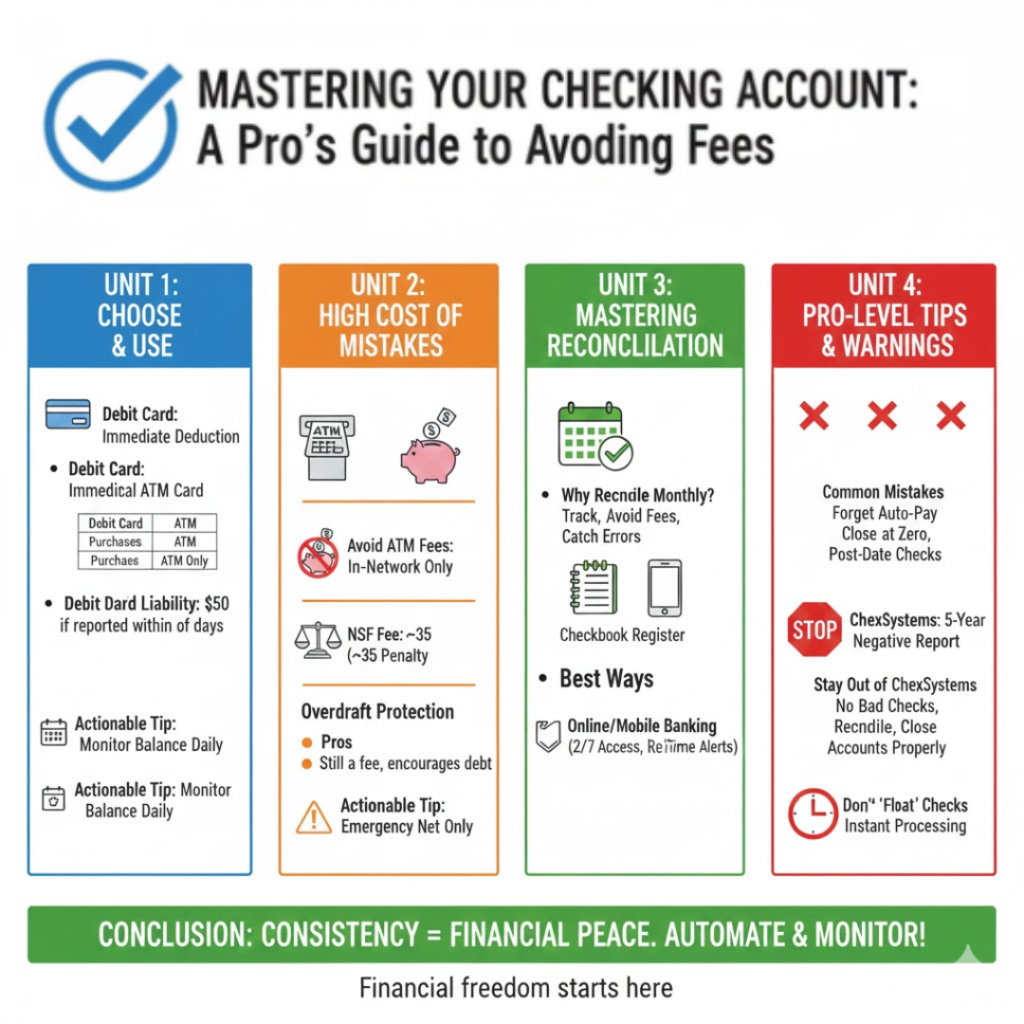

Managing Your Checking Account Like a Pro

Few financial mistakes are as instantly punitive and costly as banking errors. A single missed calculation or forgotten auto-pay can result in a Non-Sufficient Funds (NSF) fee—a $35 penalty, often compounded by a matching fee from the payee. These are the high costs of poor banking habits. Learning managing checking account best practices is essential to protecting your hard-earned money.

Learn essential checking account tips: prevent NSF fees, understand overdraft protection, know debit card liability, and how to stay out of ChexSystems. Financial freedom starts here.

Why checking accounts are the foundation ?

Checking accounts are the command center of your daily financial life. They provide the most liquid funds for routine expenses, offer essential documentation for tax purposes, and are critical for avoiding bank fees and managing cash flow.

Unit 1: Choosing & Using Your Account

How to Choose and Use a Checking Account

A checking account is crucial for secure, modern financial management. It allows you to:

- Pay Bills Securely: Facilitates electronic and paper payments, eliminating the need to handle large amounts of cash.

- Track Expenses: Provides a clear, documented record of all money flowing in and out of your possession.

- Establish Banking History: Creates a history of responsible use, which can be necessary for opening other financial products like savings accounts or securing loans.

What is a debit card and how does it work?

A debit card is a payment instrument issued by your bank that is directly linked to your checking account balance. When you use a debit card, the funds are immediately deducted from your available balance. This is known as immediate deduction.

| Comparison | Debit Card | Traditional ATM Card |

|---|---|---|

| Usage | Purchases (in-store, online) and ATM withdrawals | ATM withdrawals and sometimes in-person bank transactions |

| Deduction | Immediate deduction from checking account | Immediate deduction from checking account |

| Liability | Limited (see below) | Highly variable, often less protected |

Debit Card Liability Limit: If your debit card is lost or stolen, your maximum liability is only $50 if you report the loss to your bank within two business days. If you wait longer than two business days, your liability can increase up to $500. If you fail to report the loss within 60 calendar days after the bank statement showing the unauthorized transfer was sent, your liability may become unlimited.

Actionable Tip

Always monitor your account balance, especially after using your debit card for purchases. Relying solely on your memory or a single check of the balance days after a transaction is the fastest way to incur fees.

Unit 2: The High Cost of Mistakes

How to Avoid the Most Expensive Checking Account Fees

How can I avoid ATM fees?

ATM fees are often doubled, hitting you from both the ATM owner and your own bank. To maximize avoiding bank fees:

- Use In-Network Machines: Always check your bank’s website or mobile app to locate ATMs that are part of their fee-free network.

- Plan Withdrawals: If you must use an out-of-network ATM, withdraw a larger amount once instead of several smaller amounts across multiple transactions.

- Expect Two Fees: When you use a “foreign” (out-of-network) ATM, be prepared to pay the ATM owner’s surcharge fee and your bank’s fee for using an external machine.

What is a Non-Sufficient Funds (NSF) fee?

A Non-Sufficient Funds (NSF) fee is a substantial penalty charged by a bank when a payment instrument (such as a check, automated clearing house (ACH) transaction, or debit card transaction) is presented for payment, but the available balance in the account is insufficient to cover the full amount. This fee is also commonly referred to as a “bounced check” fee. The transaction is typically rejected by the bank.

Should I get overdraft protection? Pros and Cons

Overdraft protection is a service offered by banks to prevent a transaction from being declined when your available balance is too low.

Overdraft protection typically functions as a transfer of funds from a linked account (such as a savings account or a credit union’s line of credit) to cover a shortage in your checking account, allowing the transaction to clear.

Pros and Cons:

- Pro: It prevents the embarrassment and potential penalty fees from the payee when a payment is rejected (like having a utility payment bounce).

- Con: While usually cheaper than an NSF fee, a fee is still assessed for the transfer or line of credit usage. It encourages relying on debt rather than budgeting accurately.

Actionable Tip: Overdraft protection is typically cheaper than an NSF fee, but remember that a fee is still assessed. It should be used only as an emergency safety net, not a regular budgeting tool.

Unit 3: Mastering Reconciliation

Why should I balance my checking account monthly?

Balancing your account, or reconciliation, is vital for proper financial managing checking account. It helps you:

- Track Funds: Ensures you have an accurate, real-time understanding of what funds are truly available.

- Avoid Overdrawing: Prevents surprise shortages, eliminating costly NSF fees and overdraft charges.

- Catch Bank Mistakes: Identifies any errors made by the bank, which do occasionally occur.

- Identify Unauthorized Activity: Quickly flags fraudulent or unauthorized debit card transactions.

What are the best ways to reconcile my account?

Historically, reconciliation meant using a physical ledger. Today, you have two highly effective options:

- Checkbook Register: Still useful for tracking immediate cash and debit card expenditures as they happen, ensuring no purchase is overlooked before it posts to your bank’s system.

- Online/Mobile Banking Tools: Use your bank’s transaction history and balance updates as the primary source of truth, cross-referencing it with your own records.

Benefits of Online and Mobile Banking for Checking Accounts

Leveraging technology is a powerful tool for effective managing checking account:

- 24/7 Access: Check your balance and history at any time from anywhere.

- Real-Time Balance Checks: Confirm your available balance before making large purchases.

- Error Identification: Set up instant alerts for unusual activity or large transactions.

- Account Transfers: Easily move funds between checking and savings accounts to prevent overdrafts.

Unit 4: Pro-Level Tips and Warnings

What are the most common checking account mistakes to avoid?

Effective avoiding bank fees relies on avoiding these common pitfalls:

- Forgetting to Check Balance Before Auto-Pay: Relying on scheduled payments without verifying sufficient funds will result in an NSF fee.

- Closing an Account at Zero Balance: Always leave a few dollars when closing an account; residual, small fees can drive the balance negative and get you reported to ChexSystems.

- Post-Dating Checks: Writing a check for a future date (post-dating) is risky; if the recipient deposits it early, it could be reported as a bad check.

What is ChexSystems and how long does a negative report last?

ChexSystems is a consumer reporting agency for bank accounts. Its member institutions (banks and credit unions) report individuals who have “mishandled” their accounts, typically due to excessive overdrafts, unpaid bank fees, or fraudulent activity. Banks rely on this database to decide whether to approve an application for a new checking account.

Negative Report Duration: A negative report stays in the ChexSystems database for five years from the date of the reporting institution’s final action.

How to stay out of the ChexSystems database?

Maintaining a positive banking relationship is crucial for managing checking account successfully:

- Don’t Write Bad Checks: Never issue a check if the funds are not immediately available.

- Confirm Deposit Clearance Time: Understand that deposited funds may not be instantly available; confirm the clearance schedule before spending the money.

- Reconcile Promptly: Reconcile your account every week to catch any errors or potential problems before they lead to fees.

- Properly Close Old Accounts: Always pay all outstanding fees and confirm the bank has formally closed the account to prevent small charges from turning into a negative balance.

Why shouldn’t I “float” checks?

The concept of “floating” a check—writing it today and hoping to deposit funds before the recipient cashing it—was once common but is now extremely dangerous. Due to electronic processing and instantaneous ACH transfers, the “float” time delay has been significantly reduced or entirely eliminated. Relying on this delay makes it highly risky to prevent a Non-Sufficient Funds (NSF) fee.

Conclusion and Next Steps

The cornerstone of financial stability is responsible checking account management. By mastering the art of reconciliation, automating your payments, and understanding the high-risk pitfalls like NSF fees and ChexSystems reporting, you can turn your checking account from a source of anxiety into a powerful tool for financial growth.

Commit to checking your balance before every major transaction and leveraging online tools. These simple, consistent checking account tips are the best way toward avoiding bank fees and securing your financial future.

FAQs

What is the minimum balance I should keep in my checking account to avoid fees?

This depends entirely on your bank’s fee schedule. Most banks waive monthly maintenance fees if you maintain a certain daily minimum balance (e.g., $500 or $1,500) or meet specific activity requirements (e.g., direct deposit). Always review your account’s terms and conditions.

How long does it take for a deposited check to clear and be available in my account?

While digital deposits are often credited immediately, the funds may not be available for withdrawal right away. Federal regulations require banks to make the first $225 of a deposit available the next business day. Larger amounts can take 2 to 7 business days, depending on the check amount and your bank’s policy.

If I have an NSF fee, is it better to close the account immediately?

No. Closing an account while it has a negative balance (due to an NSF fee or other charges) is a guaranteed way to be reported to ChexSystems. You should immediately pay the negative balance, then properly close the account after all funds have cleared and the balance is $0.

How can I get an NSF fee waived by my bank?

Banks often offer a “one-time courtesy waiver,” especially if you have a long history of good account management. Call your bank, apologize for the oversight, explain it was a one-time mistake, and politely ask if they can waive the fee as a goodwill gesture.

Is it safer to use a debit card or a credit card for online purchases?

A credit card is generally safer. With a credit card, you are spending the bank’s money, and liability for fraud is often $0. With a debit card, fraudsters directly access your checking account funds, and while liability is limited to $50 if reported quickly, recovering the money can be disruptive.

I reconcile my account with my mobile app. Is a checkbook register still necessary?

The checkbook register is less critical but still useful. Mobile banking shows your posted balance. The register is important for tracking pending transactions (like recent debits or checks you wrote that haven’t cleared yet), helping you avoid overdrawing the account based on the mobile app’s data alone.

What specific negative actions will land me in the ChexSystems database?

The most common reasons are unpaid negative balances (due to overdrafts or fees) after the bank closes the account, repeated bad checks, or evidence of fraudulent activity. The bank reports you when they suffer a financial loss due to your actions.

Does Overdraft Protection cover ATM withdrawals?

By law, banks must ask you to opt-in specifically for overdraft services to cover ATM withdrawals and one-time debit card purchases. If you do not opt-in, those transactions will simply be declined if you don’t have enough funds, preventing the overdraft fee.

If I lose my debit card, what are the first two things I should do immediately?

Immediately contact your bank to report the card lost or stolen. 2. Review your recent transaction history for any unauthorized purchases. Reporting within two business days limits your liability to just $50.

How often should I check my checking account balance?

Ideally, you should check your balance every day, or at least every other day. If you use automatic payments or a debit card frequently, daily monitoring is the best way to catch errors, pending charges, and ensure funds are sufficient before large auto-pays hit.