases in the first year—twice as fast as secured cards alone. Start Building Credit with Rent (Free) → |

Learn more about the best rent reporting services and how they compare to secured cards.