Average Credit Score by Age in 2025: Compare and Improve Yours

Introduction

Your credit score shapes your financial life. It determines loan approvals, interest rates, and even job opportunities. In 2025, many ask: what’s the average credit score by age? Understanding this helps you see where you stand and how to improve. Scores generally increase with age due to experience, income stability, and better financial habits.

The national average FICO score in 2025 is 715, according to Experian data. Younger generations like Gen Z score lower, while older groups like Boomers excel. This article dives into averages by age group, explains why they vary, and offers actionable tips to improve your score. With economic challenges like rising interest rates, a strong credit score is more valuable than ever. Read on to learn how your score compares and what you can do to enhance it.

What Is a Credit Score?

A credit score is a three-digit number reflecting your creditworthiness. It predicts how likely you are to repay debts. Scores range from 300 to 850, with higher numbers indicating better credit. Lenders, landlords, and insurers use it to assess risk.

FICO and VantageScore are the main models. FICO dominates, used in 90% of lending decisions. Scores come from credit reports by Equifax, Experian, and TransUnion. These reports track your payment history, debts, and credit use.

Why Credit Scores Matter

A high score means better loan terms. For example, a 750 score might get a 4% mortgage rate, while a 650 score could mean 5%, costing thousands extra over time. In 2025, with rates high, this matters more. Scores also affect:

- Car loans: Lower rates save money.

- Credit cards: Higher scores unlock better rewards.

- Rentals: Landlords check scores.

- Jobs: Some employers review credit.

Knowing your score helps you plan.

How Credit Scores Are Calculated

Credit scores use five key factors. Each has a different impact.

Payment History (35%)

Paying on time is critical. Late payments, even by 30 days, hurt. They stay on your report for seven years.

Amounts Owed (30%)

This is credit utilization—how much you owe versus your credit limits. Keep it below 30%. High use signals risk.

Length of Credit History (15%)

Longer histories boost scores. Includes age of oldest account and average account age.

New Credit (10%)

Applying for many accounts triggers hard inquiries. Each can drop your score by 5-10 points. They last two years.

Credit Mix (10%)

Having both revolving (credit cards) and installment (loans) credit helps. Shows you can manage variety.

FICO 8 and 9 are widely used in 2025. They’re forgiving on small medical debts.

Average Credit Score by Age Group in 2025

Experian’s 2024 data, relevant for 2025, shows scores rising with age. Below is a detailed look.

Average Credit Scores Table

Compare your score here.

| Age Group | Generation | Average FICO Score |

|---|---|---|

| 18-27 | Gen Z | 681 |

| 28-43 | Millennials | 691 |

| 44-59 | Gen X | 709 |

| 60-78 | Baby Boomers | 746 |

| 79+ | Silent Generation | 760 |

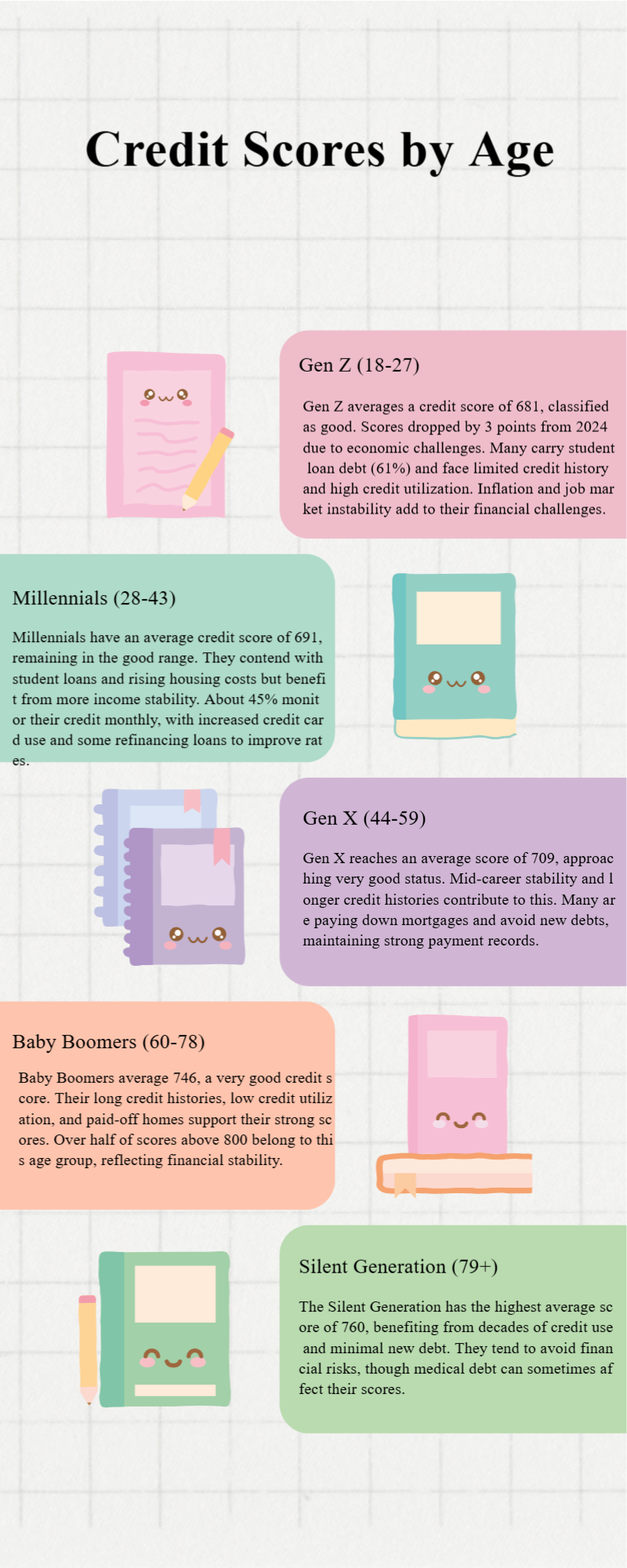

18-27: Gen Z (Average 681)

Young adults start at 681, in the good range (670-739). Scores dropped 3 points from 2024 due to economic pressures. Many have student loans, with 61% carrying debt. Limited credit history and high utilization hurt.

Challenges: Inflation and job market issues. Many lack savings.

28-43: Millennials (Average 691)

Millennials score 691, still good. They face student loans and rising housing costs. More income stability helps. About 45% monitor scores monthly, per FICO.

Trends: Credit card use up. Some refinance loans for better rates.

44-59: Gen X (Average 709)

Gen X hits 709, nearing very good (740-799). Mid-career stability and longer histories help. Many pay down mortgages.

Factors: Fewer new debts. Strong payment records.

60-78: Baby Boomers (Average 746)

Boomers average 746, very good. Long histories and low utilization drive this. 55.5% of scores above 800 are 60+.

Advantages: Paid-off homes, stable finances.

79+: Silent Generation (Average 760)

The highest at 760. Decades of credit use and minimal new debt help. Many avoid financial risks.

Note: Medical debt can lower scores for some.

Why Credit Scores Increase with Age

Scores rise as people age for clear reasons.

Longer Credit History

Older accounts show reliability. A 20-year-old card boosts scores.

Better Financial Habits

Experience reduces missed payments. Older groups budget better.

Higher Incomes

More earnings mean easier debt repayment. Median income for 45-54 is $90,000, versus $40,000 for 18-24.

Less New Debt

Younger groups borrow for education or homes. Older ones focus on payoff.

Exceptions exist. Medical bills or late-life loans can hurt.

Factors Influencing Credit Scores by Age

Other elements shape scores.

Income and Employment

Higher income correlates with better scores. Stable jobs help Gen X and Boomers.

Geographic Location

Scores vary by state. Minnesota averages 742; Mississippi, 680. Income and education play roles.

Debt Types

Student loans burden Gen Z. Mortgages, if paid well, help older groups.

Economic Conditions

In 2025, high rates increase delinquencies. Gen Z sees 5% late payments, per Experian.

Credit Access

Younger groups may overuse cards. Older ones have more options.

How to Check Your Credit Score

You can check your score for free.

AnnualCreditReport.com

Get weekly reports from all three bureaus. Federal law ensures access.

Credit Card Issuers

Banks like Chase offer free scores. Check statements or apps.

Third-Party Apps

Credit Karma or Experian apps show VantageScores. Not FICO, but close.

Review monthly. Fix errors fast.

Tips to Improve Your Credit Score at Any Age

Boosting your score is possible. Here’s how.

For Gen Z (18-27)

- Start Early: Get a secured card. Pay in full monthly.

- Report Rent: Services like Experian Boost add rent payments.

- Limit Cards: One or two is enough.

- Build Savings: Avoid relying on credit.

Example: Pay a $500 card balance monthly to build history.

For Millennials (28-43)

- Pay Down Debt: Use debt avalanche (highest interest first).

- Avoid New Cards: Too many inquiries hurt.

- Monitor Regularly: Check for fraud, common in this group.

- Refinance: Lower loan rates if possible.

Example: Reduce $10,000 card debt to drop utilization from 80% to 20%.

For Gen X (44-59)

- Diversify Credit: Add a small loan if only using cards.

- Plan Ahead: Pay off debts before retirement.

- Negotiate Rates: Ask for lower card APRs.

- Keep Accounts Open: Maintain history.

Example: Keep a 15-year-old card active with small charges.

For Boomers and Silent Generation (60+)

- Maintain Habits: Continue timely payments.

- Close Carefully: Only shut high-fee accounts.

- Protect from Scams: Fraud targets seniors.

- Downsize Debt: Pay off before fixed income.

Example: Pay off a car loan to lower utilization.

Universal Tips

- Automate Payments: Never miss a due date.

- Dispute Errors: Fix wrong report entries.

- Keep Utilization Low: Under 30% is ideal.

- Limit Inquiries: Apply sparingly.

- Build Emergency Fund: Avoid credit reliance.

Changes take 3-6 months. Be patient.

Common Myths About Credit Scores by Age

Misconceptions can mislead.

Myth: Young Can’t Have High Scores

Truth: A 25-year-old with good habits can hit 750.

Myth: Scores Drop with Age

Truth: They rise with discipline.

Myth: Checking Scores Hurts

Truth: Soft inquiries are harmless.

Myth: Closing Accounts Helps

Truth: It often raises utilization, hurting scores.

Myth: All Debt Is Bad

Truth: Managed debt builds credit.

Know the facts to avoid mistakes.

Credit Score Ranges Explained

Understand where you fall.

- Poor (300-579): Hard to get loans.

- Fair (580-669): Limited options, high rates.

- Good (670-739): Decent terms.

- Very Good (740-799): Great rates.

- Excellent (800-850): Best deals.

Aim for 670 or higher.

Credit Score Trends in 2025

National average holds at 715. Key trends:

- Gen Z Decline: Down to 681 from 684.

- Rising Utilization: Average 30%, up 2%.

- Delinquencies Up: 4% of accounts late, per FICO.

- Medical Debt Impact: Lessened by new FICO rules.

Economic pressures like 7% mortgage rates hurt.

How Average Credit Scores Vary by State

Location affects scores.

- Top States: Minnesota (742), Vermont (739), Wisconsin (737).

- Bottom States: Mississippi (680), Louisiana (684), Alabama (686).

- Factors: Income, education, cost of living.

Urban areas score higher than rural.

The Impact of Credit Scores on Life Milestones

Buying a Home

A credit score of 740 or higher secures low mortgage rates, around 4%, saving thousands over the loan’s life. Scores below 670 often face rates above 6%, increasing costs significantly. Lenders view higher scores as lower risk, offering better terms. Check your score before applying to optimize financing options.

Renting

Landlords typically require a credit score of 650 or above to approve rentals. Lower scores may demand a cosigner or higher deposit to offset risk. A strong score signals reliability, reducing hurdles in competitive markets. Monitor your score to avoid surprises when applying for apartments or leases.

Car Loans

Good credit scores, ideally 670+, secure lower interest rates on car loans, saving thousands over the loan term. Poor scores lead to higher rates, increasing monthly payments. Lenders use scores to assess repayment likelihood. Compare offers and improve your score to reduce costs when financing a vehicle.

Jobs

Some employers check credit scores for roles involving financial responsibility. Poor scores, below 650, may signal mismanagement, potentially blocking hires. High scores demonstrate reliability. Check job requirements and maintain a strong score to avoid career barriers, especially in finance or management positions. Regularly monitor your credit report.

Retirement

High credit scores, ideally 740+, help secure loans or credit lines in retirement, especially for unexpected expenses. Poor scores limit options, raising costs on fixed incomes. Maintaining a strong score ensures flexibility for late-life financial needs, like home repairs or medical costs. Plan early to preserve credit health.

Case Studies: Real-Life Credit Journeys

Gen Z Success

Lily, 23, boosted her score from 640 to 710 by getting a secured credit card, paying rent on time via reporting services, and maintaining 15% utilization. Her disciplined habits built a strong foundation early, showing young adults can achieve good credit quickly.

Millennial Recovery

Mark, 35, improved from 600 to 690 by paying off $12,000 in credit card debt using the avalanche method, targeting high-interest balances first. This strategic approach reduced costs and utilization, demonstrating recovery is possible with focused debt repayment efforts.

Gen X Stability

Tina, 50, maintains a 760 score by keeping old accounts open for history and paying mortgages early. Her stable habits, like low utilization and consistent payments, ensure ongoing financial security, illustrating mid-life discipline’s role in high scores.

Boomer Excellence

Robert, 65, sustains an 820 score through a long credit history and avoiding new debt. By focusing on timely payments and minimal borrowing, he exemplifies how lifelong consistency leads to excellent credit, benefiting retirement flexibility.

Tools and Resources for Credit Building

Use these to improve.

- Axcessrent: Rent payments.

- Credit Karma: Free VantageScore tracking.

- MyFICO: Detailed FICO insights.

- Nonprofits: National Foundation for Credit Counseling.

Start with free options.

Conclusion

In 2025, average credit scores by age range from 681 for Gen Z to 760 for the Silent Generation. Scores rise with experience, income, and discipline. The national average is 715, but your score depends on habits. Pay on time, keep debt low, and check reports regularly. No matter your age, you can improve your score with consistent effort. Start today to secure better financial opportunities.

Frequently Asked Questions

What’s a Good Credit Score for My Age?

670+ is good. Older groups aim for 740+.

Why Is My Score Below Average?

Check for late payments, high debt, or errors.

How Often Should I Check My Score?

Monthly to catch issues.

Does Marriage Combine Scores?

No, scores stay individual.

Can Medical Debt Hurt My Score?

Less impact in 2025, but unpaid bills still hurt.