Does Getting a New Credit Card Hurt Your Credit Score?

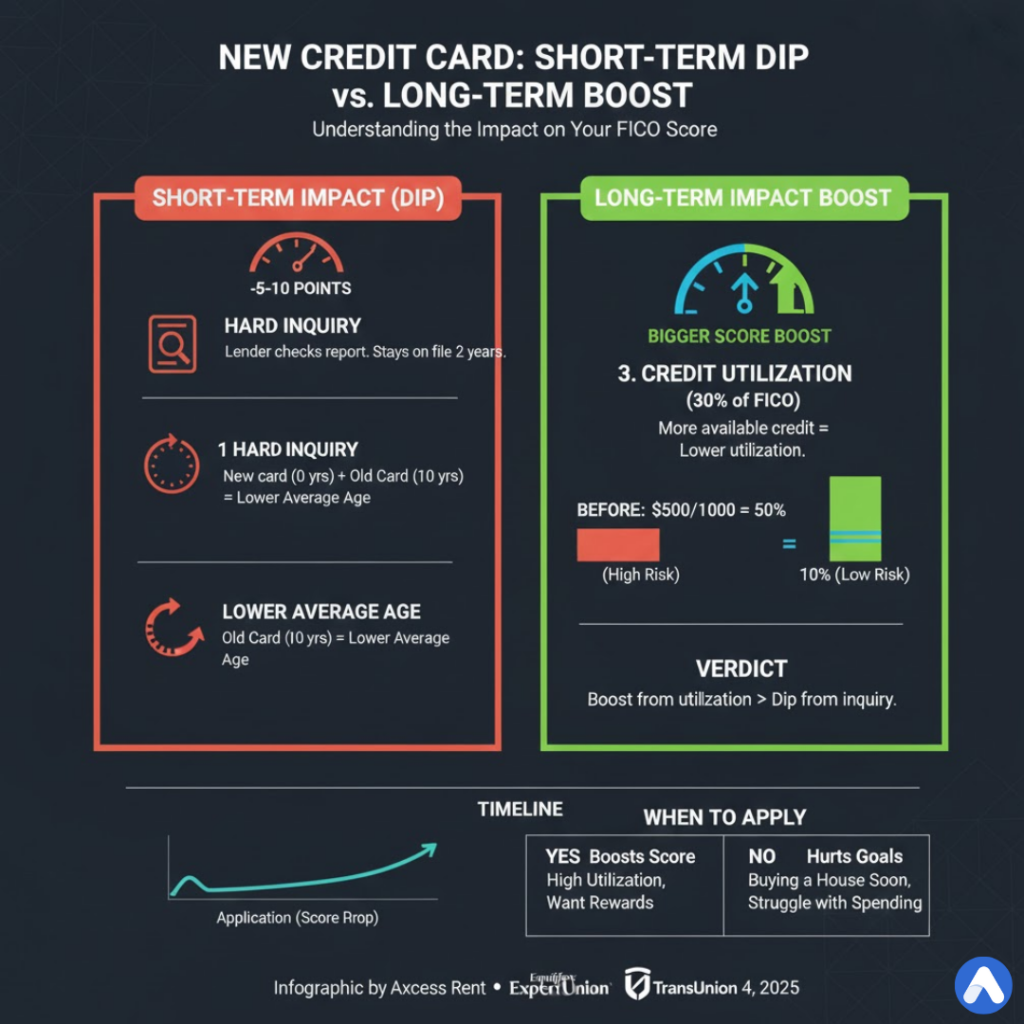

Yes, getting a new credit card will likely lower your score by 5 to 10 points temporarily. However, this drop is usually short-lived. In the long run, opening a new card is one of the most effective ways to help your credit score grow higher than it was before.

It sounds contradictory, right? How can something that hurts your score also help it?

To understand this, you have to look at the timeline. There is a “Short-Term Dip” caused by the application, followed by a “Long-Term Boost” caused by the extra credit limit.

The Short-Term Impact: Why Your Score Drops

When you apply for a new credit card, two things happen immediately that negatively affect your score.

1. The Hard Inquiry (The “Dip”)

Every time you submit a formal application for credit, the lender pulls your credit report. This is called a Hard Inquiry.

- Impact: This typically knocks 5–10 points off your score.

- Duration: The impact fades within a few months, though the inquiry stays on your report for two years.

2. Lower Average Age of Accounts

As we discussed in previous guides, 15% of your score is based on the length of your credit history.

- The Math: If you have one credit card that is 10 years old, your average age is 10 years. If you open a new card today (0 years old), your average suddenly drops to 5 years ((10+0) ÷ 2).

- Impact: This can cause a slight score drop, especially for people with “thin” credit files.

The Long-Term Impact: Why Your Score Rises

Despite the initial drop, getting a new credit card is usually a smart move for your score because of Credit Utilization.

Utilization makes up 30% of your FICO score. It measures how much of your limit you are using.

- Scenario A (Before New Card): You have a $1,000 limit and spend $500. Your utilization is 50% (High risk).

- Scenario B (After New Card): You get a new card with a $4,000 limit. Now your total limit is $5,000. If you still spend $500, your utilization drops to 10% (Excellent).

The Verdict: The benefit of lowering your utilization from 50% to 10% far outweighs the small 5-point penalty from the hard inquiry.

Will Getting a New Credit Card Stop Recurring Payments?

This is a very common question, and the answer depends on whether you mean an additional card or a replacement card.

Scenario 1: You opened an additional account

If you open a brand new Visa card but keep your old Mastercard open, your recurring payments (Netflix, Gym, Utilities) on the old Mastercard will continue as normal. Nothing stops. You would need to manually move them to the new card if you want to.

Scenario 2: You got a replacement card (Lost/Stolen/Expired)

If your bank sends you a new card with a new number because your old one was lost or expired:

- Yes, payments might stop: Any merchant trying to charge the old number will likely be declined.

- The Exception: Many big subscription services (like Amazon or Netflix) use “Automatic Biller Updater” services. Banks often send the new card info directly to these major merchants so your service isn’t interrupted. However, smaller bills (like a local gym or HOA fee) will almost certainly fail until you update them manually.

When Does Getting a New Card Help Your Credit Score?

You should consider getting a new card if:

- Your utilization is high: You pay your bills on full, but your limits are so low that your score is suffering.

- You have a “Thin File”: You only have one account. Adding a second account improves your “Credit Mix” and thickens your file.

- You want rewards: You have excellent credit and want to earn cash back or travel points.

When Does Getting a New Card Hurt Your Credit?

You should avoid applying for new credit if:

- You are applying for a mortgage soon: If you plan to buy a house in the next 6 months, do not open new cards. Mortgage lenders are very sensitive to “New Credit” inquiries and new debts.

- You struggle with spending: If a new card means you will spend money you don’t have, the debt will hurt your score far more than the credit limit will help it.

Frequently Asked Questions (FAQ)

Does getting a new credit card lower your score immediately?

Yes. You will typically see a small drop (5–10 points) as soon as the hard inquiry hits your report. However, if you keep the balance low, your score usually recovers and increases within 2–3 months.

Will credit card hurt my credit if I don’t use it?

No, simply having the card open helps your score because it increases your total available credit limit, which lowers your utilization ratio. You do not need to carry a balance to benefit from the card.

Does getting denied for a credit card hurt your score?

The denial itself does not hurt your score, but the Hard Inquiry does. Whether you are approved or denied, the inquiry remains on your report. This is why you should only apply for cards you are likely to get.