Investment Risk Tolerance Explained: Know Your Limits

Investment risk tolerance is not a static number; it is a fluid psychological and financial boundary that shifts as you move through different seasons of life. Whether you are a fresh graduate entering the workforce or a professional eyeing the finish line of retirement, your ability to endure market volatility is governed by two distinct factors: your financial capacity to take risks and your emotional willingness to do so.

In the world of wealth management, the golden rule remains: Know your limit and invest within it. This guide explores the pivot points of risk tolerance, identifying when you are at your most aggressive and when the tides turn toward preservation.

When Do You Have the Highest Investment Risk Tolerance?

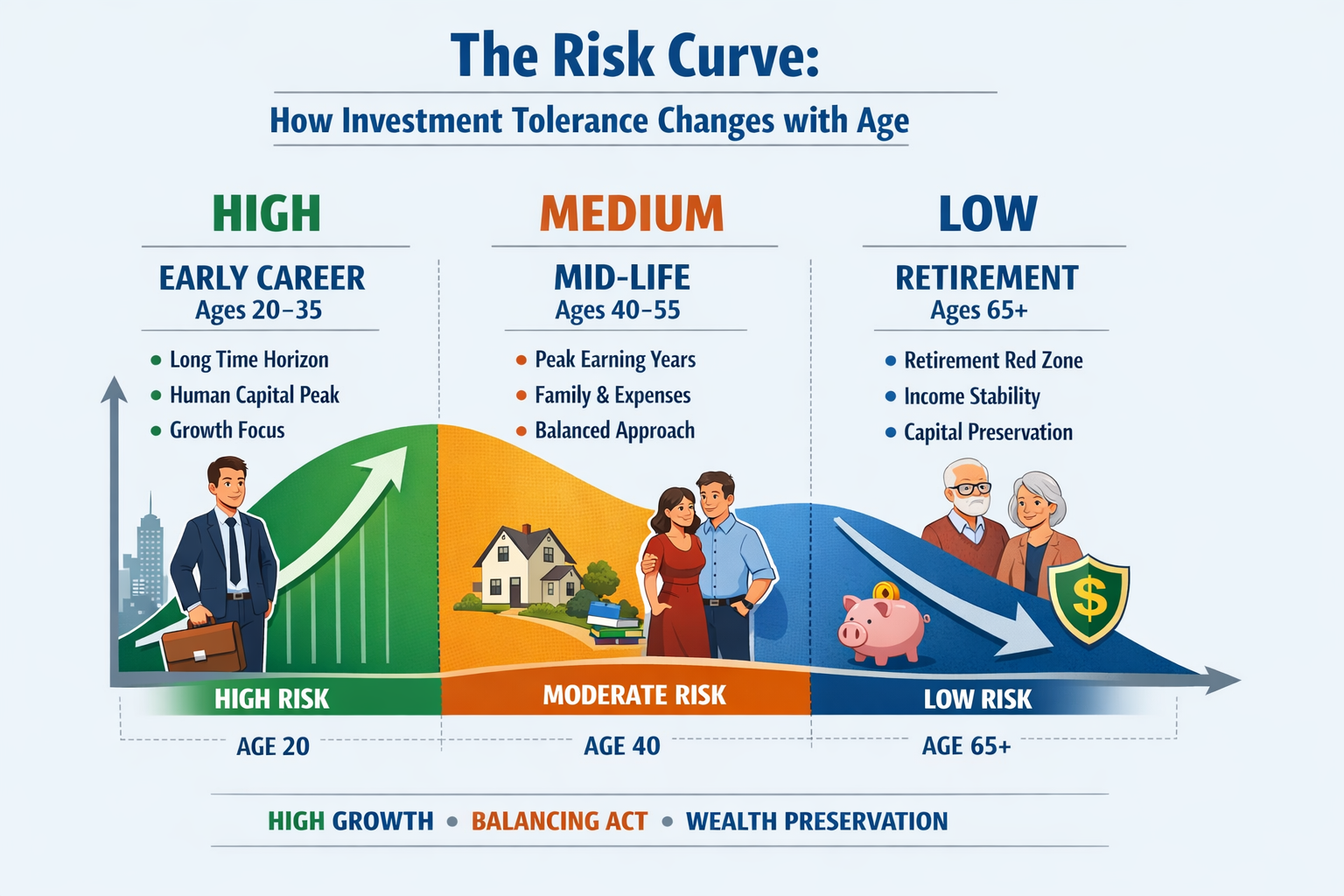

Statistically and psychologically, your highest risk tolerance typically occurs during your Early Career Phase (Ages 22–35). This is the period often referred to as the “Accumulation Phase,” and for several structural reasons, this is when you can—and often should—embrace the highest levels of market volatility.

1. The Power of Time Horizons

The single greatest asset a young investor possesses is time. When your retirement date is 30 or 40 years in the future, short-term market crashes (even those as severe as the 2008 financial crisis or the 2020 flash crash) become mere “blips” on a long-term upward trajectory. You have the luxury of waiting for the market to recover. High risk at this stage isn’t reckless; it is a strategic utilization of a long horizon to capture the higher historical returns of equities over bonds. This is why time in the market consistently outperforms market timing and why long-term investing principles remain the foundation of successful portfolios, as explained in this guide to building wealth through investing

2. Human Capital vs. Financial Capital

At the beginning of a career, future earning potential, often called human capital, is far greater than current savings. Because income will continue for decades, young investors can afford short-term losses. This is also why having a strong emergency fund before taking on higher-risk investments is critical, as outlined in this emergency fund guide.

3. Compounding Interest

High risk tolerance in youth allows for a heavier tilt toward growth stocks and emerging markets. Because compounding works exponentially, taking higher risks early on to achieve an 8% return versus a 4% return can result in a difference of hundreds of thousands of dollars by age 65.

When Do You Have the Lowest Investment Risk Tolerance?

Conversely, you typically have the lowest investment risk tolerance in the “Retirement Red Zone”—the five years immediately preceding and the five years immediately following your retirement date.

1. Sequence of Returns Risk

If markets fall sharply during the early years of retirement while withdrawals are taking place, the damage to a portfolio can be permanent. This risk makes aggressive investing dangerous at this stage and explains why understanding typical retirement savings benchmarks by age is essential when planning this transition.

2. Shift from Accumulation to Distribution

Once you stop receiving a paycheck, your portfolio changes from a “savings account” to a “pension.” You no longer have the “Human Capital” to go back and earn more money to replace investment losses. Preservation becomes the primary objective. At this stage, a 10% loss is much more painful than a 10% gain is pleasurable—a psychological phenomenon known as loss aversion. This is where understanding Roth versus traditional retirement accounts can significantly improve long-term outcomes, as discussed in this Roth IRA resource.

3. Inflation Protection vs. Capital Preservation

While risk tolerance is low, it cannot be zero. Even at this stage, investors must balance the fear of market loss with the risk of “purchasing power loss” (inflation). However, the overall “limit” is significantly lower than in previous decades. Holding all assets in cash exposes retirees to inflation risk, which slowly erodes purchasing power over time, a concept clearly explained by Investopedia’s inflation overview.

The “Medium” Ground: The Mid-Life Balancing Act

Between the ages of 40 and 55, most investors fall into the Medium Risk Tolerance category. This is often the most complex phase of financial planning because you are balancing “conflicting goals.”

- Peak Earning Years: You are likely making more money than ever before.

- High Expenses: You may be paying for a mortgage, children’s university tuition, and perhaps caring for aging parents.

- The Shrinking Horizon: Retirement is no longer a theoretical concept; it is a decade or two away.

A balanced strategy often works best during this stage, combining stable core investments with selective growth opportunities. Budgeting frameworks such as zero-based budgeting can help investors maintain discipline while managing multiple financial goals, as explained here: https://axcessrent.com/what-is-zero-based-budgeting/.

How to Calculate Your Personal Limit

Understanding the theory of risk is different from experiencing it. To truly “invest within your limit,” you must evaluate three specific dimensions:

I. Financial Capacity (The “Can”)

This is objective. If the market dropped 40% tomorrow, would you still be able to pay your mortgage? If the answer is no, your risk tolerance is low, regardless of your age. Your capacity is determined by your debt-to-income ratio, the size of your emergency fund, and the stability of your career.

II. Emotional Temperament (The “Will”)

This is subjective. How did you feel during the last market downturn? Did you check your accounts every hour and feel a pit in your stomach? If market volatility keeps you awake at night, you have a low emotional risk tolerance. It is better to have a conservative portfolio you can stick with than an aggressive one you sell in a panic at the bottom of a cycle.

III. Knowledge and Experience

Investors with a strong understanding of market cycles are less likely to panic during volatility. Learning how investment risk works and why volatility is normal can significantly improve long-term decision-making, as explained by Investor.gov: https://www.investor.gov/introduction-investing/investing-basics/investment-risk.

Considerations for Modern Investors

In today’s global economy, “knowing your limit” also involves understanding Geographical Diversification. Investing within your limit in 2025 and 2026 means recognizing that “Home Bias”—the tendency to invest only in your own country’s stock market—is itself a risk.

Optimizing your portfolio involves:

- Exposure to Emerging Markets: Higher risk, but necessary for growth in a stagnant domestic economy.

- Currency Risk Awareness: Understanding how a strong or weak local currency affects your international holdings.

- Regulatory Environments: Knowing the “limit” of your investments based on the political stability of the regions where those companies operate.

Conclusion: The Lifecycle of a Limit

Your risk tolerance is not a “set it and forget it” metric. It is a biological and economic evolution.

- Age 20–35: High Tolerance. Focus on massive growth and global equities.

- Age 35–55: Medium Tolerance. Focus on balanced portfolios and tax-advantaged accounts.

- Age 55+: Low Tolerance. Focus on income generation, bonds, and capital preservation.

By understanding where you stand on this timeline, you can avoid the two greatest mistakes in investing: being too conservative when you have time on your side, and being too aggressive when you don’t. Know your limit, stay within it, and let the math of the markets work in your favor.

Frequently Asked Questions (FAQs)

1. Can a person have a high risk tolerance even if they are close to retirement?

Yes, but only if their financial “capacity” is extremely high. If an individual has a nest egg that far exceeds their lifestyle needs—meaning a 50% market drop would still leave them with enough to live comfortably—they may choose to maintain a high-risk profile for legacy planning or charitable giving.

2. What is the difference between risk tolerance and risk capacity?

Risk tolerance is your psychological comfort level with market swings (the emotional “will”). Risk capacity is the objective ability of your financial situation to withstand a loss (the financial “can”). Ideally, your investment strategy should be based on the lower of the two.

3. How often should I re-evaluate my risk limit?

A good rule of thumb is to review your risk tolerance annually or whenever a major life event occurs, such as marriage, the birth of a child, a significant career change, or inheriting a large sum of money.

4. Does having a “Low Risk” profile mean I should put all my money in a savings account?

No. Even low-risk investors need to account for inflation risk. If your money earns 1% in a bank account while inflation is 3%, you are guaranteed to lose purchasing power. A low-risk portfolio usually includes a mix of high-quality bonds, dividend-paying stocks, and inflation-protected securities.

5. Why do experts say young people have the “highest” risk tolerance?

Because they have the most “time capital.” They can afford to ignore market downturns for 30 years. Additionally, their future earnings (human capital) act as a massive safety net that older investors no longer possess.

6. Can I increase my risk tolerance through education?

Absolutely. Behavioral finance shows that “fear of the unknown” is a major driver of low risk tolerance. By learning how markets historically behave and understanding that volatility is not the same as permanent loss, many investors become more comfortable with aggressive strategies.

7. What happens if I invest beyond my limit?

You will likely engage in “panic selling.” When the market inevitably dips, investors who have taken on more risk than they can emotionally handle tend to sell at the bottom, locking in losses and missing the subsequent recovery.

8. How does debt affect my risk tolerance?

High levels of high-interest debt (like credit cards) significantly lower your risk capacity. Before taking on high-risk investments, it is generally advised to pay down debt, as the “guaranteed return” of avoiding 20% interest is safer than any market investment.