My Credit Score Dropped for No Reason — Common Hidden Causes Revealed

If you’ve ever opened your credit app and noticed your credit score dropped — sometimes by 50 or even 100 points — without any warning, you’re not alone. It’s unsettling, especially when you’ve been paying your bills on time and keeping your balances low.

But here’s the truth: credit scores don’t just fall “for no reason.” There’s always a cause — it just might not be obvious at first. Understanding what triggered the drop is the first step toward getting your score back where it belongs.

This guide explains why your credit score might drop suddenly, how to find out what caused it, and what you can do to recover quickly.

Why Your Credit Score Dropped — Even If You Did Nothing Wrong

Credit scores react to data updates on your credit report. Even a small change — like a balance increase or a new account — can trigger a noticeable shift.

Let’s look at the most common reasons people see an unexplained score drop.

1. Your Credit Utilization Went Up

Credit utilization — the percentage of available credit you’re using — makes up about 30% of your credit score.

If your credit card balance suddenly increases, even if you haven’t missed a payment, your score can drop.

Example:

If you had a $1,000 credit limit and used $200 (20%), you were in great shape.

But if you spent $700 this month (70%), your utilization ratio shot up, which may cause your score to dip.

Quick fix:

Pay down your balance below 30% of your limit — ideally below 10%. Once the lower balance is reported, your score should rebound quickly.

2. A New Credit Inquiry Appeared

Every time you apply for credit — a credit card, auto loan, or mortgage — a hard inquiry hits your report.

Each inquiry can shave a few points off your score, and multiple applications in a short period can cause a bigger drop.

Why this happens:

Lenders see frequent credit applications as a sign of risk, assuming you may be taking on more debt.

What to do:

Only apply when necessary. The good news is inquiries lose impact after a few months and drop off your report completely after two years.

3. An Old Account Was Closed

Closing an old credit card, even one you never use, can hurt your score.

Here’s why: it affects both your credit utilization (less total available credit) and your credit age (the average age of all accounts).

Example:

If you close a card with a $5,000 limit, your available credit decreases — pushing your utilization up.

Tip:

Keep your oldest accounts open, even if you rarely use them. A small monthly purchase and automatic payment can keep them active.

4. A Payment Was Reported Late

Sometimes, a single missed or late payment can cause a major drop — even if it’s only a few days overdue.

Credit bureaus record payments as “late” once they’re 30 days past due.

How it happens unexpectedly:

- Auto-pay failed.

- Bank transfer didn’t go through.

- Payment posted after the cutoff time.

What to do:

If you realize a payment is late, call your creditor immediately. Many lenders will remove a late mark if you have a good payment history.

5. Your Credit Mix Changed

Credit scoring models reward borrowers who manage different types of credit — such as installment loans and credit cards.

If you paid off a car loan or student loan, your mix might look less balanced now, causing a temporary dip.

Don’t panic:

This type of drop is harmless. It usually stabilizes after a few months, and your good payment history will continue to benefit you.

6. Your Credit Report Updated With New Data

Sometimes a credit score changes because of data timing, not behavior.

Creditors report balances and payments at different times of the month. If a report update lands right before your payment clears, it may temporarily show a high balance.

Solution:

Check your score again after your billing cycle closes. Many temporary dips correct themselves automatically.

7. A Derogatory Mark Was Added

If your score suddenly plummets by 100 points or more, it might be due to a new derogatory entry — such as:

- A collection account

- A charge-off

- A public record (like a judgment)

These events severely impact credit, even if they were added in error.

Action plan:

- Get a free credit report from Experian, Equifax, or TransUnion.

- Identify any unfamiliar accounts or negative entries.

- File a dispute if something is incorrect.

How to Find Out Exactly Why Your Score Dropped

When your credit score changes, you can’t fix it without understanding why.

Here’s how to find the real reason:

Step 1: Check All Three Credit Reports

Visit AnnualCreditReport.com — the only official free source — and download your reports from Equifax, Experian, and TransUnion.

Compare them side by side. Look for:

- New accounts you didn’t open

- Late payments

- Balance increases

- Closed or inactive accounts

Step 2: Review Your Credit Alerts

Most credit monitoring tools will flag score changes and explain what caused them — such as “credit utilization increased” or “new inquiry added.”

Step 3: Identify Errors or Fraud

If something looks off, it might not be your fault. Credit reporting errors are common.

You can dispute inaccurate information with the bureau or creditor directly.

How Long Does It Take to Recover After a Drop?

It depends on what caused the decline.

| Cause | Typical Recovery Time |

|---|---|

| Increased balance | 1–2 months |

| Hard inquiry | 3–6 months |

| Closed account | 3–6 months |

| Late payment | 6–12 months |

| Collection or charge-off | 12–24 months (with consistent on-time payments) |

In most cases, the drop is temporary. Credit scores are dynamic and recover with good habits over time.

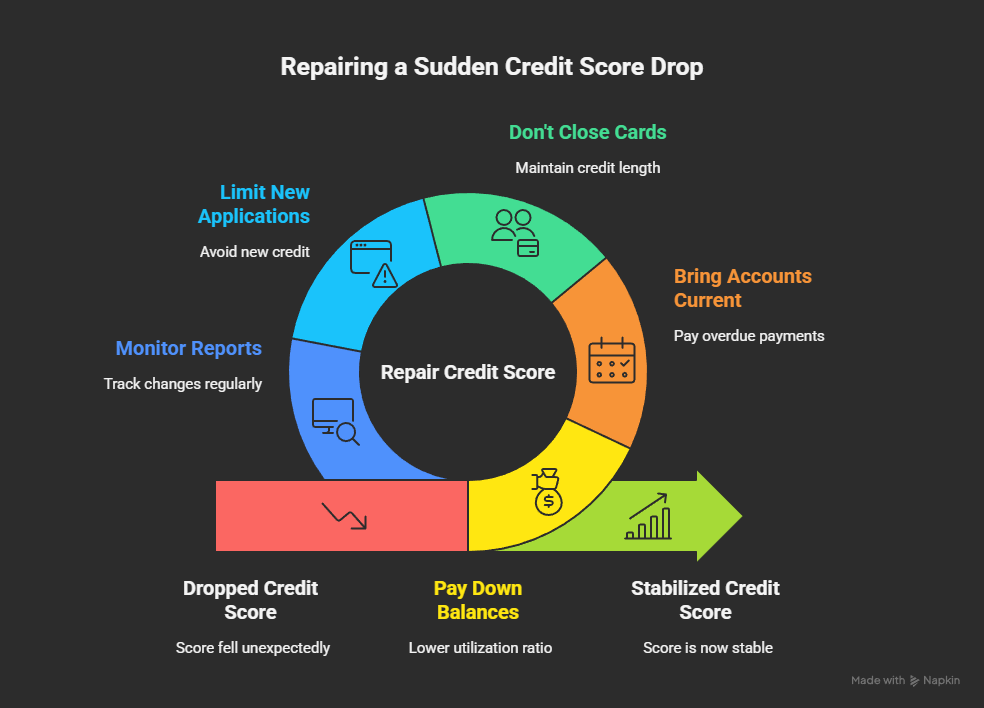

How to Fix a Sudden Credit Score Drop

If your credit score just fell, here’s what you can do to turn things around fast.

1. Pay Down Balances

Lower your utilization ratio to under 30%.

Even paying down a few hundred dollars can make a visible difference.

2. Bring All Accounts Current

If any payments are overdue, pay them immediately. Lenders prefer recent good behavior over older mistakes.

3. Don’t Close Credit Cards

Keep your oldest cards open to maintain credit length and available limits.

4. Limit New Applications

Avoid applying for new credit until your score stabilizes.

5. Monitor Your Reports Regularly

Use a credit monitoring service or your bank’s free tools to track changes.

If something suspicious appears, take action right away.

Why Your Credit Score Dropped After Opening a New Credit Card

This is one of the most common “mystery” score drops.

When you open a new card:

- You get a hard inquiry (minor score hit)

- Your average account age drops (temporary effect)

If you charge a balance right away, your utilization ratio may also spike.

But here’s the good news: within a few months, the new account can help you by increasing your overall available credit — improving your utilization long-term.

Why Your Credit Score Might Drop Even After Paying Off Debt

It seems unfair, but it happens.

When you pay off a loan, your credit mix may change. Closing the account reduces your active credit history.

Your score may drop slightly, but this is usually short-lived. Keep making on-time payments on your remaining accounts to maintain stability.

Can My Score Drop Even If I Did Everything Right?

Yes — and it doesn’t always mean something’s wrong.

Credit scores fluctuate naturally based on how lenders report data. Even if you’re managing credit perfectly, your score can move a few points each month.

Focus on long-term patterns, not daily changes.

How to Rebuild After a 100-Point Drop

A 100-point fall can feel huge, but it’s recoverable.

Here’s a step-by-step plan:

- Identify the cause. Check all reports for new marks or balance increases.

- Catch up on missed payments. Bring accounts current.

- Pay down high balances. Target credit cards with utilization over 50%.

- Add positive history. Use a secured card or rent reporting to rebuild credit.

- Avoid new credit. Let your score heal naturally over time.

Frequently Asked Questions

Why did my credit score drop 100 points for no reason?

A 100-point drop usually means a major event — like a new collection, late payment, or maxed-out card — hit your report.

Can my credit score drop without notice?

Yes. Creditors report data at different times, and new information can update your score unexpectedly.

How do I find out what caused my credit score to drop?

Get your full reports from all three bureaus and look for any changes, such as new inquiries, closed accounts, or negative marks.

Will my credit score go back up on its own?

In most cases, yes. If the cause was temporary — like a balance increase — your score will recover after your next statement cycle.

What should I do if I spot a mistake?

Dispute the error immediately with the credit bureau that reported it. They must investigate within 30 days.

Conclusion

Your credit score is sensitive to even small changes. When it drops suddenly, it’s natural to panic — but the solution is almost always within reach.

Start by reviewing your reports, understanding what triggered the change, and taking quick, focused action.

Most importantly, remember: credit recovery is a process, not a punishment. Every on-time payment, reduced balance, and positive update helps you rebuild your score — one step at a time.