Financial Tips for Renters in Shared Houses

Living with roommates can be a lifesaver. Rent is crazy high these days—average one-bedroom is $1,730, says Apartment List. Splitting a house makes it affordable. But shared houses come with money headaches. Who pays for what? What if someone skips out? This guide gives financial tips for renters in shared houses. It covers budgeting, bills, and avoiding fights. If you’re searching “financial tips for renters in shared houses,” “what is shared ownership houses,” or “how do shared ownership houses work,” you’re in the right place. We’ll explain shared ownership, who owns it, and how it works for renters. Plus, tips to keep your wallet happy.

I know shared living. I did it for five years. It saved me thousands but caused stress too. One roommate always “forgot” his share of the electric bill. Another left without notice. These stories are real. This guide fixes that. It’s straightforward. No fancy words. Just advice that works. We’ll hit FAQs like “who owns shared ownership houses” and “shared houses rent costs.” Let’s start with the basics.

What Are Shared Houses?

Shared houses are homes where two or more people rent rooms or space. It’s not just college kids anymore. In 2025, 32% of adults 25-34 live with roommates, per Pew Research. Why? Rent is up 4.2% from last year. A two-bedroom in Chicago costs $2,100. Split with one person, it’s $1,050 each. Affordable.

Shared houses can be:

- Room Rentals: You rent a bedroom in a house. Common areas like kitchen and living room are shared.

- Full House Shares: Everyone splits the whole house rent and bills equally.

- Sublets: Someone moves out, you take their spot short-term.

Pros: Lower costs, social life, shared chores. Cons: Less privacy, bill fights, bad roommates.

For first-time renters, shared houses are a start. You learn budgeting without full rent burden.

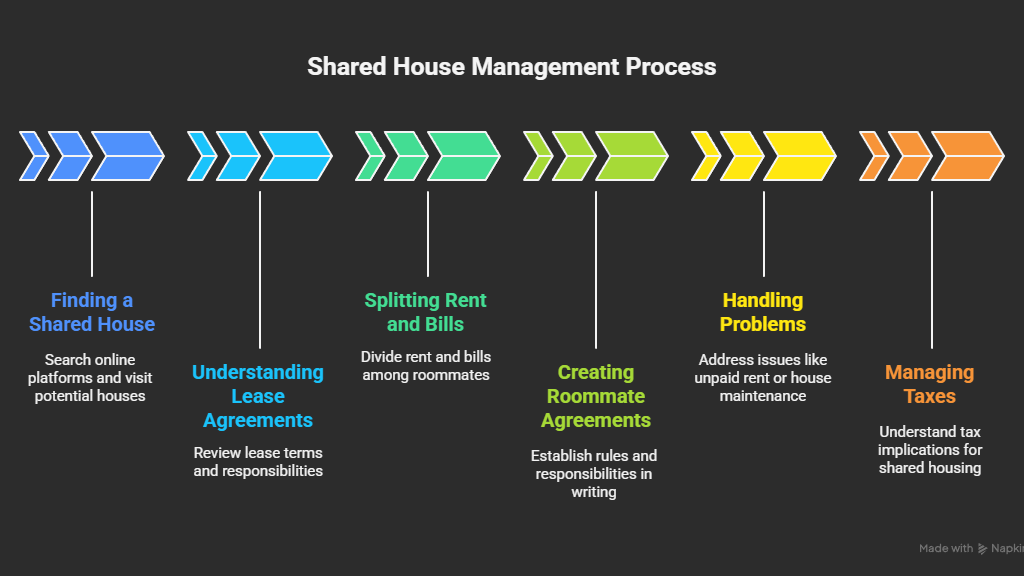

How Do Shared Houses Work?

Shared houses sound simple. But details matter. Here’s how they run day to day.

Finding a Shared House

Look on Craigslist, Facebook Marketplace, or Roommates.com. Post “ISO room in shared house” or search “rooms for rent.” Visit in person. Check cleanliness, noise, and roommate vibes. Ask about bills—who pays what?

Leases vary. Some landlords sign one lease for all. Others do individual room leases. Know yours. If one person leaves, you’re still on the hook.

Splitting Rent and Bills

Rent is easy—divide by rooms or equally. A four-bedroom house at $2,400 is $600 each.

Bills are trickier:

- Utilities: Electric, gas, water—split by use or equal. Use apps like Splitwise to track.

- Internet/Cable: $80/month, split four ways = $20 each.

- Groceries: Buy your own or share. Shared potlucks save money.

- Maintenance: Landlord covers big stuff. Small fixes? Split costs.

Set rules upfront. “We split utilities 50/50 based on bedrooms.” Write it in a roommate agreement. Not legal, but it helps.

Roommate Agreements

This is your bible. Include:

- Rent amount and due date.

- Bill splits and payment day.

- Guest rules—no overnight more than twice a month.

- Quiet hours—10 PM to 7 AM.

- Notice for leaving—30 days.

Sign it. It prevents fights. If someone skips rent, you have proof.

Handling Problems

Roommate drama happens. One doesn’t pay? Cover it, then chase them. Use small claims court if needed—$50 filing fee.

Bad house? Document issues. Talk to landlord. If unsafe, local codes protect you.

Taxes: Rent isn’t deductible. But home office deductions apply if you work from home.

Shared houses work if you communicate. Set expectations early.

Financial Tips for Renters in Shared Houses

Money is the main stress in shared houses. Here’s how to handle it right. These tips save you cash and headaches.

1. Create a Shared Budget

Sit down weekly. Use Google Sheets or Splitwise. List rent, bills, groceries. Assign shares.

Example: House rent $2,400. Four people = $600 each. Electric $200 = $50 each. Track who pays.

Tip: One person collects all, then reimburses via Venmo. Avoids late fees.

2. Automate Bill Payments

Set auto-pay for rent and utilities. No one forgets. Apps like Mint link accounts and alert you.

For shared bills, use BillSplit or Kitty. Everyone chips in via app.

3. Track Expenses with Apps

Splitwise is free. Log “I bought toilet paper $10.” It calculates owes. Pay up end of month.

YNAB (You Need A Budget) is $14.99/month. Teaches allocating money. Good for first-timers.

4. Negotiate Bulk Deals

Shared houses mean group power. Buy internet as a group—$80 for four vs. $50 each alone.

Groceries: Costco membership $60/year. Split cost. Buy in bulk, save 20%.

5. Build Credit with Rent Reporting

Paying rent builds credit if reported. AxcessRent does it for $5/month. Your $600 share shows as positive payment.

Why? Landlords see you as reliable. Future rentals easier.

6. Emergency Fund for Shared Risks

One roommate leaves? You cover their share short-term. Save $500-1,000 for that.

High-yield savings at Ally (4% APY) grows it.

7. Tax Tips for Shared Renters

Rent isn’t deductible. But:

- Home office: Deduct 5 sq ft of space at $5/sq ft = $300/year.

- Repairs: If you fix something, deduct as business expense if work-related.

Use TurboTax for renters. It finds deductions.

8. Avoid Shared Debt Traps

Don’t co-sign loans for roommates. If they default, your credit suffers.

For shared expenses, use apps, not personal checks.

9. Insurance for Shared Houses

Renters insurance covers your stuff—$15/month for $30,000. Add liability for parties.

Shared policy? No. Each gets own. Bundle with auto for 10% off.

10. Side Hustles to Cover Shares

Gig work fills gaps. Drive Uber ($20/hour) or TaskRabbit ($25/hour). $200 extra covers a bill.

what are shared ownership houses ?

Shared ownership is different from renting rooms. It’s buying part of a house, renting the rest. Common in UK, growing in US.

You buy 25-75% of the home. Pay mortgage on your share, rent on the rest. Housing associations own the unsold part.

Example: $300,000 house. You buy 40% ($120,000). Mortgage $800/month. Rent the 60% for $600. Total $1,400/month vs. $2,000 full rent.

Pros: Build equity. Lower upfront cost.

Cons: Staircasing (buying more shares) is hard. Resale rules.

For US renters, it’s like lease-to-own. Check FHA programs.

Shared ownership houses how does it work ?

It starts with eligibility. Income under $80,000, first-time buyer.

- Find a Property: Through housing associations or sites like Share to Buy.

- Deposit: 5-10% of your share ($6,000 on $120,000).

- Mortgage: For your share only.

- Rent: Service charge + ground rent for unsold part.

- Staircasing: Buy more over time, up to 100%.

Costs: Mortgage + rent + fees. In 2025, with rates 6%, it’s $1,200 total for a $300,000 share.

Legal: Association approves buyers. You can’t sublet without permission.

It’s good for low-income. But calculate total costs. Rent portion rises with inflation.

Who Owns Shared Ownership Houses?

You own your share. The housing association or developer owns the rest. They manage maintenance and set rent.

As owner, you decide decor in your space. But common areas are shared rules.

When selling, association has first buy-back. Or you sell on market with their approval.

For renters thinking of it, it’s a step to owning. But not full control.

Shared Houses Rent Costs

Rent in shared houses varies. Average room $800/month in US cities. Full house share $1,200/person for four-bedroom.

Breakdown:

- Rent: $600-1,200/room.

- Utilities: $50-100/person.

- Internet: $20/person.

- Groceries: $300/person (shared saves 20%).

Total: $1,000-1,600/month. Vs. solo $1,730.

In shared ownership, “rent” is on unsold share—$600 for 60% of $300,000 house.

Costs rise 3-5% with inflation. Budget extra.

Conclusion

Living in a shared house in 2025 is one of the smartest ways to beat sky-high rent prices, but it demands sharp financial habits to keep things smooth. Splitting rent and bills can save you thousands—$1,050 a month versus $1,730 for a solo apartment—but only if you plan carefully. Set up a clear roommate agreement to avoid disputes over who owes what. Use apps like Splitwise or YNAB to track every dollar, from $50 utility shares to $10 grocery splits. Automate payments to never miss rent, and report those payments with AxcessRent to build your credit score, which can save you on future deposits or loans.

Consider shared ownership if you’re eyeing a path to owning a home; it’s a stepping stone, but weigh the costs of mortgage plus rent. Inflation is pushing costs up 3-5%, so build a $1,000 emergency fund to cover surprises like a roommate bailing. Get renters insurance for $15 a month to protect your stuff, and explore side hustles like Uber to pad your budget. Whether you’re a first-time renter or a seasoned one, these steps keep your finances tight and your house drama-free. Start today: draft a budget with your roommates, check out AxcessRent for credit-building, and visit ApartmentList.com to compare shared house costs. Rent smart, save big, and make shared living work for you in 2025.

FAQs on Shared Houses and Finances

What Is Shared Ownership Houses?

Shared ownership is buying part of a house (25-75%), renting the rest from a housing association. It’s for first-time buyers with low deposits.

How Do Shared Ownership Houses Work?

Buy a share, pay mortgage on it, rent the rest. Staircase to buy more. Association owns unsold part.

Who Owns Shared Ownership Houses?

You own your share. Housing association owns the rest until you buy it all.

What Are Shared Houses Rent Costs?

$600-1,200/room + $50-100 utilities/person. Total $1,000-1,600/month per person.

How to Budget in Shared Houses?

Use Splitwise for bills. Auto-pay rent. Save 10% for emergencies.

Can Shared Houses Build Credit?

Yes. Report your rent share with AxcessRent. It boosts payment history.