Does Your Credit Score Matter When Renting a Home?

Introduction

When you start looking for a new home or apartment to rent, one of the first questions that might cross your mind is, “Does Your Credit Score Matter When Renting a Home?” You’re not applying for a loan, you’re simply renting a place to live—so why would a number on a credit report make a difference?

The truth is, your credit score often plays a bigger role than many realize. Landlords and property managers use it to measure your reliability and financial stability. It’s a snapshot of how responsibly you’ve handled money and credit in the past. A strong score can open doors, while a poor one can close them.

This guide will explain why credit scores matter when renting, what landlords look for, how to prepare, and what to do if your score isn’t where you want it to be.

Why Landlords Look at Credit Scores

From a landlord’s point of view, renting a property is a business decision. They want to ensure their tenants can pay rent on time and take care of the property. A credit score gives them insight into how responsible and consistent someone is with financial obligations.

Landlords don’t want to chase rent every month or risk late payments. Your credit report shows your payment history, how much debt you carry, and whether you’ve had trouble managing credit in the past. Consistent payments and low credit use signal reliability.

If your score is strong, it reassures landlords that you’re less likely to cause financial headaches. But even if your credit isn’t perfect, it doesn’t mean you’re out of options.

What Credit Score Is Good Enough to Rent?

Most landlords prefer tenants with credit scores in the “good” range—typically 670 or higher on the FICO scale. But this number isn’t a hard rule. Some property managers accept lower scores if other factors look promising, such as stable income, solid references, or a larger security deposit.

If your score is between 580 and 670, you might still qualify but may need to offer extra reassurance. For instance, landlords may ask for an additional month’s rent upfront, a co-signer, or proof of consistent payment history.

For luxury rentals or highly competitive areas, higher credit scores—above 700—are often expected. On the other hand, smaller private landlords may be more flexible and willing to look at the full picture instead of just a number.

What Landlords See When They Check Your Credit

When you apply for a rental, the landlord usually requests permission to check your credit. Most use a “soft inquiry,” which won’t affect your score. Some large property management companies, however, might use a “hard inquiry,” which can cause a small, temporary dip.

A landlord’s credit report includes:

- Payment history: Records of on-time and late payments.

- Credit utilization: The amount of credit used compared to available limits.

- Public records: Bankruptcies, evictions, or judgments.

- Outstanding debts: Total balances across credit accounts.

- Length of credit history: How long you’ve been using credit responsibly.

They use this information to assess risk. A pattern of missed payments or high debt may raise concerns, while consistent, responsible use of credit builds trust.

How a Poor Credit Score Affects Your Rental Application

A low credit score doesn’t automatically mean rejection, but it can make renting more challenging. Landlords may worry about missed payments or financial instability. Here’s how poor credit can affect your application:

- Higher security deposit: Landlords may request extra funds upfront to reduce their risk.

- Co-signer requirement: You might need someone with better credit to guarantee payment.

- Limited housing options: Some high-demand properties won’t consider applicants with poor credit.

- Higher scrutiny: You may be asked to provide proof of income, employment, or past landlord references.

Even so, many landlords will give you a chance if you’re upfront about your situation and show that you can manage rent responsibly.

What If You Have No Credit History?

If you’re new to credit or just starting out, not having a credit history can make it hard for landlords to assess your reliability. They don’t see red flags—just a lack of information.

You can make up for that by:

- Providing proof of consistent income.

- Offering a larger security deposit.

- Getting a co-signer or guarantor.

- Showing rent receipts from previous landlords or roommates.

Some landlords value steady employment and clear communication more than a credit score. The key is to present yourself as a low-risk tenant who pays on time and respects the property.

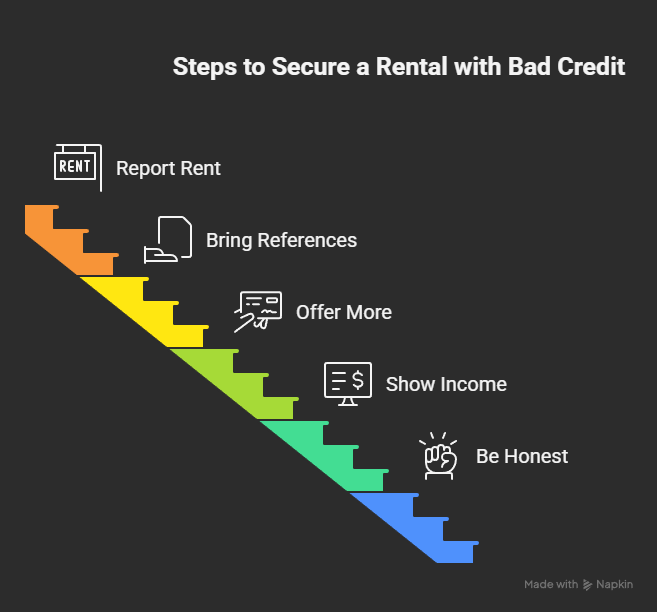

How to Rent with Bad Credit: Practical Strategies

Having less-than-perfect credit doesn’t have to stop you from getting a great home. Here are real-world ways to overcome credit challenges:

1. Be Honest and Communicate Early

If your credit isn’t ideal, it’s better to explain upfront. Share the reason—like medical bills, a divorce, or a temporary job loss—and what steps you’ve taken to fix it. Honesty often goes further than silence.

2. Show Proof of Steady Income

Provide recent pay stubs, tax returns, or bank statements. A landlord who sees consistent income may overlook a low score.

3. Offer a Larger Deposit or Prepay Rent

Putting down a bigger deposit or paying a few months’ rent in advance demonstrates commitment and reliability.

4. Bring References

Letters from past landlords, employers, or even roommates can help establish credibility.

5. Consider Rent Reporting Services

Services like Axcessrent or RentTrack can help you build credit by reporting rent payments to credit bureaus. That way, each on-time payment boosts your credit history.

Improving Your Credit Before Renting

If you have a few months before moving, start working on your credit. Small, consistent actions can lead to big improvements.

- Check your credit reports from all three major bureaus and dispute any errors.

- Pay all bills on time. Even one late payment can hurt your score.

- Reduce credit card balances to lower your utilization rate.

- Avoid opening new accounts right before applying to rent.

- Keep old accounts open to lengthen your credit history.

- Use rent reporting services to add positive history to your file.

Improving credit takes patience, but even modest gains can make a noticeable difference in approval odds and rental terms.

Beyond Credit: Other Things Landlords Consider

Landlords rarely base their decision on credit alone. They look at a mix of factors to evaluate whether you’re the right tenant.

- Income stability: Most require your income to be at least 2.5 to 3 times the rent.

- Employment status: Steady, long-term employment reassures landlords.

- Rental history: Prior evictions or disputes can raise concerns.

- References: A positive landlord reference can outweigh a lower score.

- Interview or application behavior: Responsiveness, honesty, and organization count.

Even if your credit isn’t perfect, presenting yourself as a respectful, communicative, and stable tenant can tip the decision in your favor.

How Rent Payments Can Build Credit

Traditionally, rent payments haven’t appeared on credit reports. That means you could pay on time for years without seeing any benefit on your credit score. Thankfully, that’s changing.

Today, several rent reporting services can add your rent history to major credit bureaus. If your landlord participates—or you sign up independently—those payments become part of your credit profile. Over time, this positive record can raise your score and make future rentals easier.

It’s a simple, low-risk way to build credit without taking on new debt.

Preparing for a Rental Application

Before applying, take a few simple steps to strengthen your position:

- Know your credit score so there are no surprises.

- Gather income documents like pay slips or tax returns.

- Request reference letters from past landlords.

- Explain any negative marks with a brief, honest note.

- Show you’re organized—fill out the application neatly and promptly.

Being prepared not only increases your chances of approval but also shows professionalism and reliability—traits landlords value highly.

Real Example: Turning a Weak Credit into Approval

Emily had a credit score of 615 after losing her job during the pandemic. When she applied for a new apartment, she was upfront about her credit issues and brought a letter from her employer showing stable new income. She also provided proof of 18 months of on-time rent payments.

The landlord appreciated her honesty and accepted her application with a slightly higher deposit. Within a year, Emily’s credit score improved, and she successfully renewed her lease at better terms.

Her story proves that preparation, transparency, and consistency can outweigh a less-than-perfect credit score.

Frequently Asked Questions

1. Do all landlords check credit scores?

Not all, but most do—especially larger property management companies. Smaller, independent landlords may rely more on personal references and income proof.

2. Will a good credit score guarantee approval?

No, but it increases your chances. Landlords still consider income, rental history, and background checks.

3. Can I rent a home with no credit history?

Yes. You can strengthen your application with a co-signer, larger deposit, or solid income documentation.

4. Does paying rent improve my credit score?

Only if your payments are reported to credit bureaus. Consider using a rent reporting service.

5. How far back do landlords check credit history?

Most review the past seven years, focusing on recent payment behavior and major credit issues.

6. Can a bad credit score stop me from renting?

It can make things harder, but it doesn’t have to stop you. Preparation, communication, and documentation can help you get approved.

Conclusion

Your credit score does matter when renting a home, but it’s only one piece of the puzzle. Landlords use it as a tool to measure responsibility and financial consistency, but many also weigh income, references, and honesty heavily.

If your score isn’t perfect, focus on what you can control: pay on time, reduce debts, and communicate openly. Over time, your efforts will pay off—not only improving your credit score but also helping you secure better rental opportunities.

Renting with confidence starts with understanding how credit works and taking steady steps toward improvement. The more informed and proactive you are, the easier it becomes to find a home that fits both your budget and your goals.