How Rent Payments Help Manage Credit Utilization

Credit utilization is a big part of your credit score. It shows how much of your available credit you use. A high ratio hurts your score. A low one helps. But how do rent payments fit in? Rent isn’t credit. But it can be. In 2025, reporting rent to bureaus like Experian can build your credit. This lets you get higher credit limits. Higher limits mean lower utilization. We’ll explain it all. Why high utilization drops your score. How rent fixes it. With real examples. Easy to read. No fluff.Discover How Rent Payments Help Manage Credit Utilization! Learn why high utilization hurts scores, how AxcessRent reporting helps, and tips to manage credit with real examples.

What Is Credit Utilization?

Credit utilization is the percentage of your credit you use. Say you have a $1,000 limit on your card. You owe $300. That’s 30% utilization. Credit bureaus look at this. It’s 30% of your FICO score. VantageScore too. Keep it under 30%. Below 10% is best. High utilization makes lenders nervous. They think you’re maxed out. Might miss payments.

Why does it matter for renters? You need good credit to get apartments. Low utilization shows you’re responsible. It helps with loans or cards too.

Why Does Higher Credit Utilization Decrease Your Credit Score?

High utilization signals risk. Lenders see it as over-relying on credit. You might be in trouble. A 50% ratio looks bad. It drops your score fast. 30-50 points or more. Depends on your history.

Take John. He has a $5,000 limit. Owes $3,000. 60% utilization. His score was 720. It fell to 670. He applied for a car loan. Got a higher interest rate. Paid $2,000 extra over the loan.

Bureaus think high use means you can’t pay back. Low use shows control. Pay down balances. Or get higher limits. That’s where rent comes in.

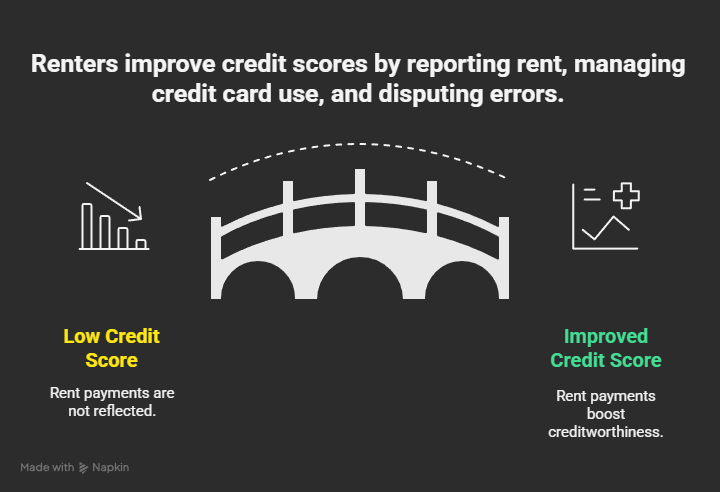

Rent builds history. Good history gets you higher limits. Higher limits lower utilization. Without more debt.

How Rent Payments Build Credit History

Rent is $1,000 a month or more. But it doesn’t count for credit. Unless reported. Services like AxcessRent do that. They send your payments to bureaus. Each on-time rent is like a loan payment. It adds to your payment history. 35% of your score.

Why does this help utilization? Better history means better score. Better score means lenders give higher limits. Say your card limit is $2,000. You owe $600. 30%. Get a limit increase to $4,000. Now 15%. Score up.

Real example: Sarah rents for $1,200. She uses AxcessRent. After 6 months, her score rises from 620 to 680. She asks for a credit limit increase. Gets $3,000 more. Her utilization drops from 40% to 25%. Score jumps 30 points.

Rent reporting is easy. Sign up. Verify with landlord. Pay rent as usual. Service reports it. Cost $5-10 a month. Worth it.

Step-by-Step: Start Rent Reporting

- Choose a service. AxcessRent reports to all three bureaus.

- Sign up online. Give lease details.

- Get landlord ok. They confirm payments.

- Link bank. Auto-report each month.

- Check score. See the boost.

Do this early in 2025. Build before applying for cards.

How Credit Utilization Affects Your Financial Health

Credit utilization isn’t just a number. It shapes your financial life. High utilization—say 60% on a $2,000 limit—can block you from loans or apartments. Lenders see risk. You might pay 5% more interest on a car loan. That’s $1,000 extra over five years. Low utilization, like 10%, shows control. You get better rates. Maybe save $500 on a credit card.

It ties to rent because good credit helps you negotiate leases. Landlords check scores. A 700 score versus 600 can mean $500 less deposit. Rent reporting boosts your score. That lowers utilization stress. Keep an eye on it. Use free tools like Credit Karma to track.

The Role of Rent Reporting in Credit Building

Rent reporting turns a big bill into a credit boost. Normally, $1,200 rent doesn’t hit your score. Services like AxcessRent change that. They report to Equifax, Experian, TransUnion. Each payment adds to your 35% payment history. Over six months, that can lift your score 20-50 points.

Why does this matter? Higher score means higher credit limits. Limits lower utilization. It’s indirect but powerful. Start with your landlord’s approval. Link your account. Pay on time. Check progress monthly. It’s $5-10 a month but pays off with better financial options.

Real-World Examples of Rent Helping Utilization

Meet Lisa. 28. Rents $1,400 in Seattle. Utilization 45% on $4,000 limit. She owes $1,800. Score 650. She starts AxcessRent. 4 months in, score 690. She gets limit to $6,000. Utilization 30%. Score 720. She gets a better car loan rate. Saves $1,500 in interest.

Another: Tom, 24. First job. $2,000 limit. Owes $800. 40%. No history. Uses rent reporting. 3 months, score up 40 points. Limit to $3,000. Utilization 27%. Gets approved for his first apartment alone.

These show rent lowers utilization indirectly. By building history for higher limits.

Why High Utilization Hurts: The Details

High utilization affects risk models. FICO sees it as a sign of trouble. You might default. It’s 30% of your score. A jump from 10% to 40% can drop 50 points.

It’s calculated per card and overall. Per card high? Hurts less than overall. But keep both low.

Rent helps by adding “trade lines.” More lines mean more available credit. Lower ratio.

Bureaus update monthly. Pay before statement closes. That lowers reported utilization.

Breaking Down Tips to Manage Utilization with Rent

Managing credit utilization with rent payments can feel tricky, but it’s doable with the right steps. These tips are practical and built for renters like you. Let’s go through each one, explain what it means, and how it works in real life. No jargon—just clear advice to keep your credit strong in 2025.

Pay Rent on Time. Use Auto-Pay.

Paying rent on time is key because it builds your payment history, which is 35% of your FICO score. When you report rent through a service like AxcessRent, late payments hurt more since they’re now on your credit report. Auto-pay ensures you never miss the due date. Set it up with your bank or landlord’s portal, and the payment goes out automatically.

How It Works

If your rent is $1,200 due the 1st, auto-pay deducts it from your account on time. No forgotten checks or excuses. On-time payments get reported, boosting your score over time. A late payment can drop your score by 50-100 points, so this avoids that risk.

Real-Life Example

Jake rents a place for $1,000. He sets auto-pay and uses AxcessRent. Six months in, his score jumps from 630 to 680. A friend who paid late saw a 70-point drop. Jake’s consistency paid off.

Report Every Payment. Don’t Miss.

Reporting every rent payment to credit bureaus (Equifax, Experian, TransUnion) turns your rent into a credit-building tool. Missing a report means missing a chance to show reliability. Services like AxcessRent automate this, but you need to keep it active and ensure each payment is logged.

How It Works

Sign up for AxcessRent, link your lease, and get landlord approval. Each $1,200 payment gets sent to bureaus monthly. If you skip a month or forget to report, that month’s good payment is lost. Consistency is what builds your history.

Real-Life Example

Maria rents for $1,500. She reports for 4 months, then skips one. Her score still rises 30 points, but she misses a 10-point boost. She restarts reporting and sees steady gains after.

Use the Score Boost to Ask for Limits.

As your credit score improves from rent reporting, use that to request higher credit limits from your card issuer. Higher limits lower your utilization ratio (debt divided by limit). A better score shows lenders you’re low-risk, making them more likely to approve.

How It Works

After 6 months of reporting, your score might hit 700 from 650. Call your bank or log in online. Ask for a limit increase from $2,000 to $4,000. If you owe $600, utilization drops from 30% to 15%. Score can rise another 20-30 points.

Real-Life Example

Tom’s score went from 620 to 690 with rent reporting. He asked for a $3,000 limit increase on his $1,500 card. Utilization fell from 40% to 20%. He got approved for a better apartment lease.

Keep Spending Low. Don’t Max New Limits.

Getting a higher limit is great, but maxing it out kills the benefit. High utilization (over 30%) still hurts your score, even with a bigger limit. The goal is to use credit sparingly to keep the ratio low and show discipline.

How It Works

With a new $4,000 limit, keep spending under $1,200 (30%). Better yet, stay under $400 (10%). Pay off balances monthly. Avoid big purchases right after a limit increase to let your score stabilize.

Real-Life Example

Sara got a limit boost to $5,000. She spent $2,500 on a trip, hitting 50% utilization. Her score dropped 40 points. She paid it down to $500 (10%) and saw a 25-point recovery.

Check Reports. Dispute Errors.

Credit reports can have mistakes—wrong late payments or old debts. Checking them catches these. Disputing errors removes bad marks, improving your score and utilization indirectly by keeping your credit profile clean.

How It Works

Get free reports at AnnualCreditReport.com (one per bureau yearly). Look for errors like a $200 bill you paid. File a dispute online with proof (receipts). Bureaus fix it in 30 days. A corrected error can add 10-20 points.

Real-Life Example

Mike found a $300 collection on his report that he’d settled. He disputed it with a bank statement. Score went from 640 to 660. His utilization looked better with the clean report.

Combine with Other Habits. Pay Cards Twice a Month. Keep Old Cards Open.

Pair rent reporting with smart habits. Paying cards twice a month lowers reported balances, reducing utilization. Keeping old cards open lengthens your credit history (15% of score), supporting the benefits of rent payments.

How It Works

Pay your $500 balance halfway through the month, then fully before the statement closes. This keeps utilization low (e.g., 10% vs. 50%). Don’t close a card you’ve had for years—even if unused—use it for a $10 charge monthly and pay it off.

Real-Life Example

Emily pays her $1,000 limit card $300 mid-month, then $200 more before closing. Utilization stays 20%. She keeps a 5-year-old card active with a $5 charge. Her score hits 720, up from 680, with rent reporting.

Conclusion

ent payments are a renter’s secret weapon for managing credit utilization, offering a practical way to strengthen your financial future in 2025. They build a solid payment history, which makes up 35% of your FICO score, and over time, this can unlock higher credit limits from lenders. With the average rent hitting $1,730, using a service like AxcessRent to report those payments—starting at just $5-10 a month—can be a game-changer. This boost can lower your utilization ratio from a risky 50% to a healthy 25%, potentially raising your score by 20-50 points and saving you hundreds on loans or deposits. It’s about consistency—pay on time with auto-pay, report every month, and watch your credit grow.

Check your credit reports regularly on AnnualCreditReport.com and dispute any errors to keep your profile clean. Pair this with habits like paying cards twice a month and keeping old accounts active to maximize your credit history’s impact. In today’s economy, where inflation pushes costs up 3-5%, avoiding high debt and building credit with rent is smarter than ever. Start today by signing up with AxcessRent, tracking your progress with Credit Karma, and taking control of your financial health. Better credit opens doors to better apartments, lower rates, and a stress-free life—make it happen now

FAQs on How Rent Payments Help Manage Credit Utilization

Why Does Higher Credit Utilization Decrease Your Credit Score?

It signals risk. Lenders think you’re overextended. A 50% ratio can drop your score 30-50 points. Keep under 30% for best scores.

How Do Rent Payments Help Manage Credit Utilization?

Rent builds history. Good history gets higher credit limits. Higher limits lower your ratio. Example: $1,000 debt on $2,000 limit = 50%. Increase to $4,000 = 25%.

Does Rent Reporting Affect Credit Utilization Directly?

No. It affects history (35% of score). But better score leads to higher limits, which lowers utilization (30% of score).

How Long Does Rent Reporting Take to Help Utilization?

3-6 months to build history. Then ask for limits. Utilization drops right after increase.

Can Rent Payments Hurt My Credit?

Only if late and reported. On-time payments help. Use AxcessRent to ensure reporting.

What’s a Good Utilization Ratio?

Under 30%. Below 10% is ideal. Calculate: debt divided by limit times 100.

How to Lower Utilization Fast?

Pay balances before statement closes. Ask for limit increases if score is good.