What is Debt Re-Aging? An Easy Guide to the 7-Year Credit Rule

For anyone grappling with old, unpaid bills, the clock is your friend. Debts are governed by strict timelines. They become time-barred (meaning a collector cannot sue you) and must eventually fall off your credit report.

Debt Re-aging is the predatory and often illegal practice of manipulating a debt’s age to restart these clocks. It’s a tactic used by debt collectors to illegally extend the time they can legally pursue payment from you and keep the negative entry damaging your credit score longer.

This article breaks down what re-aging is, why it is illegal, and the essential steps you must take to protect your rights under the law.

What is Re-Aging Debt?

Re-aging debt occurs when a creditor or debt collector falsely changes the Date of First Delinquency (DOFD) associated with a debt.

The DOFD is the single most important date for any debt. It marks the first time you missed a payment that led to the default, and it starts two separate, critical countdowns:

- The Credit Reporting Period: The time the debt can legally remain on your credit report (set by the Fair Credit Reporting Act, or FCRA).

- The Statute of Limitations (SOL): The time a debt collector has to sue you in court to force payment (set by state law).

When a collector re-ages a debt, they attempt to change the DOFD to a later date, effectively “rejuvenating” an old debt to appear new.

Why Do Collectors Re-Age Debt?

The motive is simple: old debt is worth less because it has less legal leverage. By re-aging the debt, the collector:

- Extends the FCRA Reporting Limit: They illegally keep the negative item on your credit report for more than seven years, pressuring you to pay to remove the mark.

- Resets the Statute of Limitations: They illegally reset the SOL clock, threatening you with a lawsuit that they are otherwise legally barred from filing.

The Two Critical Timelines

Understanding the difference between the FCRA reporting period and the state Statute of Limitations is key to protecting yourself.

1. The FCRA Credit Reporting Period (The 7-Year Rule)

The Fair Credit Reporting Act (FCRA) dictates that most negative information, including late payments, collections, charge-offs, and bankruptcies, must be removed from your credit report after a specific period:

- Seven Years: Most negative items (collections, charge-offs, late payments) must be removed from the date of the initial delinquency (DOFD).

- Ten Years: Bankruptcy filings can be reported for up to ten years from the filing date.

Under the FCRA, the DOFD cannot be changed. It is fixed from the first day you missed a payment that eventually led to a charge-off or collection status. Any attempt by a collector to reset this date is a violation of federal law.

2. The State Statute of Limitations (SOL)

The SOL is the legal time limit within which a debt collector can file a lawsuit against you to collect the debt.

- State-Specific: The SOL is set by state law and typically ranges from 3 to 10 years depending on your location and the type of debt (e.g., written contract vs. oral agreement).

- Time-Barred Debt: Once the SOL expires, the debt is considered “time-barred.” The collector can still call you and ask for money, but they cannot legally take you to court.

The Key Danger: Restarting the Statute of Limitations

While the FCRA reporting clock is fixed, the state SOL clock can sometimes be unintentionally restarted by the consumer through certain actions. This is often the goal of re-aging tactics.

How You Can Inadvertently Restart the SOL

In many states, the SOL clock restarts if the borrower does one of the following:

- Makes a Partial Payment: Making even a $5 payment on an old debt.

- Acknowledges the Debt: Sends a written communication to the collector admitting the debt is yours and you intend to pay it.

- Enters a Payment Plan: Agrees to a repayment schedule.

Warning: Unscrupulous collectors will aggressively try to solicit a small, “good faith” payment on old, time-barred debt. If you pay $1, the SOL resets, and they suddenly have several more years to sue you. Never make a payment on a time-barred debt.

Signs a Debt Has Been Illegally Re-Aged

Re-aging often appears as a discrepancy on your credit report. Watch for these red flags:

| Red Flag | Description | Legal Implication |

|---|---|---|

| New DOFD | The “Date of First Delinquency” field has been changed to a date that is clearly more recent than the actual default date. | Illegal FCRA violation. |

| Old Debt Resurfaces | A collection account that previously fell off your report suddenly reappears as a “new” account with a different collector. | Illegal FCRA violation. |

| Threat of Suit on Old Debt | A collector threatens a lawsuit on a debt that is clearly past your state’s Statute of Limitations. | Potential violation of the Fair Debt Collection Practices Act (FDCPA). |

| New Collection Date | A debt that originated five years ago has a “Date Opened” or “Date Reported” that is only three months old. | This is common (as debt changes hands), but the DOFD must remain the same. If the DOFD changes, it’s re-aging. |

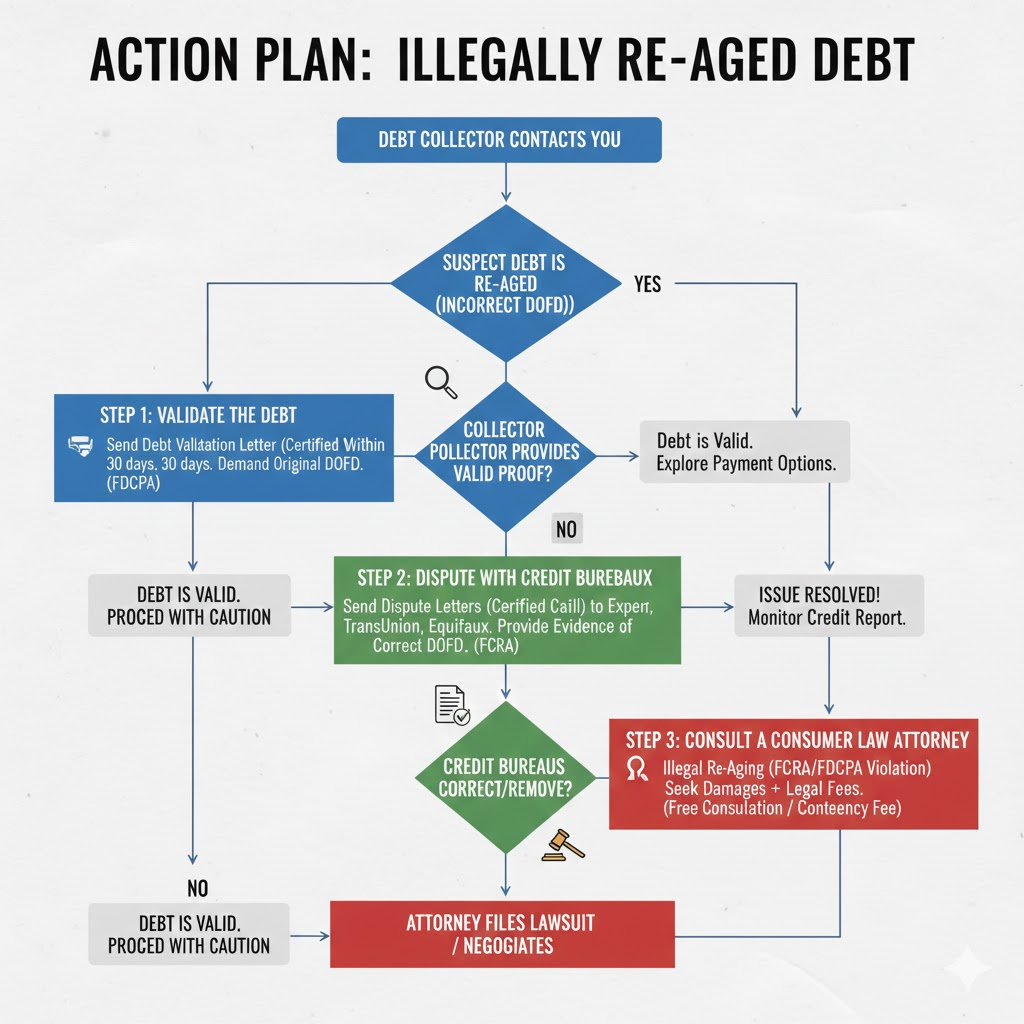

Action Plan: What to Do If Your Debt Is Re-Aged

If you suspect a debt collector has illegally re-aged your debt, you must act decisively to protect your legal and financial standing.

Step 1: Validate the Debt (The FDCPA Protection)

First, send the collector a Debt Validation Letter via certified mail (so you have proof of receipt) within 30 days of first hearing from them.

- Demand that they provide evidence of the debt, including the original Date of First Delinquency (DOFD).

- Under the FDCPA (Fair Debt Collection Practices Act), the collector must cease collection activity until they provide this proof.

Step 2: Dispute the DOFD with the Credit Bureaus

If the collector provides a DOFD that is different from your records, or if you simply see an incorrect DOFD on your report:

- Write a Dispute Letter: Send separate, certified letters to all three credit bureaus (Experian, TransUnion, and Equifax).

- Provide Evidence: State clearly that the account has been illegally re-aged and that the Date of First Delinquency is incorrect. Provide any documentation you have (like old statements) to support the original date.

- FCRA Mandate: The credit bureau has 30 days to investigate the dispute. If the creditor cannot verify the new (incorrect) DOFD, the entry must be corrected or removed.

Step 3: Consult a Consumer Law Attorney

If the collector or the credit bureaus refuse to correct the illegal re-aging, you have grounds for a lawsuit.

- FCRA Violations: An illegal re-aging of a debt is a direct violation of the FCRA.

- FDCPA Violations: Threatening to sue on a time-barred debt is a violation of the FDCPA.

Many consumer law attorneys offer free consultations and work on contingency, meaning they only get paid if they win your case. You could be entitled to statutory damages (up to $1,000 per violation) plus any actual damages.

Frequently Asked Questions (FAQ)

If I pay a debt, does it restart the FCRA 7-year clock?

No. Under the FCRA, the reporting clock is fixed from the DOFD and cannot be changed by payment, settlement, or acknowledgement. Paying a debt does not keep it on your credit report longer; the seven-year period runs regardless of subsequent activity.

Can a debt collector legally reset the Statute of Limitations?

Only if you take an action that resets it, such as making a payment or acknowledging the debt in writing. The debt collector cannot legally reset the SOL simply by selling the debt or reporting a new date.

How do I find the Statute of Limitations for my state?

You must check your specific state’s laws. A quick online search for “[Your State] Statute of Limitations Debt” will provide the current applicable timeframes for different types of debt (e.g., written contracts, verbal agreements, promissory notes).

What is the difference between a charge-off date and a DOFD?

The Date of First Delinquency (DOFD) is when the late payment cycle started. The Charge-Off Date is usually six months later, when the original creditor legally gives up on collecting the debt. The FCRA clock begins ticking from the DOFD, not the Charge-Off date. Always focus on the DOFD.