How can i fix my bad credit?: Step-by-Step Guide

You miss a few payments, lose track of bills, or hit a rough patch, and suddenly, every lender sees you as a risk. You get denied for credit cards. Auto loans come with sky-high interest. Even apartment applications get tricky. If you’ve ever caught yourself typing “Fix My Bad Credit” into Google at 2 AM — you’re not alone. Millions of Americans are in the same boat, trying to figure out how to clean up their credit and start fresh.

Here’s the truth: fixing bad credit isn’t magic, but it’s absolutely doable. You don’t need to be rich, and you don’t need a lawyer. What you do need is a plan — and consistency.

This guide breaks down how to fix bad credit step by step — from understanding what’s hurting your score to building it back stronger than before.

What is a bad credit score?

When someone says “I have bad credit,” what they’re really talking about is their credit score — a number that lenders use to measure how risky it is to lend to you.

Most people use the FICO or VantageScore models, which range from 300 to 850.

Here’s how those scores typically break down:

| Credit Range | Rating | What It Means |

|---|

| 800–850 | Excellent | You’re a top-tier borrower. |

| 740–799 | Very Good | You qualify for most loans easily. |

| 670–739 | Good | Average credit, still solid. |

| 580–669 | Fair | You’ll face higher rates. |

| 300–579 | Poor | Major credit issues — approvals are tough. |

If you fall in the “fair” or “poor” range, lenders see you as risky. That doesn’t mean you’re doomed — it just means you’ve got work to do to rebuild trust.

Common reasons for bad credit include:

- Late or missed payments

- Charge-offs or collections

- High credit card balances

- Too many credit inquiries

- Old unpaid debts

- Bankruptcy or foreclosure

But here’s the silver lining: credit isn’t permanent. It’s a snapshot of your past behavior — not your future potential.

I followed these steps to Fix My Bad Credit

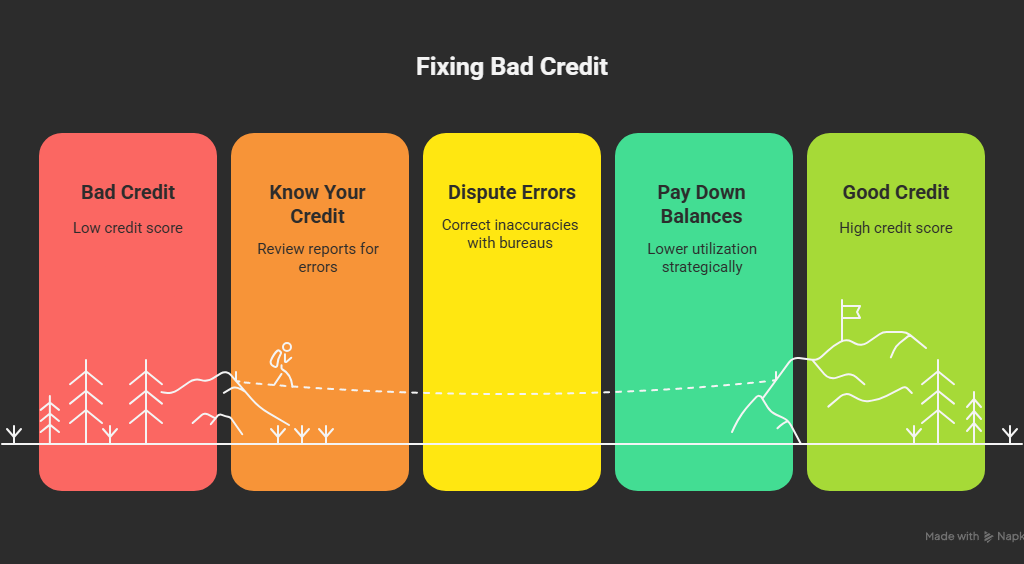

Step 1: Know Where You Stand

You can’t fix what you don’t understand. So first, find out exactly what’s pulling your score down.

Under federal law, you’re entitled to a free copy of your credit report every year from each bureau — Experian, Equifax, and TransUnion — at AnnualCreditReport.com.

When you review your reports, look for:

- Late payments — Check if the dates are accurate.

- Collections — Are the balances correct?

- Charge-offs — Still unpaid? Verify details.

- Accounts you don’t recognize — Possible identity theft.

- Old debts — Should they have already fallen off after 7 years?

Make notes on every questionable item. You’ll use this list for your next move.

Step 2: Dispute Errors on Your Credit Report

Errors happen more than you’d think. A 2023 FTC study found that 1 in 5 credit reports contains at least one mistake that could affect a score. If you see something wrong — don’t ignore it. Dispute it directly with the credit bureau. Each bureau lets you file disputes online or by mail. You’ll need:

- A copy of your credit report (highlight the error)

- Any supporting documents (payment receipts, bank statements, letters)

- A short explanation of why it’s wrong

By law, under the Fair Credit Reporting Act (FCRA), bureaus must investigate and respond within 30 days. If the creditor can’t verify the item — it gets removed. That alone can boost your score within a month or two.

Step 3: Pay Down Balances Strategically

One of the fastest ways to improve credit is lowering your credit utilization — how much of your available credit you’re using. For example, if you have a $1,000 limit and owe $900, your utilization is 90%. That’s bad. You want to keep it under 30%, ideally under 10%.

Start with the avalanche method:

- Pay off high-interest cards first.

- Make minimum payments on others.

- Once one card is paid off, roll that payment to the next.

Or use the snowball method for motivation:

- Pay off the smallest balance first.

- Celebrate small wins.

- Build momentum.

Either way, the goal is the same — reduce balances and prove control over your credit.

Step 4: Bring Delinquent Accounts Current

If you’re behind on payments, get current. Even one missed payment can drop your score 50–100 points.

Here’s how to handle it smartly:

- Call your creditor — Explain your situation. Ask about hardship programs.

- Request a “goodwill adjustment.” Sometimes lenders remove late marks if you’ve been consistent otherwise.

- Set up autopay to prevent future misses.

You can’t erase the past, but consistency now makes a huge difference. After 6–12 months of on-time payments, your score can start to rebound significantly.

Step 5: Don’t Close Old Accounts

It’s tempting to close old credit cards once you pay them off, but that can backfire.

Why? Because closing an account reduces your total available credit — which increases utilization. It also shortens your credit history.

Instead, keep old cards open with small recurring charges (like Netflix or Spotify). Pay them off monthly. This shows steady activity and keeps your credit age healthy.

Step 6: Add Positive Payment History

You don’t need new loans to prove financial responsibility — you just need consistent on-time payments reported to credit bureaus.

That’s where rent reporting comes in.

At AxcessRent, we help renters build credit by reporting their on-time rent payments to major credit bureaus.

Here’s why it works:

- Rent isn’t traditionally reported to credit bureaus — unless you do it through a service like ours.

- Those on-time payments count toward your credit history, just like a loan or credit card.

- Over 6–12 months, renters often see their scores improve by 20–60 points.

It’s one of the easiest, most affordable ways to fix bad credit without taking on new debt.

Step 7: Rebuild with Secured Credit

If your score is too low to get approved for regular credit cards, try a secured card.

You deposit a small amount (say $300), and that becomes your credit limit. Use it for small purchases and pay it off in full every month.

Within 6–9 months, you’ll start seeing positive results. Once your score improves, you can graduate to an unsecured card — and get your deposit back.

Step 8: Avoid New Hard Inquiries

Every time you apply for a loan or credit card, lenders run a “hard inquiry.” Too many of those in a short period can drag your score down.

Limit new applications while rebuilding. Focus instead on:

- Paying down existing debts

- Maintaining low utilization

- Letting accounts age

Remember: rebuilding credit is about time and trust. Each month you make progress, lenders notice.

Step 9: Mix Up Your Credit Types

Credit scoring models reward diversity.

Having a mix of installment loans (like car loans or credit-builder loans) and revolving accounts (like credit cards) shows you can handle different types of credit responsibly.

You don’t need to open everything at once. Just balance it over time.

Step 10: Track Your Progress

Fixing bad credit isn’t a one-time task — it’s a journey.

Check your credit report every few months. Use free tools like Credit Karma, Experian, or your bank’s credit monitoring service. Celebrate the small wins:

- Late payments removed.

- Collections deleted.

- Utilization down.

- Score up 20 points.

Progress is progress. Every good decision adds up.

What to Avoid While Fixing Bad Credit

There are plenty of traps that can set you back. Watch out for these:

- “Credit repair” scams — No company can legally remove accurate negative information.

- Closing multiple accounts — Hurts your utilization and history.

- Paying for fake tradelines — Can lead to fraud flags.

- Ignoring old collections — Some may turn into lawsuits.

If it sounds too good to be true, it probably is.

How Long Does It Take to Fix Bad Credit?

There’s no overnight fix. But steady progress is real. Here’s a rough timeline based on effort:

| Time Frame | Expected Results |

|---|---|

| 1–3 months | Small score bumps from disputes or paying down balances |

| 3–6 months | Noticeable improvement if you pay on time and reduce debt |

| 6–12 months | Potential jump of 50–100 points with consistent good habits |

| 12–24 months | Major rebuild — lenders start approving again |

Think of it like rebuilding trust. Each month you prove reliability, your score reflects it.

Real Story: From 520 to 700 in a Year

Take James, a renter who joined AxcessRent in 2023. He had a 520 score after losing his job and falling behind on two credit cards.

Here’s what he did:

- Checked reports for errors and disputed them.

- Paid down one card using the snowball method.

- Signed up for rent reporting.

- Opened a secured card and paid it off monthly.

By mid-2024, his score hit 700. No shortcuts. Just consistent action.

That’s the power of patience and a plan.

How Rent Reporting Helps Fix Bad Credit

Rent reporting is one of the most underused tools for credit repair — especially for renters.

Here’s why it works:

- Payment history is 35% of your FICO score.

- Rent is often your biggest recurring payment.

- When reported, it builds positive history automatically.

With AxcessRent, you can:

- Add past rent history (up to 24 months)

- Report ongoing payments monthly

- Build credit without taking on loans or credit cards

It’s a simple, affordable path to rebuilding.

Conclusion

Bad credit doesn’t define who you are—it’s simply a reflection of past habits. With steady effort, clear priorities, and consistent on-time payments, you can rebuild your score and restore financial confidence. Small, disciplined actions every month lead to long-term, lasting improvement.

Repairing credit takes patience, not perfection. Focus on progress, not quick fixes. Use tools like rent reporting, secured cards, and regular monitoring to strengthen your financial profile. Over time, your persistence pays off—and your credit report will start reflecting the responsible borrower you’ve become.

Frequently Asked Questions (FAQs)

1. How to repair bad credit on my own?

Yes. Everything credit repair companies do, you can do yourself for free — with time, patience, and the right steps.

2. How fast can I raise my score?

Many people see improvements within 3–6 months by lowering balances, disputing errors, and paying on time.

3. Does paying off collections help?

Yes — especially newer ones. It won’t remove them instantly, but it improves your risk profile and stops new damage.

4. Will rent reporting really help?

Absolutely. Consistent rent payments build a strong payment history — the #1 factor in credit scoring.

5. Is bankruptcy the only option for bad credit?

Not usually. Bankruptcy is a last resort. Most credit issues can be solved with time, negotiation, and smart rebuilding.