Red Flags That Lenders Look for on Your Credit Report in 2025

Introduction

Lenders rely heavily on your credit report when deciding whether to approve you for loans—be it for a mortgage, car, or personal credit. This report provides a detailed snapshot of your financial behaviors and history. Lenders scan it for warning signs, or red flags, that suggest you might struggle to repay. In 2025, regulatory changes push for fairer lending and faster error corrections, making it easier yet still crucial to maintain a clean credit profile. Recognizing these red flags and proactively fixing them significantly improves your chances of loan approval and better interest rates.

What Is a Credit Report and Why Do Lenders Care?

A credit report is essentially your financial report card. Compiled by bureaus like Equifax, Experian, and TransUnion, it consolidates information on your credit accounts, payment timeliness, current debts, and public records. Lenders use this data to estimate your creditworthiness. A report free of problems signals reliability, so lenders offer better terms such as lower interest rates. In contrast, reports dotted with negative marks raise concern, often resulting in higher rates or outright denials. Credit scoring models like FICO emphasize payment history (35%) and amounts owed (30%), meaning mistakes or missteps in these areas can drastically impact your score. Notably, red flags usually remain visible on reports for seven years, underscoring the long-term consequences of credit mismanagement.

Top Red Flags on Your Credit Report

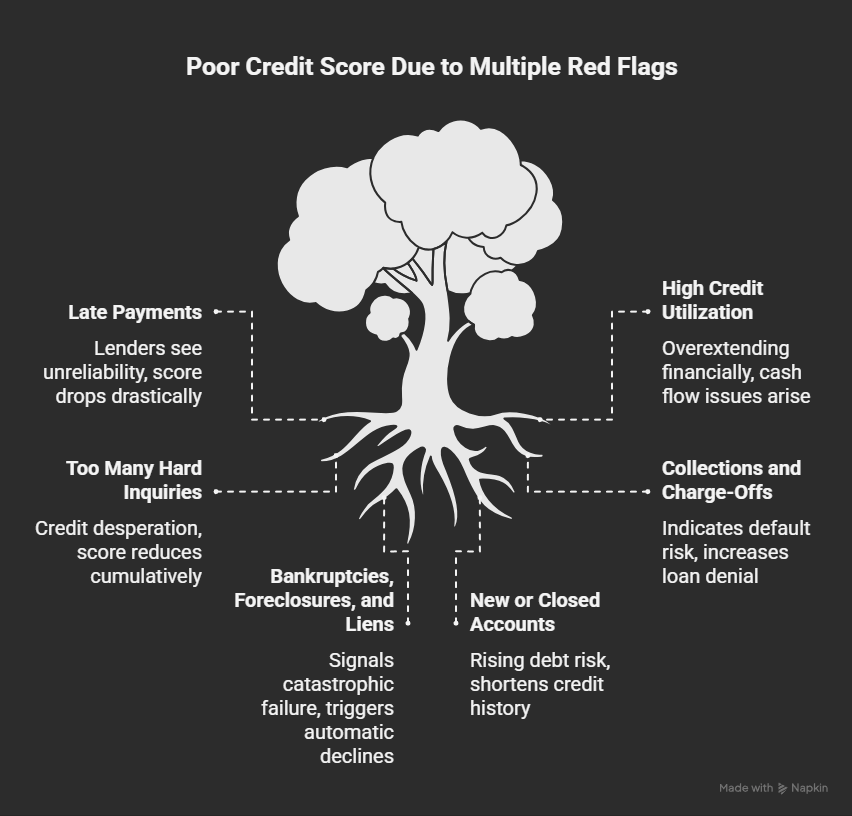

Late or Missed Payments

Late payments top the list of red flags because lenders view them as clear evidence of unreliability. Even one payment 30 or more days late can cause your credit score to plummet by as much as 110 points. Multiple late payments compound the damage drastically. Since payment history makes up over a third of your score, these marks are both damaging and persistent, remaining for seven years. Lenders are especially sensitive to recent late payments, often rejecting mortgage applicants with even a single late payment within the past year. Setting up autopay and communicating with creditors for goodwill adjustments are effective fixes.

High Credit Utilization

Your credit utilization ratio reflects how much of your available credit is currently used. Utilization above 30% signals to lenders that you may be overextending financially. For example, carrying a $4,000 balance on a $10,000 limit equates to 40% utilization—a clear caution sign. High utilization not only lowers your credit score (often by 50 points or more) but also signals potential cash flow issues that worry lenders. The 2025 trend is that lenders increasingly scrutinize utilization patterns over time, reinforcing the need to keep balances low consistently. Paying down debt and requesting increased credit limits without increasing spending are recommended strategies.

Too Many Hard Inquiries

A hard inquiry occurs whenever you apply for new credit, and these inquiries stay on your report for two years. Five or more hard inquiries within a short time raise red flags about credit desperation or over-borrowing. Each inquiry may reduce your score by 5 to 10 points, cumulatively harming your creditworthiness. However, credit shopping within a 14 to 45-day window is counted as a single inquiry to reduce impact. To protect your score, limit applications and prequalify when possible.

Collections and Charge-Offs

Accounts that have gone to collection agencies or have been charged off represent serious financial distress. Not only do they stay on your report for up to seven years, but they also negatively influence lenders’ perceptions. Collections indicate default risk and greatly increase the chance of loan denial, especially for auto and personal loans. Settled accounts are less damaging but still exert negative pressure. Timely negotiation of pay-for-delete agreements or settlements can aid in mitigating damage.

Bankruptcies, Foreclosures, and Liens

These marks are the worst kinds of financial red flags due to their severity and length of impact. Chapter 7 bankruptcies stay on credit reports for ten years, while foreclosures and liens generally last seven. They signal catastrophic financial failure, triggering automatic declines or requiring long recovery periods before mortgage approval—typically seven years clean after bankruptcy. Paying off liens and addressing tax judgments is crucial because unresolved liens remain a serious credit concern.

New or Closed Accounts

Sudden spikes in new credit accounts or closing older accounts both negatively influence your credit score. New accounts suggest rising debt risk, while closing accounts shortens your credit history, which comprises 15% of your score. Lenders prefer applicants with stable, older credit lines that demonstrate long-term responsible behavior. Monitor new credit openings carefully and avoid closing your oldest accounts if possible.

Thin or No Credit File

About 45 million Americans have little to no credit history, rendering them “credit invisible.” Without enough data, lenders cannot assign a credit score, resulting in difficulty getting loans. Building credit via authorized user status on a family member’s account or using secured credit cards is essential to develop a file and become loan-eligible.

How Red Flags Affect Your Loan Approval

The presence of one red flag might be manageable for smaller loans, but accumulating multiple flags sharply reduces approval chances. Mortgages require credit scores above 620, and loans backed by government programs like FHA are picky about late payments. Auto loan rates rise by 2-3% with high utilization, increasing borrowing costs. Personal loans often deny applicants with collections. Interest rates can essentially double, costing you thousands over a loan’s life. AI-powered credit analysis tools adopted in 2025 detect these flags faster and with greater accuracy, making remediation and monitoring more vital than ever.

How to Spot and Fix These Red Flags

Regularly accessing your free weekly credit reports from AnnualCreditReport.com for all three bureaus lets you catch red flags early. Disputing errors promptly online or by mail ensures quicker corrections, typically within 30 days. To fix late payments, enroll in autopay and request goodwill removals from creditors after demonstrating consistent payments. Lower credit utilization by paying down balances and asking for credit limit increases without increasing spending.

Limit credit applications and use prequalification tools to minimize hard inquiries. Negotiate collections pay-for-delete or settle debts to improve your standing. After bankruptcy, rebuild credit cautiously with secured cards and monitored usage. Tools like Credit Karma help track credit health continuously. Patience is key, as six months of clean credit behavior can lead to substantial improvements.

2025 Changes to Watch in Credit Reporting

Recent CFPB reforms drastically reduce the impact of medical debt by removing most of it from credit reports and accelerating removal of paid bills, giving consumers a credit score boost. Expanded rent payment reporting provides an additional positive credit stream that offsets some negatives. Fair lending oversight is stronger, requiring lenders to consider credit fixes and dispute resolutions more fairly. The introduction of FICO 10 shifts focus toward credit trends rather than historic delinquencies, benefiting borrowers who are rehabilitating credit. Staying current by reviewing CFPB updates and credit bureau communications monthly helps you adapt your credit strategies proactively.

Conclusion

Credit report red flags like late payments, high utilization, collections, and too many inquiries signal risk to lenders and can turn down your loan application. Recognizing these issues early and fixing them through disciplined payment habits, strategic credit use, and timely dispute processes is essential. Thanks to evolving 2025 regulations and credit monitoring tools, maintaining a healthy credit profile is easier and more transparent than ever. Take action today—clearing even one red flag brings you closer to better credit approvals, lower rates, and financial peace of mind.

FAQs

What is the biggest red flag on a credit report?

Late payments are the most damaging, making up 35% of the FICO score and staying on your report for seven years.

How long do red flags stay on my credit report?

Most negative marks, like late payments and collections, stay for seven years. Bankruptcies last up to 10 years.

Can I remove accurate red flags?

No. You can only dispute errors or build positive credit habits to offset them over time.

Do soft inquiries count as red flags?

No, soft inquiries don’t affect your credit score or appear to lenders in the same way hard inquiries do.

How do I get my credit report for free?

In 2025, you can pull free reports weekly from all three major bureaus at AnnualCreditReport.com.