The Guide to Investing: Building Wealth Without Fluff

Let’s be honest: most “Guide to Investing” are boring. They’re filled with dry definitions that make your eyes glaze over before you even get to the part about making money. But here’s the reality—if you aren’t investing, you’re essentially watching your savings melt away thanks to inflation.

Investing isn’t just for people in suits on Wall Street. It’s for anyone who wants to stop trading every hour of their life for a paycheck. This guide is a deep dive into how the gears of the financial world actually turn, and how you can get them to turn in your favor.

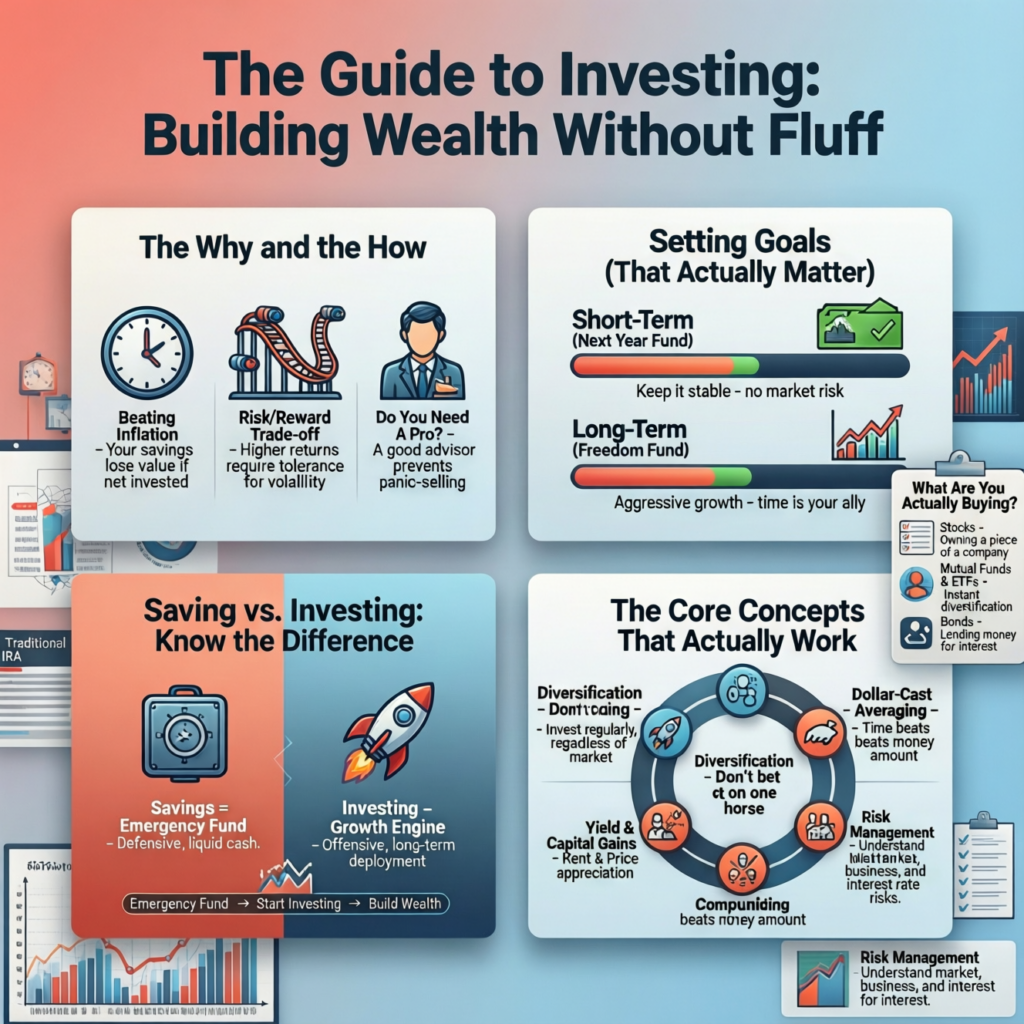

The “Why” and the “How”

1.1 Why are we even doing this?

At its simplest, investing is putting your money to work so you don’t have to work as hard later.

- Beating the “Hidden Tax”: Inflation is the silent killer of wealth. If your bank account pays you 0.01% interest while the price of eggs goes up 5%, you’re actually getting poorer. Investing is the only reliable way to outrun that.

- The Risk/Reward Trade-off: There’s no free lunch. If someone promises you 20% returns with “zero risk,” run the other way. In the real world, if you want the big gains, you have to be okay with the roller coaster.

- Do you need a “Pro”?: You can definitely do this yourself nowadays with apps, but a good advisor is less about picking stocks and more about being a “financial therapist”—keeping you from panic-selling when the market takes a dip.

1.2 Setting Goals (That Actually Matter)

“I want to be rich” isn’t a goal; it’s a wish. You need to categorize your money by when you need it back.

- Short-Term (The “Next Year” Fund): If you need the money for a wedding or a house down payment in 24 months, don’t put it in the stock market. Keep it in a High-Yield Savings Account or a CD. You want stability here, not growth.

- Long-Term (The “Freedom” Fund): This is for retirement or a kid’s college fund 15 years away. Because you have time, you can afford to be aggressive. If the market crashes tomorrow, it doesn’t matter because you aren’t selling for a decade.

1.3 Saving vs. Investing: Know the Difference

Saving is defensive. It’s your emergency fund—the cash you keep under the “digital mattress” for when the car breaks down. Investing is offensive. It’s the money you’ve deployed into the world to bring back more money. You need a solid defense (savings) before you can play a good offense (investing).

The Core Concepts (The Stuff That Actually Works)

2.1 Risk: It’s Not Just About Losing Money

Most people think risk is just “the stock went down.” But there are layers to it:

- Market Risk: The whole world is having a bad day (recession).

- Business Risk: You bought shares in a company that just got caught in a scandal.

- Interest Rate Risk: When the Fed raises rates, your bonds usually lose value.

The goal isn’t to avoid risk—it’s to manage it.

2.2 Measuring the “Win” (Returns)

Your return is more than just the price going up.

- Yield: This is the “rent” you get for owning something (dividends from stocks or interest from bonds).

- Capital Gains: Buying low and selling high.

- The “Real” Return: If you made 7% but inflation was 4%, you only really made 3%. Always look at the “Real” number.

2.3 Diversification: Don’t Bet on Just One Horse

You’ve heard “don’t put all your eggs in one basket.” In investing, that means owning a bit of everything. If tech stocks are crashing, maybe your energy stocks or your bonds are holding steady. It smoothes out the ride so you can actually sleep at night.

2.4 Dollar-Cost Averaging (The Lazy Way to Win)

This is the most powerful tool for the average person. You invest $200 every single month, regardless of whether the market is at an all-time high or a terrifying low.

- When prices are high, your $200 buys less.

- When prices are low (on sale!), your $200 buys more. Over time, you end up with a great average price without ever having to “time” the market.

2.5 The Magic of Compounding

Compound interest is just “interest on interest.” If you start at 20, you’re playing the game on “Easy Mode.” If you start at 45, you’re on “Hard Mode.” Time is more valuable than the amount of money you start with.

What are you actually buying?

3.1 Stocks: Owning a Piece of the Pie

When you buy a share of a company, you are a part-owner. You’re entitled to a slice of their profits.

- Blue Chips: The boring, reliable giants (think Apple or Disney).

- Growth Stocks: The “moonshots” that might double in a year or go to zero.

- Dividends: Some companies literally send you a check every three months just for holding their stock. This is the dream of “passive income.”

3.2 Mutual Funds & ETFs: The “Bundle”

Instead of trying to pick the next Amazon, you buy a Mutual Fund or an ETF. These are “baskets” of hundreds of different stocks. You get instant diversification with one click.

- Index Funds: These just track the whole market (like the S&P 500). They have super low fees and usually beat the “experts” in the long run anyway.

3.3 Bonds: Being the Lender

Bonds are basically you acting as the bank. You lend money to a company or the government for a set time, and they pay you back with interest. They are generally safer than stocks, which is why people buy more of them as they get older and closer to retirement.

The “Buckets” (Where to Put Your Money)

4.1 Traditional IRA vs. Roth IRA

This is the most common question in investing.

- Traditional IRA: You get a tax break now. You put in $6,000, and the IRS treats you like you earned $6,000 less this year. But, when you retire and take the money out, you pay taxes then.

- Roth IRA: You pay taxes now, but the money grows and comes out totally tax-free in retirement. If you think you’ll be more successful later in life, the Roth is usually the winner.

4.2 Specialized Accounts

- Education IRA (Coverdell): A great way to save for your kid’s school without the tax man taking a cut.

- SEP & SIMPLE IRAs: If you’re a freelancer or a small business owner, these are your best friends. They let you tuck away way more money than a standard IRA.

Final Thoughts: The Cost of Waiting

The biggest mistake people make isn’t picking the wrong stock—it’s waiting until they “have enough money” to start. You don’t need $10,000 to start. You need $50 and a recurring transfer.

Investing is a skill, but more than that, it’s a habit. The sooner you start, the more “boring” your path to wealth becomes—and in the world of finance, boring is usually where the money is. Take the first step, stay the course, and let time do the rest.

FAQs

1. Is the stock market basically just gambling?

If you’re “day trading” based on a TikTok tip, yes, it’s gambling. But if you’re buying a piece of the world’s most profitable companies and holding them for years, it’s participating in global growth. One is a coin flip; the other is a math problem where time is on your side.

2. How much money do I actually need to start?

Honestly? Like $5. Most modern brokerage apps let you buy “fractional shares.” You can buy $1 worth of Google or Amazon. The amount matters way less than the habit of doing it every single month.

3. What if the market crashes right after I invest?

If you don’t need that money for 10 years, a crash is actually a gift—it’s a “sale.” You’re buying more shares for fewer dollars. The only way you “lose” during a crash is if you panic and sell at the bottom.

4. Should I pay off my credit cards or invest first?

Pay off the cards. If your credit card interest is 22% and the stock market averages 10%, you’re losing 12% every year by investing instead of paying debt. Kill the high-interest debt first, then play offense.

5. How do I know which stocks to pick?

Most people shouldn’t pick individual stocks. It’s a full-time job. For 90% of us, buying an S&P 500 Index Fund (which owns the 500 biggest US companies) is the smartest move. It’s low-stress and high-reward over the long term.

6. Is it too late for me to start?

The best time to start was 20 years ago. The second best time is today. Even if you only have 10 years until retirement, investing can still help you outpace inflation. You just have to be more calculated with your risk.

7. Do I have to pay taxes on my gains?

Yes, usually. If you sell a stock for more than you bought it, Uncle Sam wants his “Capital Gains” tax. However, if you use “buckets” like a Roth IRA, you can avoid those taxes entirely. That’s why where you put your money is just as important as what you buy.

8. Can I get my money out whenever I want?

Technically, yes, you can sell your stocks and have the cash in a few days. But if it’s in a retirement account like an IRA or 401k, the government will slap you with a 10% penalty if you take it out before you’re 59.5. Think of your investment money as “locked away” for your future self.