What Is a 401k? Know Working, Contribution Limits, and Withdrawal Rules

If you’re staring at a stack of HR paperwork and wondering where your paycheck is going, you’re in the right place. The 401k is the “gold standard” of American retirement, but it’s also wrapped in enough red tape to confuse a CPA. Let’s strip away the fluff and answer your most pressing questions with zero corporate speak.

1. What is a 401k?

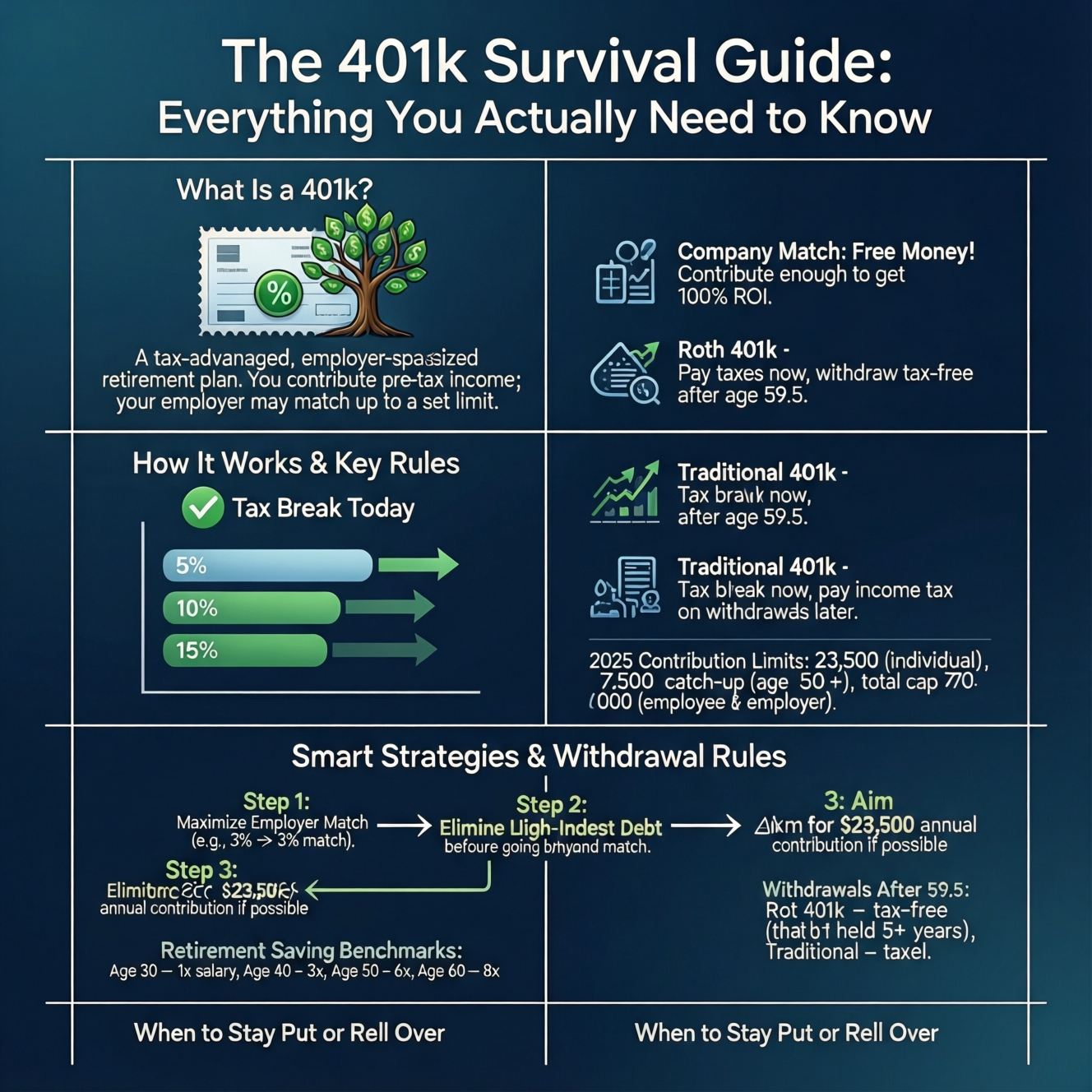

A 401k is a tax-advantaged, employer-sponsored retirement savings plan. Named after a specific section of the Internal Revenue Code, it’s essentially a deal you make with the IRS: you agree to save for the long term, and they agree to give you a massive tax break.

2. How does a 401k work?

It’s a “payroll deduction” system. You tell your employer to take a percentage of your check (say, 5% or 10%) before you ever see it. That money is sent directly to an investment account. This automation is powerful because it removes the temptation to spend first and save later—similar to how a zero-based budgeting approach forces intentional money decisions.

The Magic Ingredient: The Match Most companies offer a “company match.” If you put in 3%, they might put in 3%. This is literally free money. If you aren’t contributing enough to get the full match, you are essentially declining a portion of your salary. Don’t do that.

3. Is a 401k an IRA?

No. While both are retirement buckets, the primary difference is “who owns the keys.”

- 401k: Sponsored by your employer. They pick the provider (like Fidelity or Empower) and the investment list.

- IRA (Individual Retirement Account): Opened by you at any brokerage. You have total control and can buy almost any stock or fund in existence.

For a government-backed comparison, see 401k vs IRA differences.

4. What is a Roth 401k?

A Roth 401k is the “pay now, play later” version of the account.

- Traditional 401k: You get a tax break today, but you pay income tax when you withdraw the money in retirement.

- Roth 401k: You pay taxes on the money now, but every penny of growth and every withdrawal after age 59.5 is 100% tax-free. Expert Tip: If you think you’ll be in a higher tax bracket later in life, the Roth 401k is usually the superior choice.

5. How much can you contribute to a 401k?

The IRS sets hard limits on how much of your own salary you can defer into these accounts. These limits usually increase every year or two.

6. What is the maximum 401k contribution for 2025?

According to the IRS 401k contribution limits For the 2025 tax year, the limits are:

- Individual Contribution: $23,500 (up from $23,000 in 2024).

- Catch-up (Age 50+): $7,500.

- Total Limit (Employee + Employer): $70,000.

7. How much should I contribute to my 401k?

The “Standard Answer” is 15% of your gross income. However, life is rarely standard. Follow this hierarchy:

- The Match Level: Contribute exactly what is needed to get the maximum employer match. (100% ROI).

- Debt Check: If you have high-interest credit card debt, tackle that before going beyond the match.

- The Max-Out: If you have no high-interest debt and an emergency fund, aim for that $23,500 limit.

8. How much should I have in my 401k?

Benchmarks are scary, but they help you track progress. A general rule of thumb for total retirement savings:

- Age 30: 1x your annual salary.

- Age 40: 3x your annual salary.

- Age 50: 6x your annual salary.

- Age 60: 8x your annual salary.

- Note: If you’re behind, don’t panic. The best time to start was ten years ago; the second best time is today.

You can compare your progress with average retirement savings by age

9. When can you withdraw from a 401k?

The “Magic Age” is 59.5. This is when the IRS finally lets you touch your money without a 10% “early withdrawal” penalty.

10. At what age is 401k withdrawal tax-free?

This is a trick question!

- Withdrawals are never “tax-free” for a Traditional 401k; you always owe income tax on the amount you take out.

- Roth 401k withdrawals are tax-free after age 59.5, provided the account has been open for at least five years.

11. How to withdraw from a 401k

You contact your plan administrator (the website where you check your balance). You can usually request a “Distribution.”

- Direct Wire: They send it to your bank.

- Rollover: They send it to another retirement account (no taxes triggered).

- Check: They mail you a physical check (dangerous due to mail theft and tax withholding).

12. Can I cancel my 401k and cash out while still employed?

Technically, yes, but it’s a financial nightmare. This is called an “In-Service Withdrawal.” Most plans only allow this if you can prove “Hardship” (eviction, huge medical bills, funeral costs). If you just want the cash for a new car, your employer will likely say no. Even if they say yes, you’ll lose about 30-40% of the balance immediately to taxes and penalties.

13. What are the disadvantages of rolling over a 401k to an IRA?

Everyone tells you to roll over your old 401k when you leave a job, but there are three big reasons to stay put:

- The Rule of 55: If you leave your job in the year you turn 55, you can tap that specific 401k penalty-free. If you move it to an IRA, you have to wait until 59.5.(See IRS guidance on early distributions: https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions)

- Creditor Protection: 401ks have ironclad federal protection against lawsuits and bankruptcy. IRA protection varies by state.

- Lower Fees: If you work for a massive corporation, their institutional fund fees might be lower than what you can get as an individual.

14. How to find an old 401k

Did you leave a job in 2018 and forget your password? You aren’t alone.

- Contact HR: Call your old boss or HR department. They are legally required to keep records of your account.

- Search “Unclaimed Property”: Check your state’s treasury website.

- Use Freeerisa.com: You can search for company retirement plan filings to see who the current provider is.

- Check National Registry of Unclaimed Retirement Benefits: A private database specifically for this purpose.

Final Reality Check

The 401k isn’t a get-rich-quick scheme. It’s a get-rich-slowly scheme. It’s boring, it’s automated, and it works because it takes the “human element” (your tendency to spend money) out of the equation.

If you do nothing else today, log in to your portal and increase your contribution by 1%. You won’t feel it on Friday, but you’ll feel it in twenty years.