Checking vs Savings Account: Differences in Fees, Interest, and Balances

Effective financial management hinges on using your checking and savings accounts for their distinct, intended purposes. While both accounts hold your money, one is a dynamic spending tool while the other is a static, protected growth engine.

Misunderstanding this relationship is the easiest way to lose money to unnecessary fees in your checking account, or miss out on significant earnings in your savings account. This guide clarifies the definitive roles of your financial duo and provides actionable strategies for optimal cash management.

Defining the Financial Duo

Your checking and savings accounts are the two foundational pillars of your personal finance system. They must work together seamlessly, but they must remain separate to function optimally.

The Purpose of Each Account

- Checking: The Transaction Hub A checking account provides high liquidity and is designed for daily transactional use: paying bills, using a debit card, and receiving income. Because of this convenience, it is typically subject to transactional fees and offers little to no interest.

- Savings: The Growth Engine A savings account is designed for storage and wealth building. It holds reserved funds that you do not need immediate access to. In exchange for lower liquidity and fewer transactions, the bank pays you interest, particularly through High-Yield Savings Accounts (HYSAs).

Why the Balance Matters

The key to financial mastery is ensuring the right amount of cash is in the right location:

- Avoiding fees in checking: Maintaining a specific minimum balance is often necessary to avoid monthly maintenance fees and ensures you never incur a costly Overdraft or Non-Sufficient Funds (NSF) fee.

- Maximizing interest in savings: All cash held in excess of your checking account needs should be immediately transferred to a savings account to capitalize on compounding interest and fight inflation.

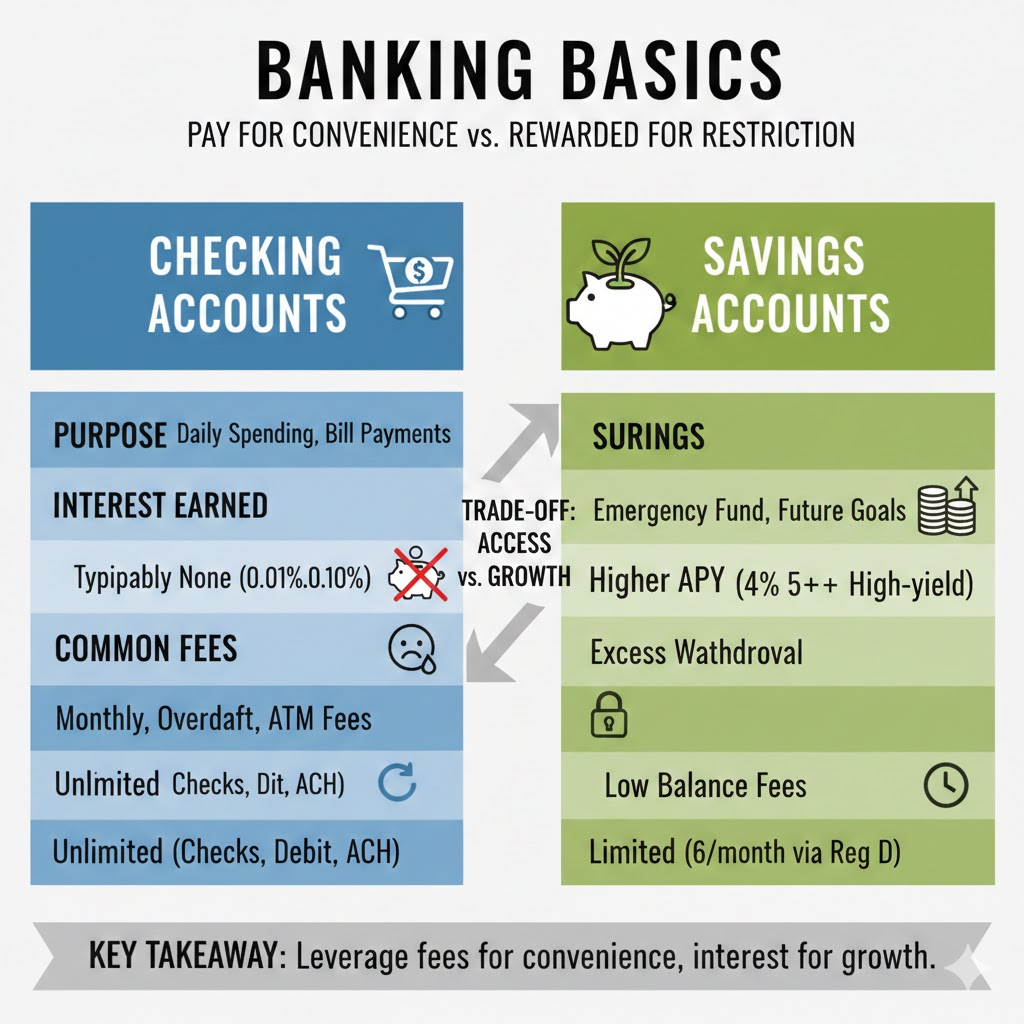

Differences Between Checking and Savings Accounts

The economic model of banking dictates that you pay for convenience and are rewarded for restriction. This is why checking accounts cost you in fees, and savings accounts reward you with interest.

| Feature | Checking Accounts | Savings Accounts |

|---|---|---|

| Purpose | Daily Spending, Bill Payments | Emergency Fund, Future Goals |

| Interest Earned | Typically None or very low (0.01% to 0.10%) | Higher APY (Often 4% to 5% + With High-yield Savings Accounts) |

| Common Fees | Monthly Maintenance, Overdraft, ATM Fees | Excess Withdrawal Fees (Regulation D limit), Low Balance Fees |

| Transactions | Unlimited Transactions (Checks, Debit, ACH) | Limited Withdrawals (Regulation D limits this to 6 transfers/withdrawals per month) |

Key Takeaway: Banks charge for the convenience and accessibility of checking (through fees) and reward the restriction of savings (through interest). Your strategy should leverage this trade-off in your favor.

Checking Strategy: The Right Amount for Daily Life

Keeping too much in your checking account is a common financial mistake, as it stagnates in a low-interest environment. Keeping too little invites costly bank fees.

How Much Do You Keep In Your Checking Account?

The ideal balance is determined by your monthly expenses plus a protective buffer. This amount ensures operational stability and fee avoidance.

The Recommended Minimum is one to two months of total living expenses that are paid out of that account.

The Buffer Rule: Add a fixed cushion to the minimum to prevent accidental overdrafts and help meet minimum balance requirements for fee waivers. A 30% cushion on top of your monthly expenses (or a fixed 200 to 500 $ buffer is highly recommended.

Optimal Checking Balance = (Monthly Expenses * 1.30) + Free Buffer

The Danger of “Bloat”: Keeping too much cash in checking—such as a large emergency fund—is known as “account bloat.” This money misses out on potential earnings in a high-yield savings account and is easily spent on impulse purchases.

How many checking accounts should I have?

For most individuals, one is sufficient for simplicity, easier reconciliation, and hitting minimum balance thresholds to avoid fees.

Reasons for Multiple Accounts (2-3 is common):

- Bill Account vs. Spending Account: Using one account for fixed bills (rent, utilities) and another for variable spending (groceries, entertainment) is an excellent, disciplined budgeting tool. This prevents you from accidentally spending money reserved for critical obligations.

- Joint vs. Individual: You might have one shared account with a partner for household expenses, plus a separate personal account for individual funds.

- Business Expenses: It is mandatory to keep a completely separate checking account for any side hustle or business finances to simplify taxes and compliance.

Savings Strategy: Building and Protecting Your Future

The savings account is where the majority of your liquid wealth should reside. Its structure encourages restricted access, allowing your money to grow securely.

How Much Do You Keep In Your Savings Account?

The core function of savings is to provide financial security:

- The Emergency Fund Goal: The top priority is building an emergency fund containing three to six months of total living expenses as an essential safety net against job loss, medical expenses, or major repairs. Some experts recommend up to 12 months for highly specialized or volatile careers.

- Beyond the Emergency Fund: Once the emergency fund is fully funded, use your savings account for short-term goals (e.g., vacation, car down payment, large purchases within the next 1–3 years) before moving money into investments for long-term growth.

- The Power of High-Yield Savings (HYSA): Always use a HYSA. These accounts earn significantly higher interest rates than traditional bank savings accounts, making them the best home for liquid, protected cash.

How many savings accounts should I have?

The Goal-Based Approach is highly recommended; it is common and beneficial to have multiple savings accounts (typically 2 to 5).

The “Buckets” System: Labeling separate accounts for distinct goals makes saving clearer, less tempting to spend, and highly motivating:

- Emergency Fund (The primary focus).

- Vacation/Travel Fund.

- Car Maintenance/Future Replacement.

- Home Down Payment/Major Purchase.

- General Buffer/Taxes.

Automation: The most effective strategy is to use automation to send money from your main checking account directly into each goal-based savings account on your payday.

Conclusion: Creating a Cohesive System

Your financial system thrives on clear boundaries and purposeful movement of money. Use your checking account as the accessible utility that handles your cash flow, and rely on your savings account as the protected, interest-earning reserve that builds your future security. By adhering to the principles of optimal balancing and goal-based saving, you ensure every dollar you own is working precisely where it needs to be.

FAQs

1. What is the fundamental difference in purpose between a checking account and a savings account?

A checking account is the Transaction Hub (high liquidity, designed for daily spending and bill payments), while a savings account is the Growth Engine (designed for storage, wealth building, and reserved funds).

2. Why do banks typically offer significantly higher interest rates on savings accounts than checking accounts?

Banks reward the restriction of savings through higher interest because they have reduced risk and higher predictability. They charge for the high convenience and unlimited transactions of checking (through fees) and reward the restriction of savings (through interest).

3. What is the formula recommended for calculating the “Optimal Checking Balance”?

The recommended balance is calculated to ensure stability and avoid fees:

Optimal Checking Balance = (Monthly Expenses*1.30) + Fee Buffer

The Fee Buffer should typically be$200 to $500.

4. What is the danger of “Account Bloat” in your checking account?

“Account Bloat” occurs when you keep too much cash (like a large emergency fund) in your checking account. The danger is that this money stagnates in a low-interest environment and misses out on significant earnings in a High-Yield Savings Account (HYSA).

5. How many checking accounts should a person typically have, and what is the reason for having more than one?

For most individuals, one checking account is sufficient for simplicity and meeting fee waiver thresholds. People use multiple accounts (2-3) primarily as a disciplined budgeting tool to separate money for “Bills Only” from “Variable Spending.”

6. What is the primary financial goal for the balance of your savings account?

The top priority for your savings account is building an Emergency Fund containing three to six months of total living expenses as an essential safety net against major life events like job loss or medical expenses.

7. How does the “Goal-Based Approach” work for managing savings accounts?

It is highly recommended to have multiple savings accounts (typically 2 to 5) using the “Buckets” System. This involves labeling separate accounts for distinct goals (e.g., Emergency Fund, Vacation Fund, Car Maintenance) to make saving clearer and more motivating.

8. What is the federal limit on withdrawals or transfers from a savings account, and what is this regulation called?

Savings accounts are subject to Regulation D, which limits transfers and withdrawals to typically 6 per month. Exceeding this limit often results in fees or the bank converting the account to a checking account.