The Ultimate Guide to Creditworthiness: Boost Your Credit Fast

Introduction

In a world where financial decisions often speak louder than words, your creditworthiness tells a story one that lenders, landlords, and even employers are reading. Whether you’re applying for a credit card, seeking a home loan, or simply trying to rent an apartment, your credit profile acts like your financial résumé.

But what exactly determines creditworthiness? And how can you actively work toward building and improving it over time? Let’s dive deep into the mechanics of creditworthiness, explore the creditworthiness standards used by lenders, and discover practical steps you can take to build a strong financial foundation.

What is Creditworthiness?

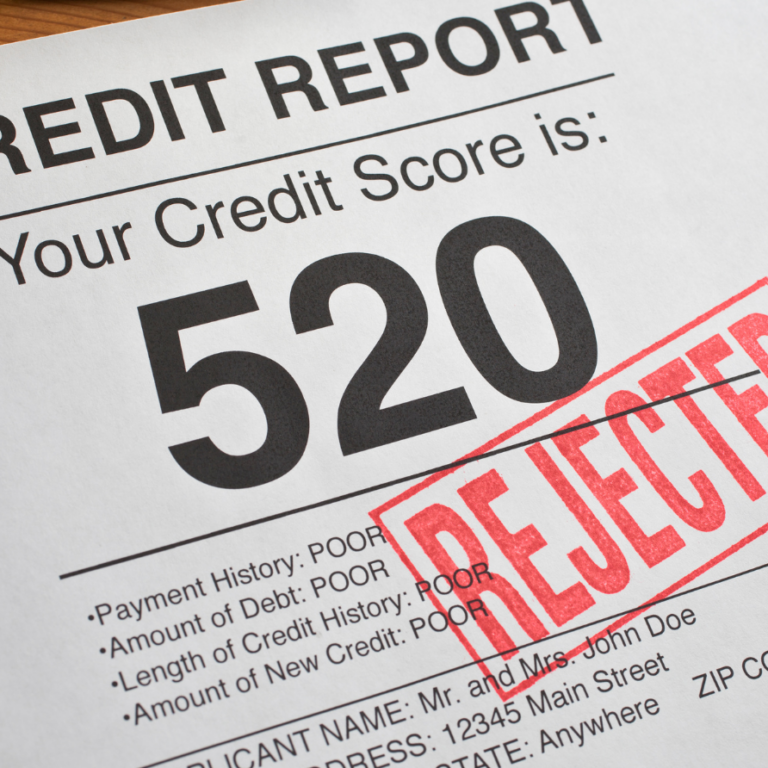

At its core, creditworthiness is an evaluation of how likely you are to repay borrowed money. It’s not just about how much money you have in the bank it’s about your financial behavior over time. Are you punctual with payments? Do you borrow responsibly? Do you have a manageable level of debt?

Think of creditworthiness as your financial character. Just as personal relationships thrive on trust, your financial life does too. Lenders, landlords, insurers, and sometimes even potential employers use your credit profile as a lens into your reliability. A high level of creditworthiness means you’re seen as a low-risk borrower, which often leads to better interest rates, easier approvals, and even more favorable terms across a variety of financial products.

In contrast, low creditworthiness can limit your options. It might mean higher interest rates, larger security deposits, or outright denials regardless of your income level. That’s why understanding and improving your creditworthiness is a crucial part of long-term financial well-being.

Why Creditworthiness Matters in the Real World

Your creditworthiness doesn’t just affect your ability to take out a loan it can influence some of the most important decisions in your life. Let’s break down a few key areas where your credit standing plays a pivotal role:

1. Loan and Credit Card Approvals

Whether it’s a mortgage, an auto loan, or a credit card application, lenders will pull your credit report to assess your level of risk. Poor creditworthiness can lead to outright denial or subprime offers with high interest rates.

2. Interest Rates and Terms

Even if you’re approved, your creditworthiness will often determine the loan terms. A strong credit profile could mean the difference between a 4% interest rate and a 12% one which adds up to thousands of dollars over the life of a loan.

3. Renting a Home or Apartment

Landlords frequently perform credit checks. If your report shows missed payments or excessive debt, they may ask for a larger deposit—or deny the rental altogether.

4. Employment Opportunities

Some industries, especially those in finance or government, conduct credit checks as part of the hiring process. A poor credit history may raise concerns about your judgment or reliability.

5. Utility and Service Deposits

If you have weak credit, utility companies might require a hefty upfront deposit to protect themselves in case of missed payments.

As you can see, your creditworthiness is like a passcode to modern financial life. The better your score and credit behavior, the easier it is to navigate the system with freedom and confidence.

How Creditworthiness is Determined: The 5 Cs of Credit

To truly understand creditworthiness standards, it’s essential to know what lenders are actually looking for when evaluating your application. These criteria are often summarized in what’s called the 5 Cs of Credit:

1. Credit History

Your credit history is the story of your borrowing and repayment behavior. It includes how long you’ve had credit accounts, your payment history, and any delinquencies or defaults. This is where your credit score comes into play—most commonly FICO or VantageScore, which ranges from 300 to 850. A score above 700 is generally considered good, but the higher, the better.

Lenders examine whether you’ve paid past debts on time, how often you’ve missed payments, and how much of your available credit you’re using. This history is often the most important factor in determining creditworthiness.

2. Capacity

Also known as debt-to-income (DTI) ratio, this measures your ability to repay debts relative to your income. If you’re earning $5,000 a month and paying $2,000 toward debt, your DTI ratio is 40%. Most lenders prefer a DTI under 36%. It’s a crucial indicator of whether you can handle more debt or if you’re already overextended.

3. Capital

Capital refers to the assets or savings you have that could be used to repay a loan. Lenders view a borrower with personal savings, investments, or a down payment as less risky. This is particularly important for large loans like mortgages or business loans. It shows you’re financially invested in the transaction and have a cushion in case of emergencies.

4. Collateral

Collateral is any asset pledged to secure a loan. In secured loans—like mortgages or auto loans—the house or car acts as collateral. If you default, the lender can seize the asset to recover their money. Collateral reduces risk for the lender and can make it easier for you to qualify even with a less-than-perfect credit score.

5. Conditions

This factor includes external elements like the purpose of the loan, the interest rate environment, and the state of the economy. For example, during a recession, even people with good credit might find it harder to qualify for loans due to stricter lending conditions.

Together, these 5 Cs offer a complete picture of your creditworthiness from multiple angles financial behavior, stability, and external risk.

How to Improve Your Creditworthiness

Building or rebuilding your credit can feel daunting but it’s entirely possible with steady effort and the right strategies. Here are proven steps to improve your creditworthiness over time:

1. Always Pay On Time

Payment history makes up about 35% of your FICO score. A single missed payment can drop your score significantly and stay on your report for up to 7 years. Set up automatic payments, calendar reminders, or use budgeting apps to make sure you never miss a due date again.

2. Keep Credit Utilization Below 30%

Credit utilization is the amount of available credit you’re currently using. If your total credit limit is $10,000, try to keep your balances below $3,000. High utilization signals risk to lenders, even if you pay off your balance in full each month.

3. Limit New Credit Applications

Every time you apply for a new loan or card, a hard inquiry appears on your credit report. Too many hard inquiries in a short time can make lenders nervous. Only apply for credit when it’s necessary, and space out your applications.

4. Check Your Credit Reports Regularly

You’re entitled to one free credit report annually from each of the three major bureaus—Equifax, Experian, and TransUnion—through axcessrent.com. Look for errors like incorrect balances, late payments you didn’t make, or accounts you don’t recognize. Dispute inaccuracies quickly—they can unfairly lower your score.

5. Start with a Secured Credit Card

If you have little or no credit history, a secured credit card is a great starting point. You’ll provide a refundable deposit (usually $200–$500), which becomes your credit limit. By making small purchases and paying on time, you build credit without much risk.

6. Become an Authorized User

Ask a trusted family member or friend with good credit to add you as an authorized user on their credit card. Their good payment history will reflect on your report—helping you build credit faster.

7. Diversify Your Credit Mix

Having different types of credit—like a credit card, auto loan, and student loan shows lenders you can handle various financial responsibilities. Just be sure to manage each responsibly.

8. Use AxcessRent to Build Credit

Most rent payments don’t impact your credit score but AxcessRent changes that by reporting your on-time rent payments to all three major credit bureaus: Experian, Equifax, and TransUnion.

How it works:

- Sign up and link your rent payments

- Rent payments are automatically reported each month

- Build credit without taking on new debt

Perfect for:

Renters with little or no credit history, or those working to rebuild their credit.

Improving your creditworthiness is a journey, not a sprint. But with consistency and patience, your financial credibility will grow stronger month by month.

How Long Does It Take to Build or Rebuild Credit?

Credit improvement is a gradual process. If you’re starting from zero, you might see positive movement in as little as 3 to 6 months. For those recovering from past mistakes like missed payments or bankruptcy, it may take 1 to 2 years or longer to significantly rebuild.

That said, the earlier you start taking control of your credit, the sooner you’ll enjoy the benefits. Keep in mind that the most important thing is not perfection, but consistency. Responsible actions, repeated over time, lead to real results.

Don’t let your largest monthly expense go unrecognized. Sign up with AxcessRent, connect your rental payments, and watch your creditworthiness grow with every on-time payment.

Final Thoughts: Take Control of Your Financial Future

Your creditworthiness is more than just a number it’s a reflection of your habits, your reliability, and your financial maturity. Whether you’re applying for a loan, renting a home, or just trying to secure a better future, understanding and improving your credit is one of the most empowering financial moves you can make.

The good news? You don’t need to be a finance expert to build excellent credit. You just need the willingness to learn, the discipline to act, and the patience to stick with it.

By following the tips outlined above, staying aware of creditworthiness standards, and staying proactive with your financial habits, you’ll not only boost your credit—you’ll unlock new opportunities for a better, more secure financial life.

Creditworthiness: Boost Your Credit Fast

Improve your credit score quickly with proven strategies. From payment history to credit utilization, we’ll show you how to optimize every factor that affects your creditworthiness.