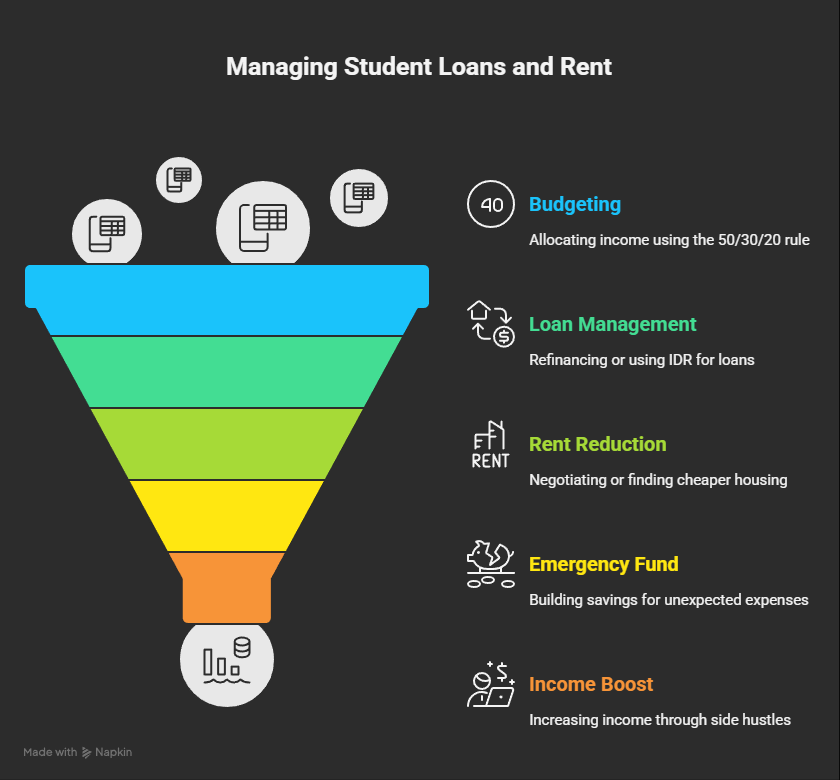

How to balance Student Loans and Rent?

To balance Student loans and pay rent eat up a big chunk of your budget. If you’re paying $400 a month on loans and $1,200 on rent, it feels like a constant juggle. But you can manage both without drowning. This guide walks you through balancing student loans and rent. It also shares refinancing tips to get better loan terms, freeing up cash for rent. With practical steps and real examples, you’ll see how to make it work.

Why Balancing Student Loans and Rent Is Tough?

The average student loan debt is $37,000, per 2025 data. Rent for a one-bedroom averages $1,730 a month in cities. Add in groceries, utilities, and maybe a car payment, and your paycheck vanishes. Most people spend 50% or more of their income on rent and loans. That’s way above the recommended 30% for housing alone. It leaves little for savings or unexpected costs.

In 2025, federal loan rates hover around 5.5% for undergrads. Private loans can hit 6-10%. Rent prices rose 3% from last year. Wages? Barely budging. Refinancing loans can lower payments. Smart budgeting can stretch your rent dollars. This guide shows how.

Step-by-Step Guide

Here are 10 practical steps to manage both expenses. Start with your numbers and go from there.

Step 1: Track Your Spending

Pull up your bank statements. Write down what you pay for loans, rent, and other bills. Use a free app like Mint or a simple spreadsheet. For example: $350 for loans, $1,100 for rent, $400 for food and utilities. That’s $1,850. If you earn $4,000 a month, that’s 46% of your income. Over 50% is a red flag.

Fix: Cut small expenses. Skip takeout three times a week. Save $75. Put it toward loans or an emergency fund.

Step 2: Know Your Student Loan Details

Check your loan type: federal or private. Federal loans have fixed rates, around 5.5% for undergrads. Private loans vary, often 6-10%. Log in to your servicer’s site (Navient, SoFi, etc.) to see your balance, rate, and term.

Example: A $30,000 loan at 6% over 10 years means $333 a month. Refinance to 4%, and it drops to $304. That’s $29 more for rent each month.

Tip: Use StudentAid.gov for federal loans. It shows all your details.

Step 3: Build a Budget for Loans and Rent

Use the 50/30/20 rule: 50% for needs (rent, loans, food), 30% for wants (dining, fun), 20% for savings or debt. If rent and loans eat up 60%, cut back on wants.

Example: Income $4,000. Needs: $2,000 (rent $1,200, loans $400, food $400). Wants: $1,000 (movies $200, dining $300). Savings: $1,000.

Tools: Try YNAB or PocketGuard to track spending.

Step 4: Use Income-Driven Repayment for Federal Loans

Federal loans offer income-driven repayment (IDR) plans. These cap payments at 10-20% of your income. If you earn $40,000, your payment might drop from $350 to $200. Apply at StudentAid.gov. It’s free.

Pros: Lower payments. Possible forgiveness after 20-25 years.

Cons: Interest adds up. Forgiven amounts may be taxed.

This frees up $150 a month for rent or savings.

Step 5: Refinance Private Loans for Lower Rates

Refinancing private loans can cut your interest rate or monthly payment. Lenders like SoFi or Earnest offer 3-5% rates if your credit score is 670 or higher. Only refinance private loans—you lose federal benefits like IDR otherwise.

Steps:

- Check your score on Credit Karma.

- Compare rates on Credible or LendingTree.

- Apply if you qualify. No hard credit pull until approved.

Example: A $20,000 loan at 8% is $242 a month. Refi to 4%, it’s $198. That’s $44 saved monthly for rent.

Tip: Refi if the rate drops 1% or more. Compare at least three lenders.

Step 6: Lower Rent Costs

Rent is tough to change, but you can negotiate. Ask for a discount for signing a longer lease or paying on time. Or get a roommate—split $1,500 rent to $750 each. Moving to a cheaper area, like a suburb, can save 20% on rent.

Example: Jane got $50 off her $1,200 rent by signing a two-year lease. That’s $600 a year for loans.

Step 7: Build an Emergency Fund

Unexpected costs—like a $1,000 car repair—can derail your budget. An emergency fund covering 3-6 months of expenses helps. Start small: save $50 a week by cutting coffee runs.

This fund protects you from missing rent or loan payments. Late payments hurt your credit score.

Example: Mike saved $3,000. When his hours were cut, he paid rent and loans without stress.

Step 8: Boost Income with Side Hustles

Extra cash makes balancing easier. Drive for Uber, freelance on Upwork, or do tasks on TaskRabbit. Aim for $500 a month. Put it toward loans or rent.

In 2025, gig apps are everywhere. TaskRabbit pays $20/hour for small jobs.

Tip: Track gig income for taxes. You can deduct loan interest too.

Step 9: Look for Forgiveness or Assistance

Federal loans offer forgiveness programs. Public Service Loan Forgiveness (PSLF) cancels debt after 10 years in public sector jobs (teachers, nurses). Apply at StudentAid.gov.

For rent, check local programs. Section 8 or city housing grants help low-income renters.

Example: Lisa got $5,000 forgiven through PSLF. She used the savings for a new apartment deposit.

Step 10: Monitor and Adjust Regularly

Check your budget monthly. Use apps to track loan balances and rent payments. If rent rises, renegotiate or move. If loan payments feel high, refi again or switch to IDR.

Keep an eye on your credit score. Paying on time boosts it, which helps future refi.

How to refinancing for better loan terms ?

Refinancing can save you hundreds. Here’s how to do it right in 2025.

Tip 1: Check Your Credit First

You need a 670+ credit score for good rates. Check it free on Credit Karma. If it’s low, pay bills on time for 6 months to improve.

Tip 2: Shop Multiple Lenders

Compare 3-5 lenders. SoFi might offer 3.5%, Earnest 4%. Use Credible to see rates without hurting your score.

Example: A $25,000 loan at 7% is $295/month. Refi to 4%, it’s $250. That’s $540 saved a year.

Tip 3: Time Your Refi

Refi when rates drop or your credit improves. In 2025, rates are 4-6%. Wait for dips if possible. Don’t refi before big purchases like a car—hard inquiries lower your score.

Tip 4: Pick Fixed Rates

Fixed rates stay the same. Variable rates can jump. For budget stability, go fixed.

Tip 5: Consider a Co-Signer

If your credit is below 670, a co-signer with a strong score helps. You can release them after 12-24 on-time payments with some lenders.

Tip 6: Look for Lender Perks

Some lenders offer 0.25% rate cuts for auto-pay. Others have unemployment protection, pausing payments if you lose your job.

how to manage loans and rent on a low Income ?

If you earn $3,000 a month, it’s tight. Rent at $1,200 and loans at $300 leave $1,500 for everything else.

Steps:

- Apply for IDR to lower loans to $200.

- Get a roommate to cut rent to $600.

- Add $400 from a side hustle.

- Budget: $300 food, $200 transport, $400 savings.

Example: Tom earned $2,800. IDR cut his loans to $250. A roommate dropped rent to $700. He saved $350 a month.

State-Specific Considerations

Rent and loan rules vary by state in 2025:

- California: Rent control in cities like LA caps increases. Check local aid for renters.

- New York: High rent ($2,000+) makes roommates a must. PSLF is popular for public workers.

- Ohio: Lower rent ($1,000) helps. Flexible loan programs available.

- Florida: No rent control, but cheaper suburbs exist. Refi is easy with many lenders.

Check your state’s housing or consumer protection site for aid programs.

Tools and Resources

- StudentAid.gov: Check federal loan details and apply for IDR or PSLF.

- Credible: Compare refi rates for private loans.

- AxcessRent: Report rent payments to boost credit ($5–$10/month).

- Credit Karma: Free credit score tracking.

- Mint: Budgeting app for rent and loans.

- NFCC.org: Free financial counseling.

FAQs

How to Balance Student Loans and Rent?

Track your spending and budget 50% for needs (rent, loans). Use IDR for federal loans to cap payments at 10-20% of income. Refinance private loans for lower rates. Get a roommate or negotiate rent. Add a side hustle for extra cash. Build an emergency fund to avoid late payments.

What Are Student Loan Refi Tips?

Check your credit (670+ for best rates). Compare 3-5 lenders on Credible. Refi when rates drop (4-6% in 2025). Choose fixed rates for stability. Use a co-signer if needed. Look for perks like auto-pay discounts or unemployment protection.

Can Refinancing Lower My Loan Payments?

Yes. Refinancing a $20,000 loan from 7% to 4% cuts payments from $242 to $198 a month. That’s $44 saved for rent. Only refinance private loans to keep federal benefits. Use Credible to compare rates.

How Much of My Income Should Go to Rent and Loans?

Aim for 30-40% of income for rent and loans. Over 50% is risky. For example, on $4,000/month, keep rent at $1,200 and loans at $400 or less. Use IDR, roommates, or refi to lower costs.

What If I Can’t Pay Both Rent and Loans?

Contact your loan servicer for deferment or IDR. Check local rent assistance like Section 8. Cut non-essentials like subscriptions. Start a side hustle for $200–$500/month. Prioritize rent to avoid eviction.

Is Refinancing Worth It for Small Loans?

Yes, if the rate drops significantly. Refinancing a $10,000 loan from 7% to 4% saves $20/month. Use NerdWallet’s refi calculator to check savings. Ensure no fees eat up benefits.

How to Prioritize Student Loans vs. Rent Payments?

Prioritize rent to avoid eviction, which hurts credit and housing prospects. Pay loans next, as late payments drop your score by 50-100 points. Use IDR to lower loan payments if rent is high. Build an emergency fund to cover both.

Can I Refinance Student Loans and Rent Together?

Not directly, as rent isn’t a loan. But refinancing student loans frees up cash for rent. For example, lowering a $300 loan payment to $250 gives $50 more for rent. Use AxcessRent to report rent payments and boost credit, which helps future refi.

What Are the Risks of Refinancing Student Loans?

You lose federal benefits like IDR or forgiveness (e.g., PSLF). Variable rates may rise, increasing payments. Hard inquiries temporarily lower your score by 5-10 points. Mitigate by only refinancing private loans, choosing fixed rates, and comparing lenders.

Conclusion

Balancing student loans and rent is tough, but you can do it. Track your spending, budget smart, and refinance private loans for better terms. Use IDR for federal loans and negotiate rent. Side hustles and emergency funds give you a safety net. In 2025, tools like SoFi, Credible, and AxcessRent make it easier. Start today: check your loans on StudentAid.gov, compare refi rates, and explore rent assistance. Your financial freedom is worth the effort. Visit AxcessRent for more credit-building tips.