How Is Credit Score Calculated for Married Couples?

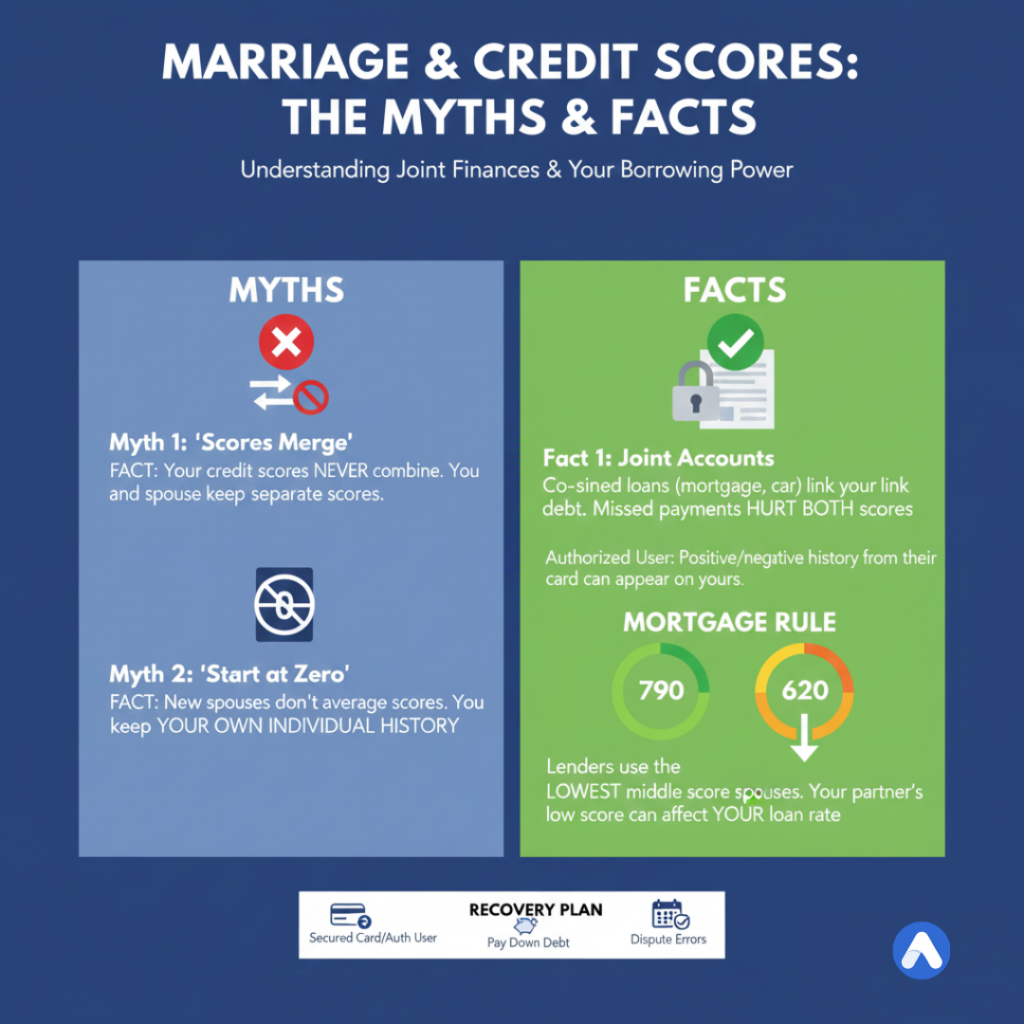

The short answer: It isn’t. There is no such thing as a “joint credit score.” When you get married, your credit scores do not merge, average out, or combine. You keep your own score, and your spouse keeps theirs.

However, marriage does affect your borrowing power in specific ways. While your scores remain separate, your debt can become linked if you open joint accounts, and this impacts your ability to buy a house together.

The “Merger” Myth: Why Your Files Stay Separate

Credit reporting agencies (Equifax, Experian, TransUnion) track credit histories based on Social Security Numbers, not marriage licenses. Even if you change your last name, your credit history is tied to your individual identity.

Think of your credit report like a school transcript. Just because you get married doesn’t mean your grades from high school get averaged with your spouse’s grades. You both still have your own permanent record.

When Does Marriage Actually Affect Your Score?

Your spouse’s bad habits cannot hurt your score unless you attach your name to their accounts. This happens in two ways:

1. Joint Accounts (Co-Signing)

If you open a mortgage, car loan, or joint credit card together, you are both 100% responsible for the debt.

- The Risk: If your spouse misses a payment on a joint car loan, that late payment shows up on your credit report too, dropping your score.

- The Benefit: If you pay on time, you both get the positive history.

2. Authorized User Status

If your spouse has a credit card with a 10-year perfect history and adds you as an “Authorized User,” their good history gets copied to your file. This is a common hack to boost a partner’s score. However, if they max out that card, your score will drop because of the high utilization.

The Mortgage Rule: How Lenders View Couples

This is the most critical concept to understand. While you don’t have a joint score, lenders use a specific formula to judge couples applying for a mortgage.

They do not average your scores. They use the lowest middle score.

The “2-2-2” Calculation Logic

When two people apply for a loan, the lender pulls three scores (Equifax, Experian, TransUnion) for both people.

- They find Person A’s middle score.

- They find Person B’s middle score.

- They use the lower of the two.

Example: The “Bad Score” Anchor

- You (Person A): Scores are 780, 790, 800. (Middle: 790)

- Spouse (Person B): Scores are 600, 620, 630. (Middle: 620)

The Result: The lender bases the interest rate on the 620 score. Your 790 is effectively ignored. This is why one spouse’s poor credit can disqualify a couple from buying a home, even if the other spouse is wealthy.

Table: What Links You vs. What Doesn’t

| Action | Does it Link Your Credit? | Impact on Score |

|---|---|---|

| Getting Married | NO | Zero impact. |

| Changing Your Name | NO | Zero impact (updates info only). |

| Applying for a Joint Mortgage | YES | Hard inquiry on both reports. |

| Spouse has Student Loans | NO | Only affects their debt-to-income ratio. |

| Adding Spouse as Authorized User | YES | Their card history appears on your file. |

| Spouse files Bankruptcy | NO* | Usually rarely affects you unless debts were joint. |

*Note: In community property states (like California or Texas), debts incurred during marriage may be considered joint liabilities even if only one name is on the account.

How to Fix a “Mixed” Credit Situation

If one spouse has bad credit, you have three options before applying for a major loan:

- The Piggyback Method: The spouse with good credit adds the other as an authorized user on their oldest, cleanest credit card. This can boost the lower score by 20–40 points quickly.

- Apply Solo: If one spouse has terrible credit, apply for the mortgage in the higher-scoring spouse’s name only. Caveat: You can only use that person’s income to qualify, which might lower your buying power.

- Debt Diet: Pay down credit card balances on the lower-scoring spouse’s accounts 30 days before applying. Utilization is the fastest way to manipulate a score.

Frequently Asked Questions (FAQ)

Does my credit score drop when I get married?

No. Marriage is not a factor in credit scoring models. Your score will only change if you apply for new credit or open joint accounts.

Can I hide my bad credit from my spouse?

Technically, yes, until you apply for a loan together. The lender will pull both reports, and your spouse will see your score and debts on the disclosure forms.

If I divorce, does the joint debt disappear?

No. A divorce decree is a court order between you and your ex, but it does not break the contract with the bank. If the judge orders your ex to pay the joint Visa card and they stop paying, the bank can and will come after you (and ruin your credit score). You must refinance or close joint accounts to separate them.

What happens if I change my last name?

You should notify the credit bureaus and your creditors. Your history will not disappear; it will simply be tagged with your new alias. For a few months, you might see “split file” issues, but the score remains the same.