Credit Bureaus and Rental Reporting: What You Need to Know

For decades, your creditworthiness was determined by a narrow set of financial behaviors: Do you pay your credit cards on time? Are your loan payments up to date? What’s your debt-to-income ratio? But what about your rent?

Millions of Americans make on-time rent payments every month—often their largest and most consistent financial obligation—yet this responsible behavior has historically been ignored by traditional credit scoring systems. That’s beginning to change.

Today, rental payment history is increasingly being recognized as a valid indicator of financial reliability. Thanks to evolving credit models and new reporting technologies, your rent can now count toward your credit score—but only if it’s reported to the right place and verified correctly.

At the heart of this transformation are the three major credit bureaus: Experian, Equifax, and TransUnion. These institutions collect, store, and distribute consumer credit data used by lenders to assess risk. While they’ve traditionally focused on loans and credit cards, all three now accept rental payment data—though each does so differently.

In this comprehensive guide, we’ll break down how Experian, Equifax, and TransUnion handle rental reporting, what it means for your credit score, and how you can ensure your rent payments work for you—not just your landlord.

Whether you’re building credit from scratch, recovering from financial setbacks, or simply want to maximize your financial reputation, understanding how credit bureaus treat rental payments is essential.

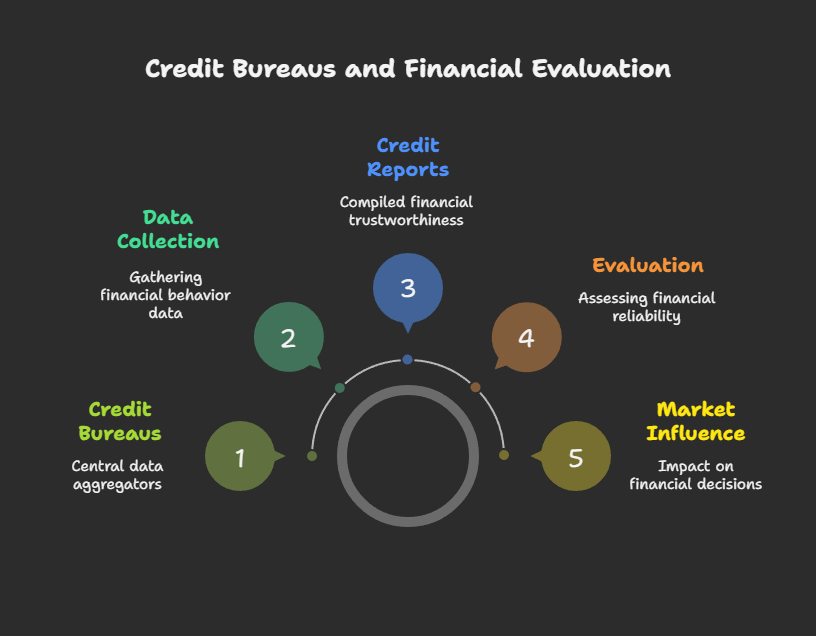

The Role of Credit Bureaus in Financial Life

Before diving into rental reporting, it’s important to understand what credit bureaus do and why they matter.

Credit bureaus—also known as credit reporting agencies—are data aggregators. They don’t create credit scores themselves but collect information from lenders, banks, and other financial institutions about your borrowing and repayment behavior. This data is then compiled into credit reports, which are used by lenders, landlords, insurers, and even employers to evaluate your financial trustworthiness.

The Big Three—Experian, Equifax, and TransUnion—dominate the U.S. credit reporting landscape. While they operate independently, they share a common goal: to provide accurate, timely, and standardized credit information.

However, they don’t always report the same data, and not all creditors report to all three. This means your credit report—and score—can vary between bureaus. And when it comes to rental reporting, the differences become even more pronounced.

Experian: Leading the Charge in Rental Reporting

Experian Boost: A Game-Changer for Renters

When it comes to including alternative data like rent, Experian leads the pack. Its innovative tool, Experian Boost, allows consumers to add positive payment histories—including rent, utilities, and phone bills—to their Experian credit report—for free.

Here’s how it works:

- You connect your bank account to Experian Boost.

- The system scans for recurring payments to landlords or property managers.

- Once identified, you can choose to add those payments to your credit file.

- The update is instant, and your VantageScore 3.0 (used by Experian) can increase immediately.

This is a powerful opportunity for renters with thin or limited credit files. According to Experian, 75% of users see an immediate score increase, with many gaining 10–20 points or more.

What Rent Data Does Experian Accept?

Experian accepts rent payments through:

- Experian Boost (consumer-initiated)

- RentBureau (via property management companies)

- Third-party services like RentReporters and Piñata

However, there’s a catch: Experian Boost only affects your Experian credit score, not your FICO Score 8 or other models widely used by mortgage lenders. It also only impacts VantageScore 3.0, not all scoring systems.

Still, for credit cards, personal loans, and fintech lenders who use Experian data, this boost can be the difference between approval and denial.

Unique Insight: Experian Rewards Consistency, Not Just History

Unlike traditional scoring models that focus on debt usage, Experian Boost emphasizes positive behavioral patterns. This means consistent rent payments—even without a long credit history—can significantly improve your standing.

Equifax: Selective but Growing in Rental Inclusion

How Equifax Handles Rent Payments

Equifax has been more cautious than Experian in adopting alternative data, but it does accept rental payment information—just not through a consumer-facing tool like Boost.

Instead, Equifax receives rent data primarily through:

- ClearNow (a rent payment and reporting platform)

- CoreLogic Rental Payment History™

- Property management software integrations

These systems are typically used by large apartment complexes and corporate landlords, meaning tenant-initiated reporting is limited.

If your landlord uses one of these platforms and reports to Equifax, your on-time rent payments will appear on your credit report—often under a section labeled “Alternative Data” or “Rental History.”

Impact on Equifax Credit Scores

Equifax includes rental data in its Equifax Credit Score 3.0 and Premier scoring models, both of which are used by some lenders. However, like Experian, the impact depends on the scoring model being used.

A key limitation: Equifax does not offer a free tool for consumers to self-report rent, unlike Experian Boost. This puts renters at a disadvantage unless their landlord participates in a reporting program.

The Bottom Line on Equifax

While Equifax is making progress, it remains less accessible for individual renters. The burden is on landlords to report, and many still don’t.

That said, if you live in a managed property with automated rent collection, there’s a good chance your payments are already being reported—so check your Equifax report regularly to confirm.

TransUnion: The Most Comprehensive Rental Reporting System

TransUnion RentBureau: The Gold Standard

When it comes to rental reporting, TransUnion has the most robust infrastructure through its RentBureau division—one of the largest rental payment databases in the U.S.

RentBureau collects data from over 12 million rental units nationwide, partnering with property management companies, payment processors, and credit reporting services. It doesn’t just report rent—it verifies and standardizes it for inclusion in credit files.

What sets RentBureau apart?

- FCRA-compliant reporting: Meets federal standards for accuracy and fairness.

- Trended data: Shows payment history over time, not just a snapshot.

- Integration with TransUnion CreditVision®: A next-gen scoring model that rewards consistent behavior.

How Renters Benefit from TransUnion Reporting

If your rent is reported through RentBureau your payment history will appear on your TransUnion credit report and may influence your VantageScore 4.0 and FICO Score 9, both of which consider alternative data.

This is especially valuable because:

- FICO Score 9 includes rental data if it’s verified and reported properly.

- VantageScore 4.0 was designed with alternative data in mind.

A 2023 study by the Consumer Financial Protection Bureau (CFPB) found that verified rent reporting through TransUnion increased credit scores by an average of 46 points for consumers with limited credit histories.

Can You Self-Report to TransUnion?

Yes—but not directly. You need to use a third-party service like:

- RentReporters

- LevelCredit

- Piñata (reports to TransUnion via partnerships)

These services collect your bank statements, lease agreement, and landlord info, then submit the data to TransUnion (and other bureaus) on your behalf.

How Rental Reporting Impacts Your Credit Score

Which Scoring Models Count Rent?

Not all credit scores are created equal. Here’s how major models treat rent:

| Scoring Model | Include Rent ? | Requirement |

|---|---|---|

| FICO Score 8 | ❌ No | Traditional data only |

| FICO Score 9 | ✅ Yes | Verified, FCRA-compliant |

| FICO XD | ✅ Yes | Alternative data focused |

| VantageScore 3.0 | ✅ Yes | Via Experian Boost |

| VantageScore 4.0 | ✅ Yes | All bureaus, trended data |

This means your score gain depends on which model a lender uses. If you’re applying for a mortgage, the lender likely uses FICO Score 8 or 9—so verified reporting to all three bureaus is ideal.

Real-World Impact: Case Study

Meet Tanya, a 29-year-old teacher in Atlanta. She had no credit cards and never taken a loan, but she’d paid $1,300 in rent on time for five years. After using Axcessrent to report her history to all three bureaus, her credit profile changed dramatically:

- Experian Score: 580 → 632 (+52)

- TransUnion Score: 570 → 645 (+75)

- Equifax Score: 565 → 610 (+45)

Within six months, she qualified for a car loan at 6.2% APR, saving over $2,000 in interest compared to subprime rates.

Challenges and Limitations of Rental Reporting

Not All Services Are Equal

While many apps claim to “boost your credit with rent,” not all meet FCRA standards. Some only report to one bureau, others lack verification, and a few don’t notify you if the data is rejected.

Always ask:

- Does this service report to all three bureaus?

- Is the data verified with documentation?

- Is it FCRA-compliant?

Landlord Participation Is Key

Most individual landlords don’t report rent. Without their cooperation—or integration with reporting-friendly software—tenants must take the initiative.

Privacy and Data Security

Linking your bank account to a rent reporting service carries risks. Always choose platforms with:

- Bank-level encryption

- SOC 2 compliance

- Clear privacy policies

The Future of Rental Reporting

The financial world is shifting toward inclusive credit scoring. With over 44 million Americans having little or no credit history, policymakers and fintech companies are pushing for broader adoption of alternative data.

- California’s SB 1040 encourages rent reporting to promote financial equity.

- Fannie Mae and Freddie Mac now accept VantageScore 4.0 for certain mortgages.

- Fintech lenders increasingly use trended data and alternative sources.

Experts predict that within the next decade, rental payment history will be standard credit data, just like a car loan or credit card.

Conclusion

Your rent payment is more than just a monthly expense—it’s proof of financial responsibility. And thanks to advancements at Experian, Equifax, and TransUnion, that responsibility can finally be recognized.

While the systems aren’t perfect, and not all renters are being reported equally, the tools exist to turn your rent into credit-building power. Whether you use Experian Boost, axcessrent, or work with your landlord to join a reporting program, the choice is yours.

Don’t let your on-time payments go unnoticed. Take control of your credit story by ensuring your rent is not just paid—but reported, verified, and counted.