Everything You Need to Know About Roth IRA

If you’re reading this, you’ve probably heard that a Roth IRA is a “good idea.” That is a massive understatement. In the world of finance, where every bank and government agency is trying to take a slice of your pie, the Roth IRA is one of the few places where you get to keep the whole thing.

Let’s cut through the jargon. You don’t need a PhD in finance to understand this; you just need to understand how to keep the government’s hands out of your pockets.

What is Roth IRAs ?

Most people mistake a Roth IRA for an investment. It’s not. If you tell someone, “I bought some Roth IRA today,” you’re going to get some funny looks.

A Roth IRA is a tax-advantaged bucket. You put money in the bucket, and then you use that money to buy things like stocks, bonds, or real estate. The “magic” isn’t in what’s in the bucket—the magic is the bucket itself.

The Core Philosophy: With a traditional retirement account (like a 401k or a Traditional IRA), you get a tax break now, but you pay the piper later. With a Roth, you pay the tax now (using your take-home pay), but everything that happens inside that bucket—and everything you take out of it later—is completely, 100% tax-free.

If you’re new to investing, this guide on building a long-term investment strategy breaks down what actually belongs inside that bucket.

Why Roth IRA Matters ?

Let’s say you’re 25 years old. You put $7,000 into a Roth IRA this year. You invest it in a boring S&P 500 index fund that returns an average of 10% a year. By age 65, that single contribution becomes over $316,000 — thanks to compound interest over time.

If that money was in a regular brokerage account, you might owe the government $45,000 to $60,000 in capital gains taxes when you try to spend it. In a Roth IRA? You keep every single penny. That is the difference between retiring in a tiny apartment and retiring on a boat.

Rules of Engagement (Limits and Eligibility)

The government knows this is a “cheat code,” so they put fences around it. You can’t just dump a million dollars in here.

How much can you contribute to a Roth IRA ?

The IRS updates these numbers every couple of years to keep up with inflation. If you’re young, you have a lower limit than the “catch-up” crowd.

| Year | Under Age 50 | Age 50+ (Catch-up) |

|---|---|---|

| 2024 | $7,000 | $8,000 |

| 2025 | $7,000 | $8,000 |

The “Earned Income” Trap

You cannot contribute more than you earned. if you only made $3,000 working a summer job, you can only put $3,000 in your Roth. You can’t use your birthday money from Grandma unless you can prove it was “income” (though technically, if you did chores for her and she “hired” you, you’re in the clear).

If you’re budgeting to free up money for investing, zero-based budgeting is one of the easiest ways to find extra cash without cutting your lifestyle.

Income Phase-Outs

If you make “too much” money, the IRS starts to get jealous. They start reducing how much you can contribute. For 2024, if you’re single and make over $146,000, the amount you can put in starts to drop. If you make over $161,000, you’re technically “banned” from the front door. (But don’t worry, we’ll talk about the “backdoor” in a minute).

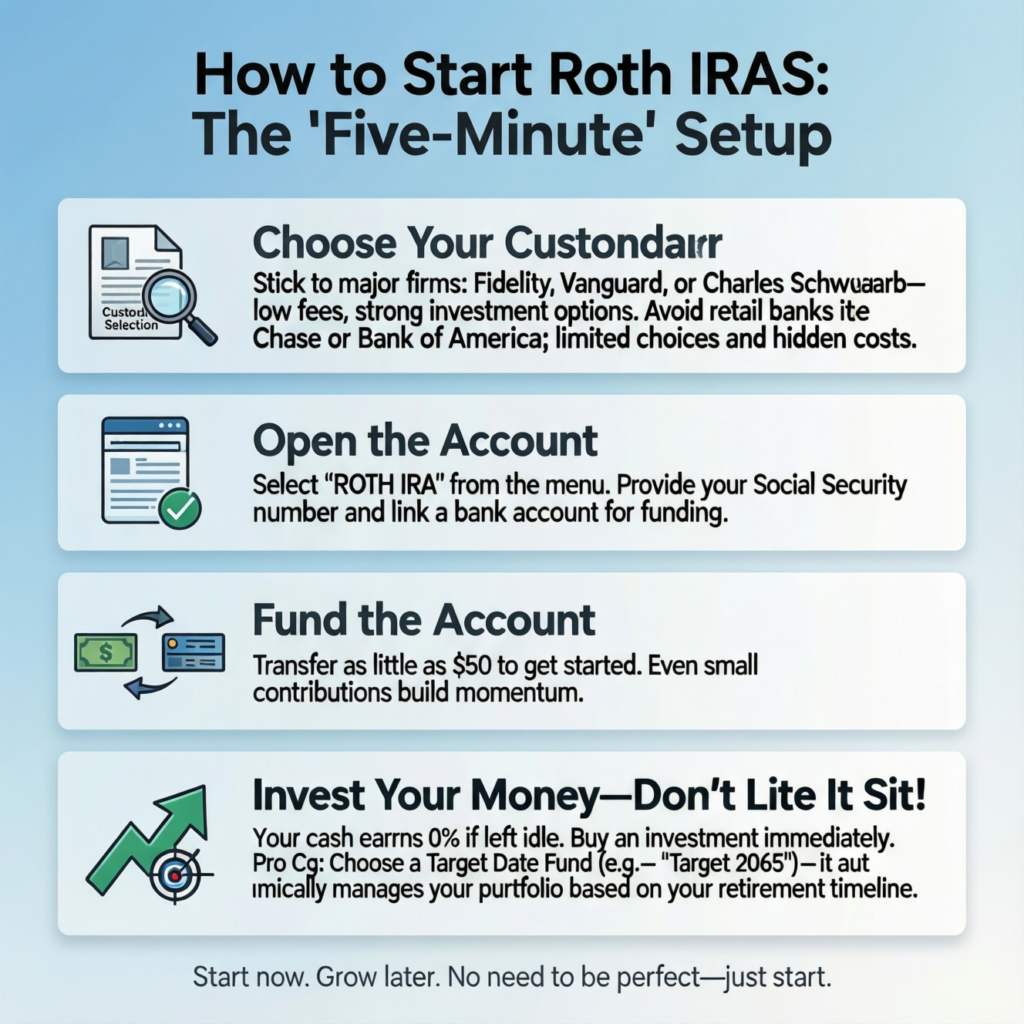

How to Start (The “Five-Minute” Setup)

Don’t let the fear of “doing it wrong” stop you. Opening an account is easier than ordering a pizza.

- Pick a Custodian: This is just a fancy word for a bank or broker. My advice? Stick to the big three: Fidelity, Vanguard, or Charles Schwab. They have the lowest fees. Avoid “retail” banks like Chase or Bank of America for this—their investment options usually suck and come with hidden fees.

- Open the Account: Select “Roth IRA” from their menu. You’ll need your Social Security number and a bank account to link it to.

- Fund the Account: Move your money over. Even if it’s just $50 to start.

- THE MOST IMPORTANT STEP: Many people move the money and then stop. If you do this, your money will sit there as “cash” and grow at 0%. You must actually buy an investment.

- Pro Tip: If you’re overwhelmed, just buy a “Target Date Fund” for the year you plan to retire (e.g., Target 2065). It does all the work for you.

If you’re unsure what to buy, learn the basics of asset allocation or use a Target Date Fund (e.g., Target 2065).

The “Backdoor” Roth IRA (For the High Earners)

So, you’re a high-flyer and you make $200,000 a year. The IRS says you can’t have a Roth IRA. They’re wrong. There is a perfectly legal loophole called the Backdoor Roth.

Here is how you do the dance:

- Step A: Open a Traditional IRA (which has no income limits for contributions).

- Step B: Put your $7,000 in there. Do not claim a tax deduction for it.

- Step C: Wait a day or two for the funds to settle.

- Step D: Click the “Convert to Roth” button on your broker’s website.

- Step E: Pay $0 in taxes (because you didn’t take a deduction in Step B) and now your money is in the Roth “bucket” where it belongs.

It’s a bit of extra paperwork, but it’s the only way for high earners to get that tax-free growth.

When can i withdraw from Roth IRA ?

People hate “locking up” their money. The good news? The Roth IRA is actually the most flexible retirement account in existence.

- Your Contributions: You can take out the money you put in at any time. If you put in $10,000 over two years and you have an emergency, you can take that $10,000 back out tomorrow. No taxes, no penalties.

- The Earnings (The Profits): This is the part you should leave alone. If you take out the growth before age 59.5, you’ll usually pay a 10% penalty plus income taxes.

- The Exceptions: There are ways to get the profit out early if you really need it:

- First Home: You can take out up to $10,000 of profit to buy your first house.

- Education: You can use it for college expenses for you, your spouse, or your kids.

- Medical: If you have massive medical bills or lose your job, there are ways to tap the funds.

If buying a home is your long-term goal, this guide on how to buy your first home pairs perfectly with a Roth strategy.

What is the best time to start ?

If you are a teenager with a job, you have a superpower: Time. Most 13-year-olds are spending their money on video games and snacks. If you put $1,000 into a Roth IRA at 13 and never touch it again, by the time you’re 63, that $1,000 could be worth nearly $120,000. That’s for doing nothing for 50 years.

If you’re a parent reading this, open a Custodial Roth IRA for your kid. As long as they have “earned income” (even from babysitting or mowing lawns, as long as it’s documented), you can jumpstart their wealth.

Common Mistakes to Avoid (The “Don’t Do This” List)

Even smart people mess this up. Here’s how to avoid being one of them.

- Mistake 1: Not Investing the Money. I’ll say it again: a Roth IRA is just a bucket. If you don’t buy stocks or funds inside the bucket, you’re just wasting your time.

- Mistake 2: Forgetting the 5-Year Rule. Even if you are 60 years old, you usually have to wait until the account has been open for 5 years before you can take the earnings out tax-free. Open it now, even if you only put $10 in it, just to start the clock.

- Mistake 3: Withdrawing Contributions because of a “Market Dip.” The stock market goes up and down. If you see your balance drop from $5,000 to $4,000, do NOT panic and pull the money out. That’s how you lose. Leave it alone.

- Mistake 4: Not Automating. If you try to remember to contribute every month, you’ll fail. Set up an “Auto-Transfer” from your bank for $100 a week. You won’t even miss the money after a month.

Frequently Asked Questions

Is a Roth IRA better than a 401k?

It’s not an “either/or.” Usually, you want to do both. If your job offers a 401k match, do that first (it’s free money). Then, try to max out your Roth IRA.

What if I lose my job?

Stop contributing. You don’t “owe” the Roth IRA anything. It’s your account. You can pick back up whenever you get back on your feet.

Can I have more than one Roth IRA?

Sure, but the contribution limit is total. You can’t put $7,000 into a Fidelity Roth and another $7,000 into a Vanguard Roth. The IRS will find you and they will be annoyed.

What happens to the money when I die?

Your heirs get it. And here’s the best part: they get it tax-free too. It is one of the greatest wealth-transfer tools in history.

Final Thoughts: Just Do It

The biggest enemy of wealth isn’t the stock market—it’s procrastination. Every year you wait to open a Roth IRA is a year of tax-free growth you can never get back.

You don’t need to be a “finance person.” You don’t need to watch the news. You just need to open an account, buy a broad index fund, and let time do the heavy lifting. Your 65-year-old self will thank you for being smart enough to read this today.

Now, go open that account.