How Rent Payments Affect Your Credit Score: Supercharge Your Credit Without Debt

Introduction

For millions of renters across the U.S. and beyond, rent is the single largest monthly expense — often even higher than a mortgage payment. Despite the financial responsibility this represents, traditional credit reporting systems long ignored rent payments when calculating credit scores. That meant on-time rent payments, made consistently month after month, did little or nothing to improve a person’s credit profile.

Fortunately, the tide is turning. Thanks to updates in credit scoring models and the rise of rent-reporting fintech solutions, your monthly rent can now do more than keep a roof over your head — it can actively boost your creditworthiness. If you’ve ever felt penalized for not having a credit card or loan, this shift presents an opportunity to leverage your existing habits for financial gain.

In this blog, we’ll break down how rent payments affect your credit score, examine which scoring models include rent data (FICO 9, FICO 10, VantageScore 3.0 & 4.0), and give you tips to ensure your rent truly works in your favor.

Why Credit Scores Matter

A credit score isn’t just a number — it’s a financial passport. It plays a pivotal role in your ability to access housing, secure loans, open utility accounts, and sometimes even land a job. Lenders use your score to determine how risky it is to lend to you, which directly impacts whether you’re approved and the interest rate you’ll pay. A strong credit score can mean thousands of dollars saved over a lifetime through better loan terms, lower insurance premiums, and waived deposits on utilities or apartments. On the other hand, a poor or nonexistent credit score can lead to denials, higher fees, or limited access to financial tools.

Traditionally, building or improving your credit score involved strategies like opening a credit card, taking out a loan, or becoming an authorized user on someone else’s account. But not everyone has access to these options — and for many, the risks (like going into debt or missing payments) outweigh the rewards. That’s where rent reporting comes in. By simply paying rent — something you’re likely doing already — you can now build credit more safely and inclusively.

Understanding Traditional Credit Scoring Models

Credit scoring models analyze your credit report and generate a three-digit score, usually between 300 and 850. The most commonly used models include:

FICO Score (Versions 8, 9, and 10)

- FICO 8: Still the most widely used by lenders, but it does not consider rent payments.

- FICO 9: Introduced in 2014, this version began to include rent data when it’s reported by landlords or rent-reporting services.

- FICO 10 and FICO 10T: These latest models give more weight to rental history and trend data, but adoption has been slow across the lending industry.

VantageScore (Versions 3.0 and 4.0)

- VantageScore was developed by the three major credit bureaus (Experian, Equifax, and TransUnion).

- VantageScore 3.0: Began considering rental data if it is included in the credit file.

- VantageScore 4.0: Built on 3.0, but with more advanced analytics and emphasis on trended data (like payment patterns over time).

Both VantageScore models are more receptive to non-traditional data, including utility and rent payments.

How Rent Payments Get Reported

Contrary to common belief, your rent payments don’t automatically appear on your credit report like credit cards or loans. The three major credit bureaus — Equifax, Experian, and TransUnion — require verified reporting from trusted sources. That means for your rent to count toward your credit score, it must be submitted through an approved channel. Here are the main ways to get your rent payments reported:

1. Your Landlord or Property Manager

Some large apartment complexes and property management companies have systems in place to report tenant payment history directly to the credit bureaus. This is more common with institutional landlords who manage hundreds or thousands of units. If you’re renting from such a company, it’s worth asking whether they already report rent — or if they’d be open to doing so. Unfortunately, many independent landlords or smaller property managers don’t participate in rent reporting due to limited infrastructure.

2. Rent Reporting Services

Independent rent reporting services like AxcessRent, RentTrack, and Experian RentBureau allow tenants to take credit-building into their own hands. These platforms act as intermediaries between you, your landlord, and the credit bureaus. Some services charge a small monthly fee, while others may include it as part of broader credit-building packages. With AxcessRent, for example, renters can build credit just by making on-time rent payments — no credit card or loan required.

3. Third-Party Fintech Platforms

Innovative fintech companies are now embedding rent reporting into apps and tools designed for underserved or credit-invisible communities. These platforms often combine rent reporting with features like budgeting, savings, and debt tracking. For people without traditional financial access, they offer a much-needed alternative route to building credit in a fairer, more inclusive way.

Benefits of Reporting Rent

- Faster Credit Building: Consistent, on-time rent payments can boost your credit score, especially if you have a thin credit file.

- Credit Score Visibility: Over 45 million Americans are “credit invisible”. Rent reporting can make you visible to lenders.

- No Debt Required: Unlike credit cards or loans, rent doesn’t require borrowing.

- Financial Empowerment: It gives renters more control and transparency over their financial growth.

Challenges and Limitations of Rent Reporting

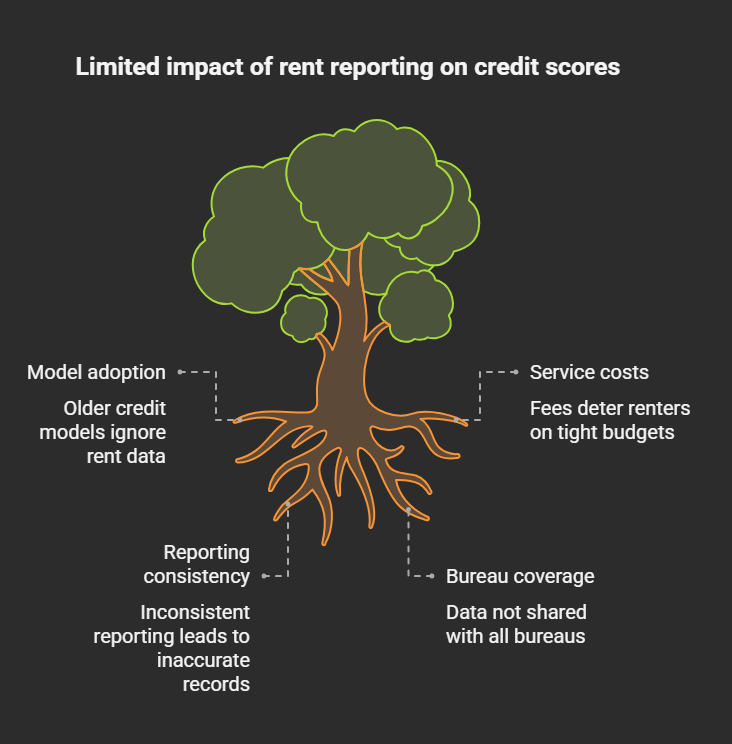

While the idea of turning your rent payments into a credit-building opportunity is exciting, it’s essential to recognize that rent reporting isn’t a silver bullet. Several practical and systemic limitations still hinder its full potential.

1. Model Adoption Isn’t Universal

One of the biggest hurdles is that not all credit scoring models weigh rent data equally — or at all. For example, FICO Score 8, the most commonly used version by lenders today, does not factor in rent payments, even if they’re reported. Only newer models like FICO 9, FICO 10, and VantageScore 3.0 & 4.0 include rental data as part of their scoring algorithms. Unfortunately, many banks, credit card issuers, and mortgage lenders still rely on older versions. This means that even if your rent payments are reported and visible on your credit file, they might not influence the final score a lender sees.

2. Some Services Cost Money

Another barrier is cost. Many rent reporting services charge tenants a fee — either monthly, annually, or as a one-time setup. While some programs (like AxcessRent) offer affordable or subsidized plans, others can charge $6–$15/month, which may deter renters on a tight budget. For a service designed to support financially vulnerable populations, affordability is key — and sadly, not all platforms deliver on that.

3. Inconsistent or Unreliable Reporting

If your landlord or rent reporting service fails to report consistently, your rental history might not be reflected accurately. Gaps or missed months — even if you paid on time — can make your record incomplete or misleading. Worse, some services may not be integrated well with the major credit bureaus, risking delayed or lost data.

4. Not All Bureaus Get the Data

Many rent reporting platforms only report to one or two of the three major credit bureaus. For example, a service might report to TransUnion and Equifax but not Experian, or vice versa. This fragmented approach can reduce the overall impact of your rental history, especially if a lender pulls a report from the bureau that doesn’t have your rent data.

How to Make Sure Your Rent Counts

- Talk to Your Landlord: Ask if they report rent. If not, recommend a rent-reporting platform.

- Choose a Reputable Service: AxcessRent, for instance, reports to all major bureaus, maximizing your exposure.

- Stay Consistent: Late payments can be reported too. Set up auto-pay if possible.

- Monitor Your Credit Reports: Use free tools or annualcreditreport.com to ensure your rent is reflected.

Credit Building with AxcessRent

AxcessRent simplifies the rent-reporting process by connecting directly with landlords and credit bureaus. It allows you to:

- Report rent without a credit card.

- Track your credit-building progress.

- Access additional financial wellness tools.

- Avoid high-interest debt or loans.

It’s ideal for renters seeking an inclusive, no-debt path to credit improvement.

Real Impact: Examples and Statistics

- According to a TransUnion study, rent reporting increased scores by up to 40 points for thin-file consumers.

- Renters who consistently report payments are 60% more likely to qualify for loans within a year.

- 7 in 10 renters say they would choose a unit that offers rent reporting over one that doesn’t.

Who Benefits Most from Rent Reporting?

- Young Adults and Students: No credit history? Start here.

- Immigrants and Expats: Establish credit without loans.

- Low-Income Renters: Build credit without taking on risk.

- Rebuilders: Recover from financial hardship by showing responsibility through rent.

The Future of Credit Scoring

As fintech evolves, so will the credit industry. Alternative data—including rent, subscriptions, and utilities—is becoming more mainstream. Lenders are realizing that traditional credit reports don’t tell the whole story. Rent reporting is one of the most promising paths toward a more inclusive and accurate credit system.

Final Thoughts

Rent payments are more than just a monthly obligation—they’re an untapped resource that can empower your financial future. With modern credit scoring models such as FICO 9, FICO 10, and VantageScore 3.0 and 4.0, your on-time rent payments now have the potential to positively influence your credit score — a shift that could open doors to better loans, lower interest rates, and long-term financial freedom.

However, this opportunity doesn’t unlock itself automatically. Rent reporting must be initiated, either through a landlord-partnered service or a third-party platform. This is where companies like AxcessRent step in. They help bridge the gap between your rent payments and your credit report—without requiring you to take on debt like a loan or credit card. For renters who pay on time every month but struggle to build credit, this is a game-changer.

It’s important to choose a reporting partner that’s reliable, affordable, and transparent—because consistency is everything. A single missed report or data error can undermine months of progress.

So, start small. Choose a rent-reporting service that aligns with your goals. Stay consistent with your payments. And let your rent work for you—not just your landlord.

With the right tools, building credit doesn’t have to be complicated. It can start right where you live.