How Much Rent Can I Afford in 2026? Free Calculator & Tips

Before diving into apartment listings or rental websites, it’s important to ask yourself one key question: how much rent can I afford? A common starting point is the 30% rule, which recommends spending no more than 30% of your gross monthly income on rent. While this is a helpful guideline, it doesn’t fit everyone’s situation. Your actual rent affordability depends on several factors—your total income, monthly bills, debt obligations, lifestyle choices, and most importantly, the cost of living in your city.

At AxcessRent, we understand that finding affordable housing while managing other financial responsibilities can feel overwhelming. That’s why we’re here to help renters not only afford rent but also make their rent payments work for them—by helping build credit and gain access to long-term financial stability.

How Much Rent Can I Afford?

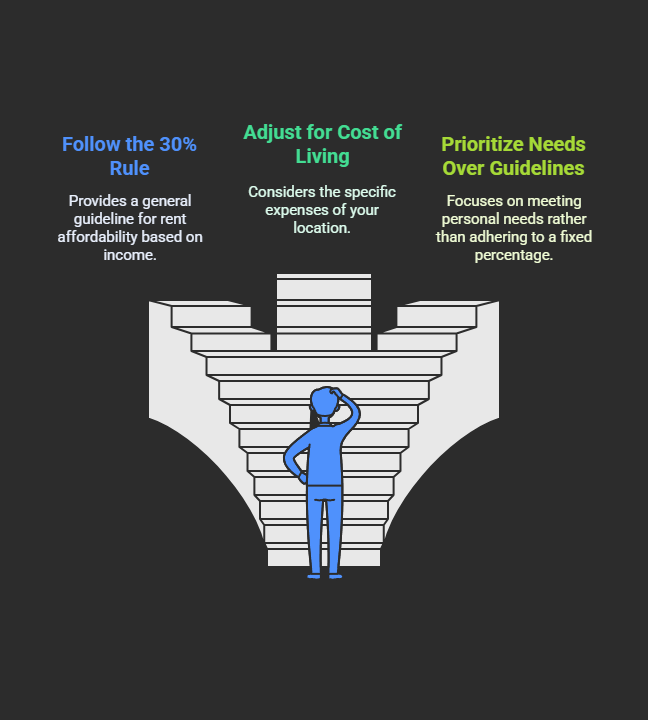

The 30% rule has been a widely accepted benchmark in personal finance for decades. It simply suggests that you should spend around 30% of your gross income (your income before taxes and deductions) on rent.

For example, if you earn $4,000 per month before taxes, 30% of that would be $1,200. In theory, this means $1,200 is a comfortable rent budget for you.

But this rule is more of a general starting point than a hard limit. In high-cost-of-living cities like New York or San Francisco, $1,200 won’t even get you a studio apartment, whereas in smaller towns, it might be more than enough for a nice one-bedroom. And if you find a place that only costs 18% of your income and it meets your needs don’t feel pressured to spend more just to meet a guideline.

How Much Should I Spend on Rent?

The 30% rule has been a widely accepted benchmark in personal finance for decades. It simply suggests that you should spend around 30% of your gross income (your income before taxes and deductions) on rent.

For example, if you earn $4,000 per month before taxes, 30% of that would be $1,200. In theory, this means $1,200 is a comfortable rent budget for you.

But this rule is more of a general starting point than a hard limit. In high-cost-of-living cities like New York or San Francisco, $1,200 won’t even get you a studio apartment, whereas in smaller towns, it might be more than enough for a nice one-bedroom. And if you find a place that only costs 18% of your income and it meets your needs—don’t feel pressured to spend more just to meet a guideline.

Remember, every financial situation is unique. Use the 30% rule as a guidepost, not a restriction.

US Rent Affordability Calculator

Enter your numbers:

Consider the 50/30/20 Budget Rule

Another helpful budgeting method is the 50/30/20 rule, which breaks your take-home (after-tax) income into three broad categories:

- 50% for Needs: This includes rent, groceries, utilities, insurance, transportation, and minimum debt payments.

- 30% for Wants: Think dining out, entertainment, hobbies, shopping.

- 20% for Savings and Debt Repayment: Contributions to savings, retirement, or paying down student loans, credit cards, etc.

Let’s say your monthly after-tax income is $4,000. Based on the 50/30/20 rule:

- You’d allocate $2,000 toward needs.

- Spend up to $1,200 on wants.

- And reserve $800 for savings or extra debt payments.

Here’s where rent comes in. If your rent and utilities alone are $1,600, that only leaves $400 for other essentials like groceries or insurance. So while the 50/30/20 method gives structure, you might need to tweak the percentages depending on your reality.

In some cases, the 60/30/10 rule—allocating a higher portion (60%) toward needs—might be more realistic, especially in expensive cities or during high inflation periods.

Example Rent Budget Breakdown

Let’s break this down with real numbers.

Say your after-tax monthly income is $4,000. Your fixed monthly costs include:

- Student Loan: $400

- Car Payment: $360

- Car Insurance: $135

- Groceries: $225

That’s a total of $1,120—leaving $880 for rent and utilities under the 50% “needs” category. But what if average rent in your area is $1,500? You’re already over budget.

This is a common issue for many renters, especially in urban areas. That’s why AxcessRent offers solutions like rent reporting to help you build credit history through your rent payments. So even if rent takes a bigger slice of your budget, you’re turning that expense into a credit-building opportunity.

US-specific table

| Gross Monthly Income | 30% Max Rent (US Average) | Notes |

|---|---|---|

| $3,000 | $900 | Good for Midwest/South |

| $4,000 | $1,200 | Fits many 1BR in average markets |

| $5,000 | $1,500 | Needed in bigger cities |

| $6,000+ | $1,800+ | Common in CA/NY areas |

When It Makes Sense to Spend More Than 30% on Rent

Life isn’t always neat and budget-friendly, and sometimes going over the 30% or 50% rule is not only okay—but necessary.

You may need to exceed your ideal rent budget if:

- You’re in an unsafe or unstable living situation, and your health or well-being is at stake.

- You’re relocating for a new job opportunity and need to be closer to work.

- You require special accommodations or amenities that justify the higher price, such as accessibility features, better security, or shorter commute times.

While it’s important to stay mindful of your spending, remember that comfort, stability, and safety are valid reasons to stretch your budget when necessary.

Factor in Hidden and Additional Costs

Rent isn’t the only cost you need to consider when budgeting for a new place. There are additional expenses—some obvious, others more hidden.

Transportation: Cheaper rent in a distant suburb may mean more money spent on gas, transit, or car maintenance.

Utilities: Some rentals include water, gas, or even electricity—others don’t. Always ask what’s included.

Amenities: Think about what comes with your rent. A place with an on-site gym, laundry, and free parking could save you $100–$300 monthly compared to a cheaper place without those features.

Commute time & lifestyle costs: Living closer to the city might mean you’ll walk or bike more—saving money on transportation and even improving your health.

Tips to Cut Costs and Afford Rent

If your ideal rent is a stretch, here are a few ways to lower your monthly burden:

1. Get a Roommate

Splitting a two-bedroom with someone could cut your rent and utilities in half. You get the same location, same amenities, at a much lower personal cost.

2. Negotiate Your Bills

Call your internet or phone provider and ask about promotional rates or cheaper packages. Every $10 or $20 you save adds up.

3. Use Coupons and Meal Plans

Groceries are a necessity—but you can still be smart about spending. Use store apps, loyalty programs, and meal plans to reduce waste and maximize value.

4. Shop Around for Car Insurance

Getting quotes from different insurance providers could reveal significant savings. You can also ask about safe driver or low-mileage discounts.

5. Look for Rental Deals

Many landlords offer first-month-free or no-deposit specials, especially during slow rental seasons. Also, offering to sign a longer lease can sometimes earn you a lower monthly rate.

6. Use AxcessRent to Build Credit

When you’re already spending hundreds or thousands on rent, why not make those payments work for you? With AxcessRent’s rent reporting services, you can build your credit score month by month—without needing a credit card or loan.

Final Thoughts

Rent is likely your biggest monthly expense, but it doesn’t have to be a financial trap. By knowing your income, understanding your real monthly needs, and using smart strategies like rent reporting, budgeting tools, and cost-cutting techniques—you can take control of your rental finances.

At AxcessRent, we’re not just here to help you find a place to live—we’re here to help you build the future you deserve through financial empowerment.

FAQs

How do I calculate how much rent can I afford?

You can start with the 30% rule—spend no more than 30% of your gross income on rent. Or use a rent affordability calculator to consider other expenses like debts, savings goals, and cost of living.

What’s the average rent in the US right now?

The average rent in US right now is around $1,800–$2,000/month in early 2026, but varies a lot by state and city.

Is the 30% rule for rent still relevant today?

Yes, it’s a helpful starting point, but it may not work for everyone. In high-cost cities, spending more may be necessary, while in low-cost areas, you might spend less and save more.

What is a rent affordability calculator?

A rent affordability calculator is a tool that helps estimate the rent you can afford based on your income, expenses, and financial goals.

Should I base rent on gross or net income?

While the 30% rule is based on gross income, many experts recommend budgeting using net (after-tax) income for a more realistic financial picture.

How can I lower my rent expenses?

You can lower rent costs by living with a roommate, moving to a less expensive area, negotiating with landlords, or finding properties with included utilities or move-in deals.

Can spending too much on rent hurt my finances?

Yes. Overspending on rent can limit your ability to save, pay off debt, or handle emergencies, leading to financial stress or instability.

Does rent affect my credit score?

Yes, if your rent payments are reported to credit bureaus. Services like AxcessRent help renters build credit by reporting on-time rent payments.

What percentage of income should go to rent and bills combined?

Using the 50/30/20 rule, about 50% of your take-home pay should cover needs—including rent, utilities, groceries, and essential bills.

Is it okay to spend more than 30% of my income on rent?

In some cases, yes—especially if you’re in a high-cost area or have fewer debts. Just make sure the rest of your budget can support it.

What should I consider besides rent price when renting?

Think about total living costs: utilities, transportation, parking, laundry, insurance, and proximity to work or essential services. These can impact your true affordability.