what is debt consolidation ? How does it works ?

Introduction

Many people struggle with multiple debts from credit cards, loans, or medical bills. These debts can pile up, making it hard to keep track of payments and interest rates. Debt consolidation offers a way to combine these debts into one single payment, which might simplify your financial life. But a common question arises: does debt consolidation hurt your credit? The truth is, it can have both short-term and long-term effects on your credit score, depending on how you handle the process.

In this article, we’ll break down everything you need to know about debt consolidation and its impact on credit. We’ll start by explaining what debt consolidation is, then dive into how it affects your credit score factors. You’ll learn about the potential benefits and drawbacks, and get actionable advice on how to minimize any negative effects. By the end, you’ll have a clear understanding to decide if debt consolidation is right for you.

Statistics show that over 80% of Americans carry some form of debt, with credit card debt being the most common. High interest rates on these cards can make it feel like you’re running on a treadmill—paying but not getting ahead. Debt consolidation aims to break this cycle, but it’s crucial to approach it wisely to avoid damaging your credit.

What Is Debt Consolidation?

Debt consolidation is a financial strategy where you take out a new loan or use another method to pay off multiple existing debts. This leaves you with just one debt to manage, often at a lower interest rate or with more favorable terms. The primary goal is to make debt repayment easier and potentially save money on interest over time.

Imagine you have three credit cards: one with a $5,000 balance at 18% interest, another with $3,000 at 20%, and a personal loan of $2,000 at 15%. Keeping track of different due dates and payments can be overwhelming. With debt consolidation, you might get a single loan for $10,000 at 12% interest, use it to pay off the others, and then focus on one monthly payment.

This approach doesn’t erase your debt; it restructures it. It’s not a magic fix, but for those with good credit, it can lead to significant savings. However, if your credit is already poor, qualifying for a favorable consolidation loan might be challenging.

is debt consolidation a good idea ?

People opt for debt consolidation for several reasons. First, it simplifies budgeting. Instead of juggling multiple payments, you have one predictable amount each month. Second, it can reduce overall interest costs if the new rate is lower than the average of your current debts. Third, it might extend the repayment term, lowering monthly payments and easing cash flow—though this could mean paying more interest in the long run.

It’s important to note that debt consolidation works best when you’re committed to changing spending habits. Without discipline, you might end up accumulating new debt on top of the consolidated one.

Types of Debt Consolidation

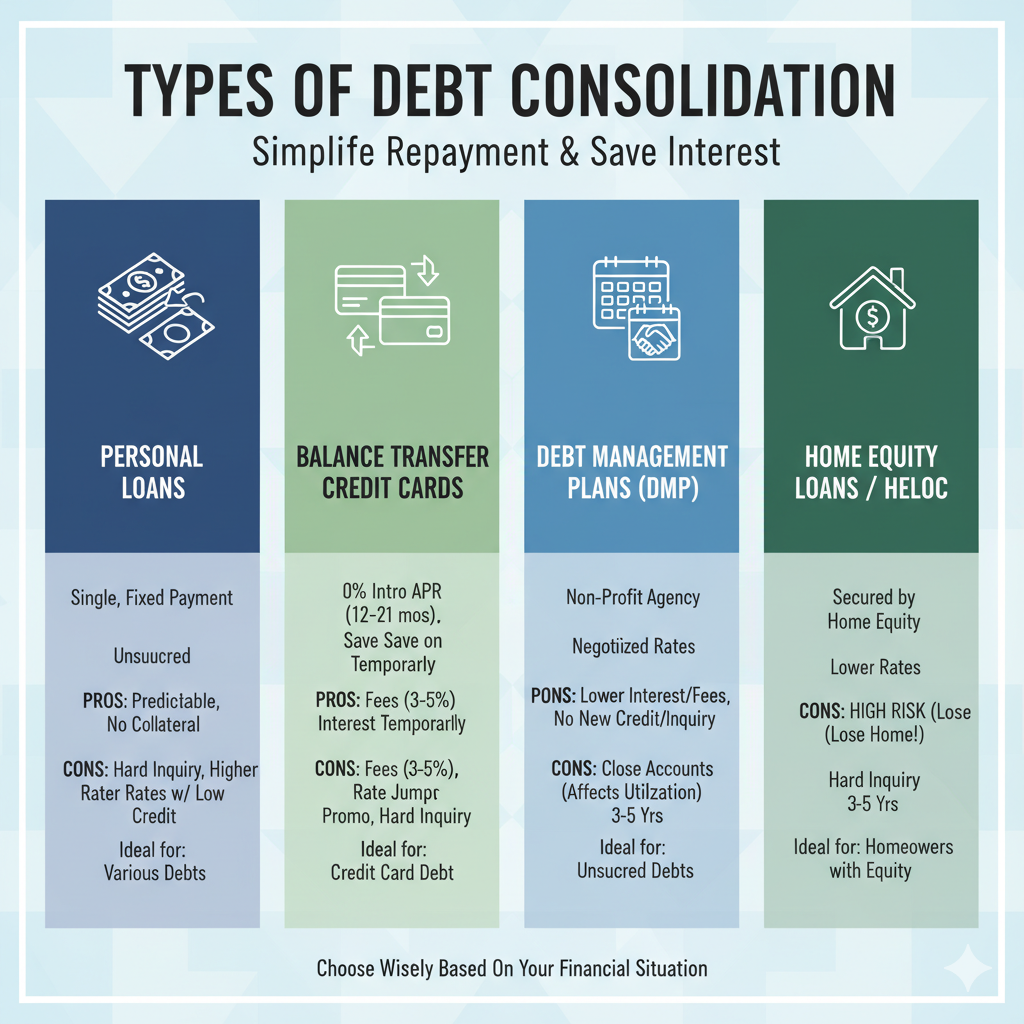

There are several ways to consolidate debt, each with its own mechanics, advantages, and potential credit implications. Choosing the right type depends on your financial situation, credit score, and the types of debt you have.

Personal Loans for Debt Consolidation

A personal loan is an unsecured loan from a bank, credit union, or online lender. You borrow a lump sum to pay off your debts, then repay the loan in fixed monthly installments over a set period, typically 2-5 years.

Pros include fixed interest rates, which provide payment stability, and no collateral required. Cons might involve higher rates if your credit isn’t strong. Applying for a personal loan involves a hard credit inquiry, which can temporarily ding your score by 5-10 points.

For example, if you have $15,000 in credit card debt at an average 19% APR, a personal loan at 10% could save you thousands in interest.

Balance Transfer Credit Cards

This method involves transferring high-interest credit card balances to a new card with a promotional low or 0% APR for a set period, often 12-21 months.

It’s ideal for credit card debt only. After the promo period, the rate jumps, so you need a plan to pay off the balance before then. Balance transfer fees (3-5% of the transferred amount) add to the cost.

Credit impact: Opening a new card means a hard inquiry and potentially higher utilization if you max out the new card. But paying down balances quickly can improve your score.

Debt Management Plans (DMPs)

Offered by nonprofit credit counseling agencies, a DMP involves negotiating with creditors for lower interest rates or waived fees. You make one monthly payment to the agency, which distributes it to your creditors.

DMPs are good for those with multiple unsecured debts. They don’t involve new credit, so no hard inquiries, but enrolling might require closing credit accounts, affecting utilization.

Agencies like the National Foundation for Credit Counseling can help set this up. It typically takes 3-5 years to complete, and while on the plan, you agree not to open new credit.

Home Equity Loans or Lines of Credit (HELOCs)

If you own a home, you can borrow against its equity. These secured loans often have lower rates because your home is collateral.

However, the risk is high—if you default, you could lose your home. Credit impact includes a hard inquiry and adding new debt. It’s best for those with substantial equity and stable income.

Other options like 401(k) loans exist but are riskier, as they can lead to taxes and penalties if not repaid.

how does debt consolidation affect your credit ?

Your credit score, calculated by models like FICO or VantageScore, reflects your creditworthiness. Debt consolidation can influence it in various ways, both positively and negatively. Let’s examine the key factors.

Understanding Credit Score Factors

- Payment history (35%): On-time payments are crucial.

- Amounts owed/credit utilization (30%): How much you owe relative to your credit limits.

- Length of credit history (15%): Longer is better.

- New credit (10%): Recent inquiries and accounts.

- Credit mix (10%): Variety of credit types.

Potential Negative Impacts Explained

Hard inquiries occur when lenders check your credit for a new application. Each can lower your score by 5-10 points, but they fade after 12 months and stop affecting scores after 24 months. If you apply for multiple loans, group them within 14-45 days to count as one inquiry.

Closing old accounts after payoff reduces your available credit, spiking utilization. For instance, if you had $10,000 in limits and $5,000 debt (50% utilization), closing cards drops limits to $0 for those, but the debt is paid, so overall utilization might improve if done right.

New debt from the consolidation loan increases your total debt initially, though it’s the same amount restructured.

Missed payments on the new loan are devastating, as they stay on your report for seven years.

Potential Positive Impacts Explained

Lowering credit utilization by paying off revolving debts like credit cards is a big win. Aim to keep utilization under 30%. For example, paying off $8,000 in cards with a loan drops utilization from 80% to 0% on those cards.

Simplified payments reduce the chance of late payments, bolstering your payment history.

Over time, consistent payments on the new loan add positive history, and diversifying your credit mix (adding an installment loan) can help.

Pros and Cons of Debt Consolidation

Detailed Pros

Lower interest rates: Switching from 20% credit cards to a 7% loan saves money. Calculate potential savings using online tools.

Simplified finances: One payment means less stress and fewer chances for errors.

Potential credit boost: As utilization drops and payments are made, scores can rise within months.

Faster debt payoff: Fixed terms encourage discipline.

Detailed Cons

Temporary credit dip: Inquiries and changes can lower scores short-term.

Risk of new debt: Cleared cards might lead to overspending. Studies show 30% of consolidators accumulate new debt.

Fees and costs: Loans may have origination fees (1-6%), balance transfers have fees.

Not for everyone: If rates aren’t lower, it’s pointless.

Scenarios: If you’re disciplined, pros outweigh cons. If not, it could worsen your situation.

Does Debt Consolidation Hurt Your Credit in the Long Run?

In the long term, debt consolidation is more likely to help than hurt if managed well. The initial impacts are fleeting—hard inquiries drop off, and positive payment history builds. Many see score improvements within 6-12 months.

However, if you miss payments or add debt, long-term damage ensues. Credit reports show the consolidation loan as new credit, but as it’s paid down, it becomes a positive mark.

Real-life examples: Someone with a 650 score might dip to 630 initially but climb to 700 after a year of on-time payments.

How to Minimize Credit Impact During Debt Consolidation

Protecting your credit requires strategy.

1. Shop Around Wisely

Use pre-qualification tools for soft inquiries first. Then, apply formally within the rate-shopping window.

2. Keep Old Accounts Open

Maintain limits to keep utilization low. Only close if fees are high.

3. Make Timely Payments

Automate payments and set reminders. Pay more than minimum to reduce debt faster.

4. Avoid New Debt

Cut up cards or freeze them in ice to prevent impulse spending.

5. Monitor Your Credit

Use free tools like Credit Karma. Dispute errors promptly.

Additional tips: Build an emergency fund to avoid relying on credit. Consider credit counseling for guidance.

When Is Debt Consolidation a Good Idea?

It’s suitable if you have high-interest unsecured debt, a steady income, and credit good enough for better terms. Calculate if the new payment fits your budget.

Signs it’s good: Debt-to-income ratio under 40%, commitment to no new debt.

Not ideal if debts are low-interest, you’re in financial crisis (consider bankruptcy), or can’t qualify.

Alternatives to Debt Consolidation

Debt Snowball Method

List debts smallest to largest, pay minimums on all but attack the smallest aggressively. Builds momentum.

Debt Avalanche

Prioritize highest interest first to save money.

Credit Counseling

Free advice, budget help.

Debt Settlement

Negotiate lumpsum payoffs for less, but hurts credit badly (scores drop 100+ points).

Bankruptcy

Last resort, erases debt but tanks credit for 7-10 years.

Choose based on your situation.

Case Studies: Real-Life Examples

Case 1: Sarah had $20,000 in credit card debt at 22% interest. She consolidated with a personal loan at 9%, paid off in 3 years, score rose from 680 to 750.

Case 2: John used a balance transfer but racked up new debt, score dropped.

These illustrate the importance of discipline.

Conclusion

Debt consolidation can be a smart move if it lowers costs and simplifies payments, but it might cause a short-term credit hit. By understanding the impacts, choosing the right method, and following best practices, you can minimize risks and potentially improve your credit over time. Assess your finances, perhaps consult a advisor, and take action if it fits. Remember, the key is long-term financial health.

Frequently Asked Questions (FAQs)

How Long Does a Hard Inquiry Stay on My Credit Report?

Two years, but affects score for one.

Can Debt Consolidation Help If I Have Bad Credit?

Options are limited, rates higher. Improve credit first.

What’s the Difference Between Consolidation and Settlement?

Consolidation restructures, settlement reduces amount owed.

Should I Use a Debt Consolidation Company?

Be cautious; some charge high fees. Use nonprofits.