Does Student Loan Debt Affect Your Credit Score?

Understanding how student loan debt affect your credit score is a critical step in modern financial literacy. Whether you are a current student, a recent graduate entering repayment, or a parent co-signer, your student loan behavior is one of the most significant factors in determining your “creditworthiness.”

In this comprehensive guide, we will explore the nuances of credit reporting, the mechanics of credit scoring models (FICO and VantageScore), and provide actionable strategies to ensure your education debt builds—rather than breaks—your financial future.

Quick Answer: How Do Student Loans Affect Credit?

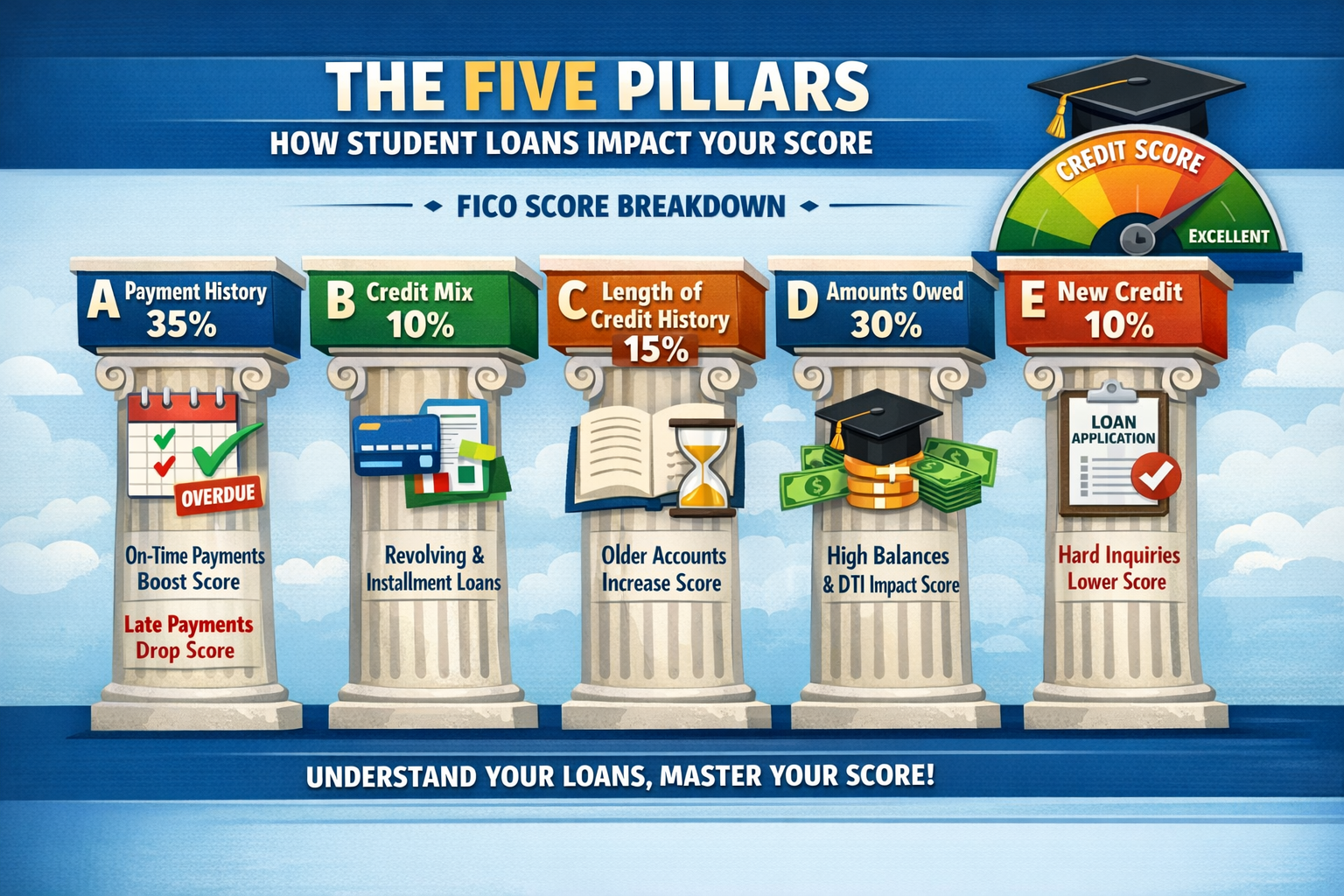

Yes, student loans affect your credit score in several ways. Because student loans are reported to the three major credit bureaus (Equifax, Experian, and TransUnion), they impact the five core pillars of your credit score: payment history, credit mix, length of credit history, amounts owed, and new credit inquiries.

1. The Five Pillars: How Student Loans Impact Your Score

To understand why student loans matter, we have to look at how credit scores are calculated. Most lenders use FICO scores, which are weighted as follows:

A. Payment History (35% – The Most Important)

This is the single biggest factor. When you make a student loan payment on time, your servicer reports it to the bureaus.

- The Positive: A 10-year history of on-time payments creates a “thick” credit file that signals to banks you are a low-risk borrower.

- The Negative: A single payment that is 30 days late can cause a score to drop by 50 to 100 points.

B. Credit Mix (10%)

Lenders like to see that you can handle different types of debt. There are two main types:

- Revolving Credit: Credit cards (where the balance goes up and down).

- Installment Credit: Student loans, mortgages, and auto loans (fixed payments over a set time). Having a student loan adds to your “Credit Mix,” which can actually improve your score compared to someone who only has a credit card.

C. Length of Credit History (15%)

The “age” of your accounts matters. Student loans are often the oldest accounts on a young person’s credit report. Keeping these accounts open for the duration of the loan term helps increase the average age of your accounts, which is a net positive for your score.

D. Amounts Owed / Credit Utilization (30%)

While “credit utilization” usually refers to credit cards, the total amount of debt you owe compared to your initial loan amount still plays a role. If you have high student loan balances that aren’t decreasing because of high interest, it can impact your “debt-to-income” (DTI) ratio, which—while not part of your credit score—is a major factor when applying for a mortgage.

E. New Credit (10%)

Every time you apply for a new student loan (especially private loans), a “hard inquiry” is placed on your report. This causes a temporary, minor dip in your score (usually less than 5 points).

2. Does Student Loan Forbearance Affect Your Credit Score?

One of the most searched questions is whether pausing payments hurts your credit.

No, official student loan forbearance or deferment does not negatively impact your credit score. Under the CARES Act and standard reporting guidelines, lenders report loans in forbearance as “current.”

However, there is a catch: Interest usually continues to accrue. This means your total balance will grow. While your score won’t drop due to the “pause,” your higher balance might be viewed less favorably by mortgage lenders in the future.

3. Does Not Paying Student Loans Affect Credit Score?

The consequences of “going dark” on your student loans are severe and long-lasting.

- Delinquency: Once you are 30 days late, the lender can report you. Your score will take an immediate hit.

- Default: For federal loans, default typically occurs after 270 days of non-payment.

- The “7-Year Rule”: A default remains on your credit report for seven years from the date of the first missed payment. This can prevent you from getting credit cards, car loans, or even passing a background check for certain jobs.

4. Does Paying Off Student Loans Help Credit Score?

It seems logical: paying off debt should make your score go up. However, many graduates are shocked to see their score drop slightly after making their final payment.

Why does this happen? When you pay off a student loan, that “installment account” is marked as closed. This can:

- Reduce your credit mix (if you have no other installment loans).

- Decrease the average age of your accounts (if the student loan was your oldest account).

The Strategy: Don’t let this discourage you. The dip is temporary and minor. The long-term benefit of being debt-free far outweighs the small, short-term drop in your credit score.

5. What is a Good Credit Score for a College Student?

Most college students start with a “thin” file or no score at all.

- 630 – 689: Fair Credit (A typical starting point for students with a few years of loan history).

- 690 – 719: Good Credit.

- 720+: Excellent Credit.

If you are a student, aiming for a 700 is a fantastic goal. This will allow you to qualify for most car loans and apartment rentals without needing a co-signer.

6. Federal vs. Private Student Loans & Credit

| Feature | Federal Student Loans | Private Student Loans |

|---|---|---|

| Credit Check Required? | No (except for PLUS loans) | Yes, usually requires a high score |

| Co-signer Needed? | No | Almost always for students |

| Credit Reporting | Reported monthly | Reported monthly |

| Default Timeline | 270 days | Can be as little as 90 days |

7. Expert Tips for students

To ensure your student loans are working for you, follow these three rules:

- Update Your Contact Info: Many students miss payments simply because the bill went to an old college address. Ensure your loan servicer has your current email and phone number.

- Pay the Interest (if you can): If you have unsubsidized loans, interest builds while you are in school. Paying just $25 a month toward that interest can keep your total balance from ballooning, which helps your “amounts owed” category.

- Use Auto-Pay: Most servicers offer a 0.25% interest rate deduction if you sign up for auto-pay. It also guarantees you never have a late payment reported to the bureaus.

Summary

Student loans are a double-edged sword for credit scores. They provide the necessary “credit mix” and “account age” to build a strong financial foundation for young adults. However, due to the high weight of “payment history” (35%) in FICO models, any delinquency can be catastrophic. To maintain a high score, borrowers should prioritize on-time payments, consider auto-pay for interest discounts, and communicate with servicers for official forbearance if financial hardship occurs.

Frequently Asked Questions

Does student loan debt affect your credit score?

Yes. Student loans are installment debts that appear on your credit report. They impact your payment history, the average age of your accounts, and your total debt balance.

Can student loans affect your credit score if you haven’t graduated?

Yes. Even if you are in a “grace period” or “in-school deferment,” the accounts are listed on your report. While you aren’t required to pay, the age of the account is already helping you build a credit history.

How much will my credit score drop if I miss a student loan payment?

Depending on your starting score, a single 30-day late payment can cause a drop of 60 to 100 points. The higher your initial score, the more points you stand to lose.

Does consolidated student loan affect credit score?

Consolidating can cause a temporary dip because it closes old accounts and opens a new one (lowering your average account age). However, it can help your score in the long run by making payments more manageable and consistent.

Is student loan debt “good debt” for credit scores?

Generally, yes. Because it is an installment loan with typically lower interest rates than credit cards, it is viewed by scoring models as a positive indicator of long-term financial planning—provided payments are made on time.