What Is the Lowest Credit Score you can have ?

The lowest credit score you can have is 300. This applies to both the FICO® Score and VantageScore® models, which range from 300 to 850. Despite common myths, it is impossible to have a credit score of zero; if you have no credit history at all, you are simply “unscorable” or “credit invisible,” meaning you have no number—not a zero.

The Absolute Bottom: FICO vs. Vantage Score

While different lenders use different algorithms, the floor remains consistent for general scoring models. However, “industry-specific” scores (used specifically for car loans or credit cards) can technically dip lower.

| Scoring Model | Lowest Possible Score | Highest Possible Score |

|---|---|---|

| FICO Score 8 & 9 | 300 | 850 |

| VantageScore 3.0 & 4.0 | 300 | 850 |

| FICO Auto Score | 250 | 900 |

| FICO Bankcard Score | 250 | 900 |

Can You Actually Get a Zero?

No. A “0” credit score does not exist in the algorithms used by lenders.

- Credit Invisible: If you have never borrowed money, or haven’t used credit in years, the bureaus (Equifax, Experian, TransUnion) have no data to calculate a score. You don’t start at zero; you simply don’t exist in the scoring system yet.

- The “4” Myth: Occasionally, a rejection letter might show a code like “4” or “N/A.” This is an error code indicating insufficient history, not a score of 4.

How Hard Is It to Hit 300?

Hitting the absolute rock bottom of 300 is actually difficult. It requires more than just forgetting a bill.

Most people with “bad credit” hover between 500 and 579. To reach 300, a borrower typically needs a catastrophic combination of negative events occurring simultaneously, such as:

- Multiple defaulted loans (90+ days late).

- Active bankruptcy.

- Foreclosure or repossession.

- Maxed-out credit limits on all accounts.

Data Insight: According to 2024 FICO data, less than 2% of the U.S. population falls into the 300–499 range. It is statistically rare to be at the absolute bottom.

What Happens if You Have the Lowest Score?

Having a score near 300 puts you in the “Deep Subprime” category. This has real-world consequences beyond just getting rejected for a credit card.

- Renting Apartments: Most corporate landlords require a minimum score of 600–620. With a 300 score, you will likely need a guarantor or be asked to pay 3–6 months of rent upfront.

- Employment: For jobs in finance or government clearance, a score this low can be a red flag for potential bribery risk or irresponsibility, leading to job denial.

- Utilities: Electric and internet companies may require a security deposit ($100–$300) before turning on service.

- Predatory Loans: You may only qualify for payday loans or title loans with APRs exceeding 400%, which trap you in a debt cycle.

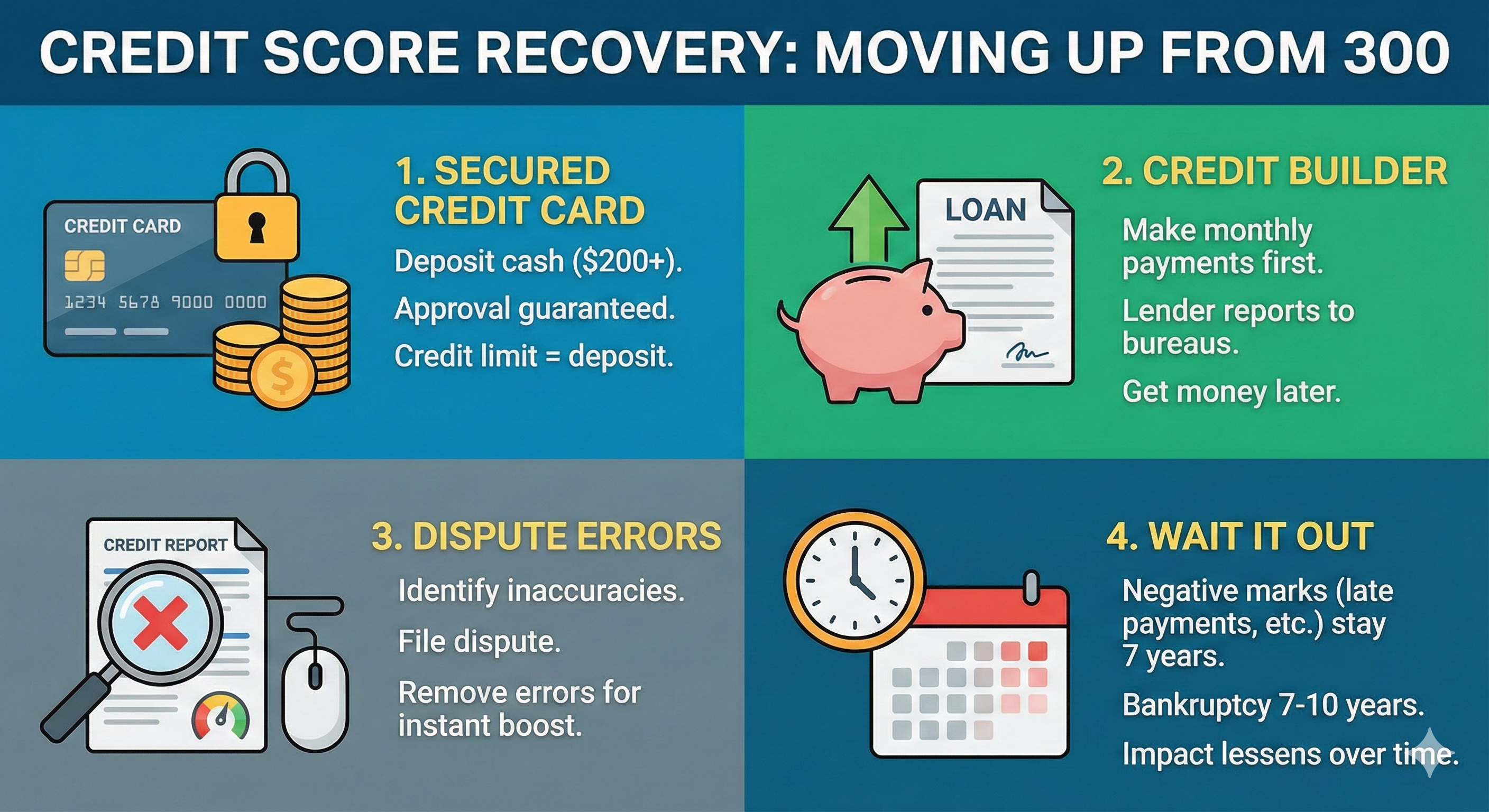

Recovery Plan: Moving Up from the Bottom

The good news about a 300 score is that the only way is up. Because the score is so low, even small positive actions can result in double-digit point jumps.

- Get a Secured Credit Card: You deposit $200, and that becomes your credit limit. Since it is backed by cash, approval is nearly guaranteed.

- Use a Credit Builder Loan: These are forced savings accounts where you make monthly payments before getting the money. The lender reports these payments to the bureaus.

- Dispute Errors: If your score is 300 due to identity theft or an error (like a debt that isn’t yours), disputing it can remove the negative mark and spike your score immediately.

- Wait It Out: Most negative marks (late payments, collections) stay on your report for 7 years, but their impact fades over time. Bankruptcy stays for 7–10 years.

Frequently Asked Questions (FAQ)

Is 500 the lowest credit score?

No, 300 is the lowest. However, 500 is often the “functional” floor for many mortgage lenders (FHA loans usually require a 500-580 minimum), so people often mistake it for the absolute lowest score.

Do I start with a score of 300?

No. When you are new to credit, you don’t start at the bottom. Once you generate enough history (usually after 6 months of using a credit account), you will typically debut with a score in the 600s or even 700s, depending on your utilization and payment status.

Can a credit score be negative?

No. Credit scores cannot go below the minimum floor of 300 (or 250 for industry-specific scores). There are no negative numbers in credit scoring.

How long does it take to fix a 300 credit score?

It depends on the cause. If it’s due to high balances, paying them off can boost your score in 30–45 days. If it’s due to bankruptcy or foreclosure, it may take 12–24 months of perfect payment history to see significant recovery.