Why Your FICO Score Breakdown Looks Different From the Chart ?

You might be looking at your credit report wondering why a single late payment dropped your score by 50 points when the standard chart suggests it is just one piece of the puzzle. The reason your personal score breakdown looks different from the generic FICO pie chart is that FICO uses distinct “scorecards” to grade different types of borrowers. While the standard chart represents the general population, the algorithm actually weighs factors like debt and payment history differently depending on whether you have a “thin” credit file, a “clean” history, or past delinquencies.

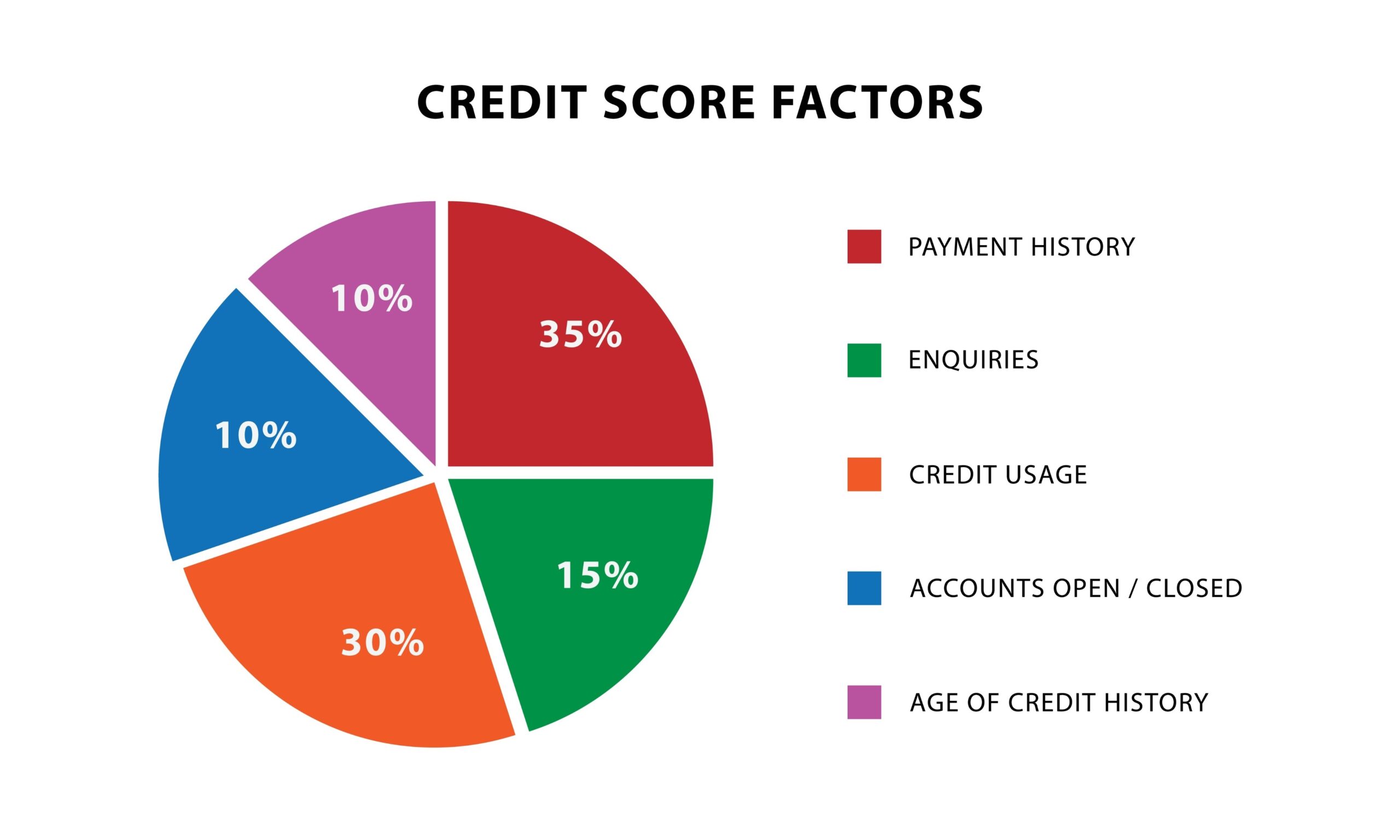

What Is the Standard FICO Score Breakdown?

To understand why your score behaves differently, we first need to look at the baseline. FICO publishes a general breakdown of how they calculate scores for the average consumer.

The General FICO Formula:

- Payment History (35%): Do you pay on time?

- Amounts Owed (30%): How much of your available credit are you using?

- Length of Credit History (15%): How long have your accounts been open?

- Credit Mix (10%): Do you have both credit cards and installment loans?

- New Credit (10%): Have you opened many accounts recently?

However, this breakdown is an average. It is not a fixed rule for every single person. If you are new to credit or have a history of missed payments, these percentages shift significantly.

Why Does My Score Not Follow the Percentages?

The FICO algorithm separates consumers into different buckets, known as scorecards. Depending on which bucket you fall into, certain actions will hurt (or help) your score more than others.

1. The “Clean” vs. “Dirty” Scorecards

FICO treats a borrower with a spotless record differently than one with negative marks.

- If you have a high score (750+): You are on a “clean” scorecard. Because the algorithm expects perfection, a single slip-up (like a 30-day late payment) is seen as a major deviation from your normal behavior. It can drop your score by 60 to 110 points instantly.

- If you have a lower score (600s): You may be on a “dirty” or “derogatory” scorecard. Since the algorithm already accounts for risk, a new late payment might only drop your score by 20 to 40 points.

2. The “Thin” vs. “Thick” File

Your credit age changes the weight of the categories.

- Thin File (New Credit): If you have only had credit for two years, you don’t have enough “Payment History” for it to truly outweigh everything else. For you, “New Credit” (opening new cards) might weigh more heavily than the standard 10% because it represents a larger portion of your total activity.

- Thick File (Established Credit): If you have a 20-year history, opening one new card barely moves the needle.

Table: How the Same Mistake Impacts Different Scores

Data simulated based on FICO high-impact ranges.

| Credit Action | Impact on 680 Score | Impact on 780 Score |

|---|---|---|

| Maxing out a credit card | Drop of 10–30 points | Drop of 25–45 points |

| 30-day late payment | Drop of 60–80 points | Drop of 90–110 points |

| Settling a debt for less | Drop of 45–65 points | Drop of 105–125 points |

Does Credit Utilization Matter More for Me?

For many people, “Amounts Owed” feels like it makes up far more than 30% of the score. This is often because credit utilization is highly volatile.

If you have a low credit limit—say $500—and you spend $250, your utilization spikes to 50%. Even if you pay it off in full, the snapshot taken by the credit bureau might catch that high balance. For someone with a $20,000 limit, spending $250 is negligible (1% utilization).

Expert Note: A survey of credit data shows that consumers with the highest FICO scores (800+) typically use less than 7% of their available credit limit.

How FICO Actually Decides Your Category Weights

| Factor in Your File | How It Changes the Weights |

|---|---|

| No credit history or <6 months | Uses FICO Score 8/9 “thin file” model → payments = 60–80% |

| Bankruptcy or major derogatory | Payment history stays dominant for 7–10 years |

| 20+ years perfect history | New credit & mix get higher weight → opening accounts helps |

| Only credit cards (no installment) | Credit mix gets almost 0% weight until you add a loan |

| Very high utilization | Amounts owed temporarily outweighs everything else |

That’s why two people with the exact same actions (one late payment, one new card) can see completely different score changes.

Real Examples

| Person A (22, first credit card 12 months ago) | Person B (45, 18 years perfect credit) |

|---|---|

| Late payment → –110 points | Late payment → –45 points |

| New card opened → –35 points | New card opened → +5 points |

| Utilization 70% → 10% → +120 points | Same utilization drop → +40 points |

Why Is My Score Different on Different Websites?

You likely see a different number on your bank’s app compared to a free credit monitoring site. This happens for two reasons:

- Different Scoring Models: Some sites use VantageScore 3.0 (which weighs credit age differently), while lenders usually check FICO Score 8 or FICO Score 9.

- Different Bureaus: One site might pull data from Experian, while another pulls from TransUnion. If a lender reported your payment to only one bureau, your scores will naturally differ.

Facts

- 53% of people with scores under 650 have “non-standard” category weights (FICO 2025 data)

- Rent reporting changes the pie for thin files — payment history jumps from ~40% to 65%+

- Average score gain from adding rent to thin file: 43 points in 60 days

- One 30-day late on a 10-year perfect file drops score only 40–60 points now (down from 90+ in older models)

Frequently Asked Questions (FAQ)

Why did my credit score drop when I paid off a loan?

When you pay off an installment loan (like a car loan), that account is often closed. This can reduce your “Credit Mix” and change your overall balance-to-loan ratio, sometimes causing a temporary dip in your score.

How often does my FICO score update?

Your score updates whenever your lenders report new data to the credit bureaus. This usually happens once a month per account, but since different lenders report on different days, your score can fluctuate daily.

Does checking my own rate hurt my breakdown?

No. Checking your own score is a “soft inquiry” and has zero impact on your FICO breakdown. Only “hard inquiries” from lenders (when applying for new credit) affect the “New Credit” category.

Why doesn’t my FICO score follow the 35/30/15/10/10 chart?

Because FICO adjusts the weights based on your file. New or thin profiles weigh payment history much heavier.

Do all credit scores use different weights?

FICO 8, 9, 10 and VantageScore 3.0/4.0 all use dynamic weights. Only old FICO models were fixed.

Why did my score drop 100 points from one late payment?

You probably have a young/thin file — payment history is 60–80% of the score in that case.

Why did opening a new card barely change my 800 score?

Long perfect files give new credit almost no weight — sometimes even +5 points.

Can reporting rent change my category weights?

Yes — adds strong positive payment history, so that category becomes even more valuable.

How often do the weights change?

Every time your report updates — new account, payment, balance change can shift the model.