5 Ways Credit Counseling Can Help You Buy a Home?

The journey to homeownership is often viewed through the lens of open houses and aesthetic renovations. However, for the millions of Americans navigating the “credit gap,” the reality is much more clinical. It is a world of FICO scores, Debt-to-Income (DTI) ratios, and the looming fear of a “denied” notification from a mortgage underwriter.

If your credit isn’t “mortgage-ready,” you don’t have to navigate the complex financial landscape alone. Professional credit counseling—specifically from HUD-approved housing counseling agencies—serves as a bridge between your current financial state and the keys to your new home.

What is Credit Counseling? (The Fundamentals)

To understand how it helps you buy a home, we must first define it. What is credit counseling? At its core, it is a service provided by non-profit organizations designed to help individuals manage their debt and improve their financial literacy.

Unlike “credit repair” companies that often use aggressive or borderline illegal tactics to “scrub” credit reports, consumer credit counseling services focus on education, budgeting, and structured repayment. These services are typically delivered by certified counselors who review your entire financial picture—income, expenses, and debt—to create a personalized roadmap.

Is Credit Counseling a Good Idea?

For most people, the answer is a resounding yes. It is an especially good idea if:

- You are struggling to make minimum payments.

- You want to buy a house but have been told your credit score is too low.

- You are overwhelmed by high-interest credit card debt.

- You need an official certificate for a Down Payment Assistance (DPA) program.

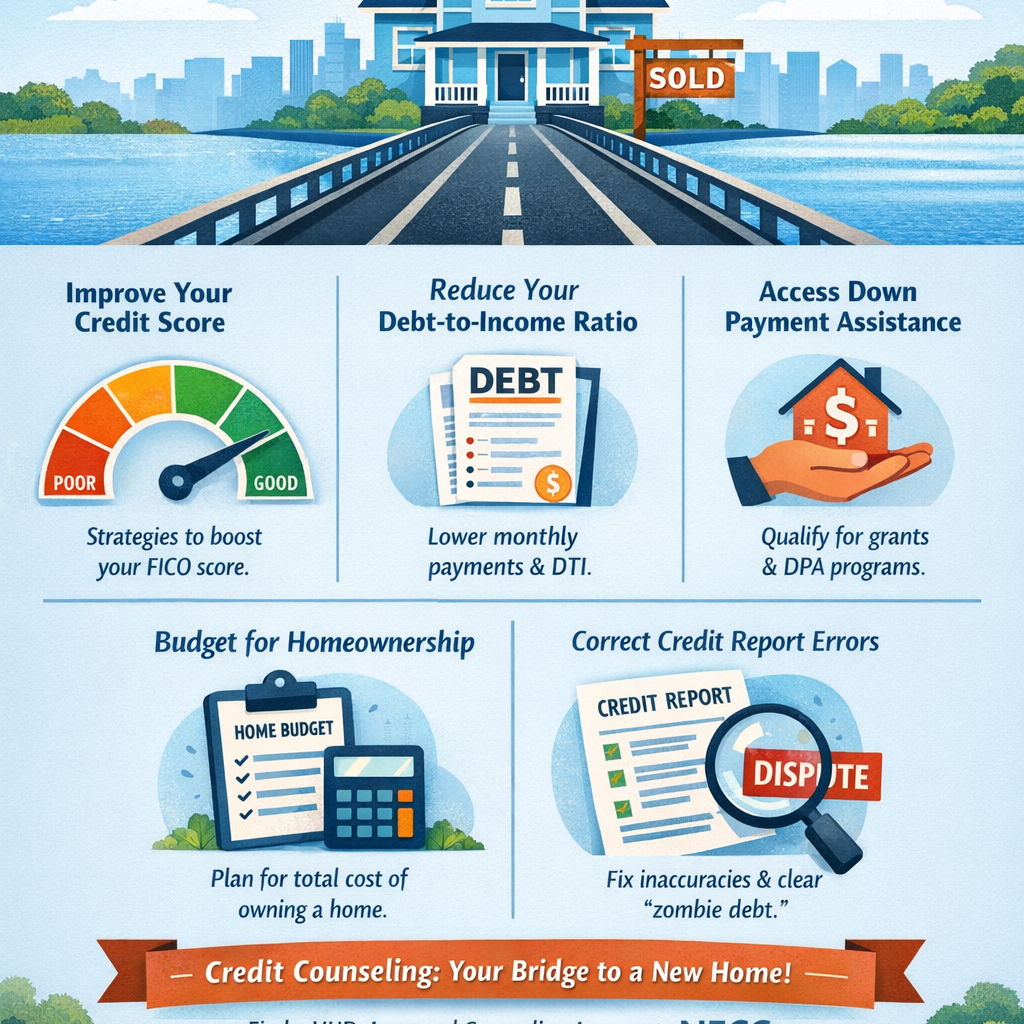

1. Precision Credit Score Optimization (The “Prime Rate” Strategy)

The single most significant barrier to homeownership is the credit score. While you can technically get a mortgage with a score in the 500s (via certain FHA products), the financial cost of doing so is staggering.

How Does Credit Counseling Work?

The process begins with a deep-dive analysis. A counselor pulls your credit report and identifies “score killers.” They look for high credit utilization, late payments, and collection accounts. Instead of just telling you to “pay your bills,” they provide a tactical sequence. For example, paying down a specific $500 balance might jump your score more than paying $1,000 across multiple cards due to how credit scoring models view individual card limits.

Does Credit Counseling Hurt Your Credit?

This is the most common concern. Does credit counseling hurt your credit? The act of meeting with a counselor and receiving advice has zero impact on your credit score. If you enter a Debt Management Plan (DMP), your score might experience a temporary dip if accounts are closed, but it typically rebounds quickly as your balances drop and your payment history becomes “perfect” under the plan.

2. Managing the Debt-to-Income (DTI) Ratio

Lenders are less interested in how much you earn and more interested in how much of that income is already “spoken for.” Most conventional loans require a DTI ratio below 36%.

How Does Consumer Credit Counseling Work?

When you work with a service like American Consumer Credit Counseling or Cambridge Credit Counseling, they often suggest a Debt Management Plan (DMP).

- They negotiate with your creditors to lower interest rates (sometimes from 29% down to 8% or even 0%).

- They consolidate your payments into one monthly draft.

- This reduces your monthly minimum payment, which immediately lowers your DTI, making you more attractive to mortgage lenders.

3. Unlocking Down Payment Assistance (DPA) and Grants

One of the best-kept secrets in real estate is the abundance of Down Payment Assistance (DPA) programs. Many states and cities offer grants that don’t need to be paid back.

What Does the Consumer Credit Counseling Service Offer?

Beyond debt management, these agencies offer Homebuyer Education Classes. These courses are a mandatory requirement for almost all DPA grants. By completing the course, you prove to the government and lenders that you understand the responsibilities of homeownership.

Who Would Best Benefit from Credit Counseling?

- First-time homebuyers with limited savings.

- “Middle-income” earners who are just slightly above the threshold for some programs but need a credit boost to qualify for others.

- Anyone who has experienced a “life event” (medical emergency or divorce) that temporarily damaged their credit.

4. The “Stress-Test” Budgeting for Total Cost of Ownership (TCO)

A mortgage lender tells you what you can borrow; a credit counselor tells you what you can afford.

How Much Does Credit Counseling Cost?

Many people ask, how much does consumer credit counseling service cost? * Initial Session: Usually free.

- Education Classes: Often $50 to $100.

- DMP Fees: If you enter a repayment plan, there is usually a small monthly administrative fee (typically $25–$50) which is capped by state law.

Compared to the thousands you save in interest, is credit counseling worth it? Mathematically, the ROI is usually 10x to 50x the cost of the service.

5. Navigating the Dispute Process and “Zombie Debt”

Credit reports are riddled with errors. According to the FTC, one in five consumers has an error that could be dragging their score down.

Is Consumer Credit Counseling Legit?

Yes, provided you choose the right agency. Is American Consumer Credit Counseling legit? Yes. Is Cambridge Credit Counseling legit? Yes. Both are established, non-profit organizations with high ratings. You should always look for agencies that are members of the National Foundation for Credit Counseling (NFCC).

Who Financially Supports the Consumer Credit Counseling Service?

This is a “Hard” question many ask to verify legitimacy. These agencies are funded by:

- Grants: From foundations and the government (HUD).

- Client Fees: Small, regulated fees for services.

- Fair Share Contributions: Creditors (banks) actually pay the agencies a small percentage of the money recovered because the agencies help banks get paid without having to go to collections.

Comparison: The DIY Path vs. The Counseling Path

| Feature | The DIY Homebuyer | The Counseled Homebuyer |

|---|---|---|

| Loan Type | Limited to FHA/Subprime | Full access to Conventional & Prime |

| Closing Costs | Paid out of pocket | Often offset by DPA grants |

| Credit Strategy | Guesswork | Data-driven optimization |

| Success Rate | Higher risk of default | 30% lower default rates (statistically) |

Frequently Asked Questions (FAQ)

What is the consumer credit counseling service?

It is a generic term for non-profit agencies that provide financial guidance. The most common “Consumer Credit Counseling Service” (CCCS) agencies are local branches of the NFCC network.

Does credit counseling work?

Yes. Studies by the Federal Reserve and HUD show that individuals who receive pre-purchase counseling have significantly higher credit scores and lower foreclosure rates than those who do not.

Can I buy a house while on a Debt Management Plan (DMP)?

Yes. Most lenders require you to be on the plan for at least 12 months with a perfect payment history and to receive a letter of support from your counselor.

Consumer credit counseling services can help you by:

- Stopping collection calls.

- Lowering interest rates on credit cards.

- Waiving late fees.

- Providing the required certificates for first-time buyer grants.

Summary: Is It Worth It?

If you are asking “is credit counseling worth it?”, consider this: A 100-point difference in your credit score can mean the difference between a 6% mortgage and an 8% mortgage. On a $300,000 house, that 2% difference costs you over $150,000 in interest over the life of the loan.

Spending $50 on a counseling session to save $150,000 is perhaps the single best financial investment a future homeowner can make.

Ready to start? Look for a non-profit agency via the NFCC website or the HUD.gov database. Your future home is waiting; make sure your credit is ready to meet it.