Can I Report My Rent Payments to Credit Bureau or Does My Landlord Have To?

Every month, millions of renters across the U.S. make their rent payments on time. No reminders. No stress. Just another responsible financial decision done quietly in the background. But here’s the hard truth: unless that payment is reported to a credit bureau, it doesn’t help your credit score one bit.

For decades, this was the reality—your rent mattered to your landlord, but not to your financial future. That’s finally changing.

Today, rent reporting is becoming a mainstream way to build credit, especially for those who don’t use credit cards or loans. But a big question remains: Who should report your rent?

You might assume it’s your responsibility. Or maybe you’re hoping your landlord is already doing it for you. The truth is, there are two main paths, landlord managed vs renter initiated rent reporting—and each comes with its own strengths, limitations, and real-world impact.

Understanding the difference isn’t just about convenience. It’s about how much your credit improves, how fast it happens, and whether lenders actually recognize it when you apply for a car loan, mortgage, or credit card.

Let’s take a closer look at both models, how they work in practice, and which one might be the better fit for your life.

What Is Rent Reporting (And Why It Matters)

Before we compare the two models, let’s make sure we’re on the same page.

Rent reporting is the process of sending your rental payment history to one or more of the three major credit bureaus: Experian, Equifax, and TransUnion. When done correctly, it appears on your credit report just like a car loan or credit card payment.

Why does this matter?

- 45 million Americans are “credit invisible” — no credit file at all.

- Millions more have “thin” files — not enough history to qualify for loans.

- On-time rent is often their most consistent financial habit.

According to the Consumer Financial Protection Bureau (CFPB), including verified rent data can increase credit scores by 40–65 points—enough to move from “fair” to “good” credit and qualify for better interest rates.

Landlord-Managed Rent Reporting: How It Works

If you live in an apartment complex, workforce housing, or a property managed by a professional company, there’s a good chance your landlord is already reporting your rent—without you even knowing.

This is called landlord-managed rent reporting, and it works behind the scenes. The property owner or management team uses a platform like AxcessRent, RentTrack, or ClearNow to automatically send tenant payment histories to credit bureaus. All you have to do is pay on time.

The beauty of this system is its simplicity. You don’t need to sign up, link your bank account, or upload documents. If your landlord is using the service, your on-time payments start showing up on your credit report—like magic.

Common platforms used:

- AxcessRent

- RentTrack

- ClearNow

- AppFolio

- Yardi with integrated reporting

How It Works – Step by Step

- Your landlord signs up for a rent-reporting service.

- You pay rent as usual (via portal, check, or ACH).

- The system verifies the payment.

- Monthly, your payment history is sent to one or more credit bureaus.

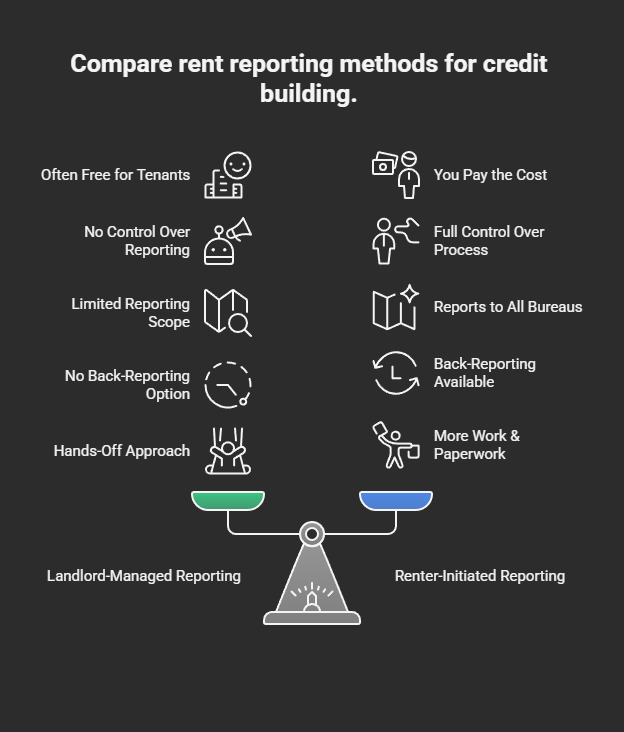

Pros of Landlord-Managed Reporting

It’s usually free for tenants. The cost is absorbed by the landlord, who may see value in attracting and retaining financially responsible renters. In affordable housing communities, rent reporting is increasingly being used as a tool for financial inclusion, helping low-income and underserved renters build credit where the traditional system has failed them.

But it’s not without limitations. The biggest drawback is lack of control. If your landlord doesn’t offer rent reporting, you can’t force them to start. And if they decide to stop using the service, your reporting stops too—no warning, no backup. You’re entirely dependent on their participation.

Also, not all platforms report to all three credit bureaus. Some only send data to Experian and TransUnion, leaving out Equifax. That means your full credit picture might still be incomplete, depending on which report a lender pulls.

And one more thing: these systems typically only report going forward. You can’t go back and report six or twelve months of on-time payments. What you gain is consistency over time—not an instant boost.

Pros

1. It’s Hands-Off : You don’t have to sign up, link your bank, or upload documents. If your landlord uses the service, you benefit automatically.

2. Higher Data Accuracy : Because the data comes directly from the landlord or payment processor, it’s considered more reliable and FCRA-compliant—a big deal for lenders.

3. Often Free for Tenants : Most landlords cover the cost, so you get credit-building power at zero cost to you.

4. Used in Large-Scale Properties : If you live in an apartment complex, workforce housing, or affordable units, your landlord is more likely to use a system like AxcessRent or RentTrack.

5. Trusted by Lenders : Since the reporting is institutional and verified, mortgage underwriters are more likely to recognize and accept it.

Cons

1. You Have No Control : If your landlord doesn’t offer it, you can’t force them to start. And if they stop, your reporting stops too.

2. Not All Landlords Participate : Only about 15–20% of landlords currently report rent. Individual or small landlords rarely do.

3. May Not Report to All Three Bureaus : Some services only report to Experian and TransUnion—missing Equifax, which can hurt your full credit picture.

4. No Back-Reporting Option : These systems usually only report going forward. You can’t add past on-time payments.

Real-World Example

Maria lives in a HUD-assisted apartment in Houston. Her landlord uses AxcessRent, and she didn’t even know her rent was being reported—until she checked her credit report and saw a +52 point increase in her credit score. No effort. No cost. Just results.

Renter-Initiated Rent Reporting: How It Works

This model puts you in the driver’s seat. You choose a third-party service—like Axcessrent PayYourRent, LevelCredit, Piñata, or Boom—and use it to report your own rent payments to the credit bureaus. You provide proof (usually bank statements and a lease), verify your landlord’s contact, and the service handles the rest.

It’s not automatic. It takes effort. But it gives you full control over the process.

One of the biggest advantages of this approach is back-reporting. Services like PayYourRent and LevelCredit allow you to report up to 24 months of past on-time payments, as long as you have the documentation. For someone with a thin or nonexistent credit file, this can be a game-changer—delivering an immediate boost that reflects years of responsible behavior.

How It Works – Step by Step

- You choose a rent-reporting service.

- Upload proof: lease agreement + 12 months of bank statements.

- Confirm your landlord’s contact (they may call to verify).

- The service begins reporting to one or more credit bureaus.

Pros

1. You Don’t Need Landlord Buy-In : Even if your landlord doesn’t report, you can still build credit.

2. Back-Reporting Available : Services like Axcessrent, PayYourRent and LevelCredit let you report up to 24 months of past on-time payments—a huge boost for thin-file users.

3. Full Control Over the Process : You choose when to start, stop, or switch services.

4. Reports to All Three Bureaus (Some Services) : PayYourRent and LevelCredit report to Experian, Equifax, and TransUnion—maximizing your credit file impact.

5. Great for Private Rentals : Ideal for renters with individual landlords, roommates, or non-traditional leases.

Cons

1. You Pay the Cost : Monthly fees range from $1.95 to $9.95, plus some have setup fees

2. More Work & Paperwork : You must upload documents, verify identity, and sometimes get landlord confirmation.

3. Verification Can Take Weeks : Some services take 2–4 weeks to verify and start reporting.

4. Not All Services Are Lender-Recognized : Free apps that don’t verify properly may boost your score temporarily—but lenders might ignore the data.

5. Risk of Inaccurate or Rejected Reporting : If your proof isn’t clear or your landlord doesn’t respond, the service may not report your rent.

Real-World Example

James rents a house from a private owner in Denver. His landlord doesn’t report rent, so James signed up for AxcessRent. He uploaded 18 months of bank statements, got his landlord to confirm by phone, and started reporting to all three bureaus. In 5 months, his FICO score rose from 610 to 678—enough to qualify for a car loan at 5.9% instead of 14.5%.

Side-by-Side Comparison: Landlord Managed vs Renter Initiated

| Features | Landlord managed | Renter Initiated |

|---|---|---|

| Who Controls It? | Landlord | You |

| Cost to Tenant | Usually free | $3.99–$9.95/month (or more) |

| Setup Effort | None | Moderate to high |

| Back-Reporting? | ❌ No | ✅ Yes (up to 24 months) |

| Bureau Coverage | Varies (often 2 of 3) | Varies (some do all 3) |

| Verification Level | High (direct source) | Medium to high |

| Lender Trust | High | Medium to high |

| Best For | Apartment complexes, managed housing | Private rentals, credit rebuilders |

Which One Is Better?

There’s no one-size-fits-all answer.

If you live in a professionally managed property and your landlord uses a system like AxcessRent or RentTrack, landlord-managed reporting is hands-down the better option. It’s free, automatic, and trusted by lenders. You get the benefit without lifting a finger.

But if you’re renting from a private owner, or your landlord doesn’t participate, renter-initiated reporting is your best—and often only—path to getting your rent on your credit report. Yes, it costs money and effort. But for many, it’s the only way to turn years of on-time payments into real financial progress.

The good news? You don’t always have to pick one. Some renters use both. For example, if your landlord reports to two bureaus, you might use a renter-initiated service to report to the third—or to add back-reported history for even greater impact.

Quick Takeaways

- Landlord-managed reporting is free, automatic, and trusted, but only available if your landlord participates.

- Renter-initiated reporting gives you control and flexibility, including the ability to report past payments.

- Both methods can boost your credit, but renter-initiated often costs money and requires effort.

- For maximum impact, aim for verified reporting to all three credit bureaus.

- Your rent is financial proof—don’t let it go to waste.

Conclusion

At the end of the day, both landlord-managed and renter-initiated rent reporting can build your credit. The real question isn’t which is “better”—it’s which is better for you.

If you’re lucky enough to have a landlord using AxcessRent ride that wave—your credit is growing while you sleep.

But if you’re on your own, don’t wait. Take charge with a trusted service like PayYourRent or LevelCredit and start claiming the credit you’ve already earned.

FAQs

Can I use both landlord-managed and renter-initiated reporting?

Yes, but avoid duplicates. Most bureaus will merge the data, but it’s best to coordinate.

Will rent reporting hurt my credit if I miss a payment?

Most services only report on-time payments, so you’re safe.

How long does it take to see a score increase?

Most users see changes within 30–60 days of reporting.

Do all lenders accept reported rent?

FICO Score 9 and VantageScore 4.0 include it. Older models may not.

Can I cancel rent reporting anytime?

Yes, but your reported history usually stays on your file.