Debt Snowball vs Debt Avalanche: Which Method is Better?

If you are serious about becoming debt-free, you have likely encountered the two titans of debt payoff strategy: the Debt Avalanche and the Debt Snowball. Both methods focus on creating momentum by making minimum payments on all debts while aggressively targeting one debt at a time.

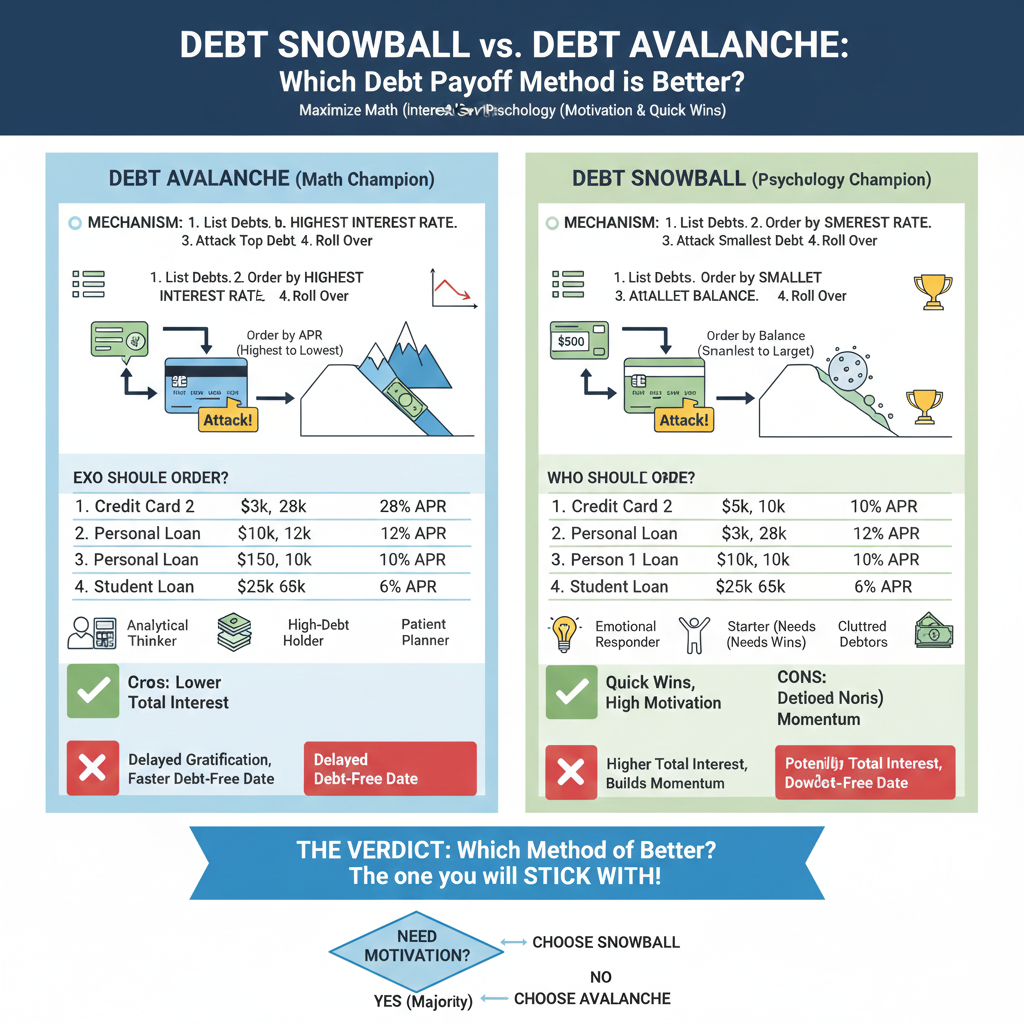

However, their fundamental approaches are completely different, forcing you to choose between maximizing math (interest savings) and maximizing psychology (motivation and quick wins).

Choosing the wrong method can lead to burnout. Choosing the right one can save you thousands of dollars and shave years off your debt journey.

What is the Debt Avalanche Method?

The Debt Avalanche method is the most mathematically efficient way to eliminate debt. It prioritizes saving money by focusing on debts with the highest interest rates first.

The Mechanism of the Debt Avalanche

- List all your debts: Include the total balance, the minimum monthly payment, and the interest rate (APR).

- Order by Interest Rate (APR): Arrange the list from highest interest rate to lowest interest rate, regardless of the balance size.

- Attack the Top Debt: Dedicate all extra money, beyond the minimum required payments, to the debt with the absolute highest APR.

- Roll Over: Once the highest-interest debt is paid off, take the money you were paying on it (the minimum payment + the extra amount) and immediately add it to the minimum payment of the next highest-interest rate debt. The goal is to maximize the speed at which you tackle the debts that cost you the most money.

Example: Debt Avalanche Order

| Debt | Balance | APR | Priority |

|---|---|---|---|

| Credit Card 2 | $3,000 | 28.0% | #1 (Attack) |

| Personal Loan | $10,000 | 12.0% | #2 |

| Credit Card 1 | $500 | 10.0% | #3 |

| Student Loan | $25,000 | 6.0% | #4 |

In this scenario, you would aggressively attack Credit Card 2 (28.0% APR) first, even though Credit Card 1 has the smallest balance.

Who Should Use the Debt Avalanche?

- The Analytical Thinker: You are driven by numbers, spreadsheets, and optimization.

- The High-Debt Holder: You have significant high-interest debt (e.g., credit cards, payday loans) where the interest rate difference is substantial.

- The Patient Planner: You are confident you can stick to the plan for several months without needing immediate psychological reinforcement.

What is the Debt Snowball Method? (The Psychology Champion)

The Debt Snowball method is championed by financial personality experts like Dave Ramsey. It is the most psychologically effective way to eliminate debt, prioritizing motivation and consistency by focusing on the smallest balances first.

The Mechanism of the Debt Snowball

- List all your debts: Include the total balance and the minimum monthly payment. (The interest rate is ignored).

- Order by Balance Size: Arrange the list from the smallest total balance to the largest total balance.

- Attack the Smallest Debt: Dedicate all extra money to the debt with the smallest overall balance.

- Roll Over: Once the smallest debt is paid off, take the entire payment amount (minimum payment + extra amount) and add it to the minimum payment of the next smallest debt. This creates a literal snowball effect, increasing the payment amount as the debts get larger, building incredible momentum.

Example: Debt Snowball Order

| Debt | Balance | APR | Priority |

|---|---|---|---|

| Credit Card 1 | $500 | 10.0% | #1 (Attack) |

| Credit Card 2 | $3,000 | 28.0% | #2 |

| Personal Loan | $10,000 | 12.0% | #3 |

| Student Loan | $25,000 | 6.0% | #4 |

In this scenario, you would aggressively attack Credit Card 1 ($500 balance) first, even though its interest rate is relatively low. The fast win provides the confidence to move on to the next, larger debt.

Who Should Use the Debt Snowball?

- The Emotional Responder: You need quick wins to stay motivated and avoid feeling overwhelmed.

- The Starter: You have a long debt journey ahead of you (e.g., 5+ debts) and need an immediate boost of confidence.

- The Unpaid: You have many small debts that clutter your monthly budget and want the administrative ease of quickly clearing them off your plate.

Debt Snowball vs. Debt Avalanche: A Practical Comparison

| Feature | Debt Avalanche | Debt Snowball |

|---|---|---|

| Primary Focus | Saving the most money (Financial Efficiency) | Building psychological momentum (Emotional Consistency) |

| Ordering | Highest Interest Rate First | Smallest Balance First |

| Total Interest Paid | Lower (Always mathematically superior) | Higher (More interest accrues on large, high-rate debts) |

| Time to Debt-Free | Faster (By paying off the most expensive debt first) | Potentially Slower (If the smallest balance has a low rate) |

| Motivation Level | High initial commitment required. Delayed gratification. | High immediate motivation. Quick wins provide confidence. |

| Best For | Disciplined individuals with high-interest debt. | Those who need psychological wins to stick with the plan. |

The Verdict: Which Method is Better?

The answer to this question depends entirely on your personality. Financial independence is a game of consistency, and the best method is the one you will actually stick with.

1. If You Need Motivation (The Majority)

If you have tried and failed to tackle your debt before, or if the idea of seeing that $25,000 student loan as your first target feels paralyzing, the Debt Snowball is better.

- Why? The dopamine rush from paying off that first $500 debt is a powerful, reinforcing drug. That win proves to yourself that the system works. That motivation is what will carry you through the months when you are facing the larger, tougher debts.

2. If You Are Already Disciplined (The Exception)

If you are inherently disciplined, budget meticulously, and view debt primarily as an optimization problem, the Debt Avalanche is better.

- Why? If you have high-interest debt, the mathematical savings are too significant to ignore. Sticking to the Avalanche will genuinely save you hundreds or even thousands of dollars in interest and cut time off your journey.

A Note on Savings: The mathematical difference between the two methods is usually smaller than people think, unless you have credit card debt with an APR over 20% that is significantly larger than your smallest debts. For average debt portfolios (mortgage, car, student loans), the difference in total interest paid might be negligible, making the psychological consistency of the Snowball a more valuable asset.

Frequently Asked Questions (FAQ)

Does the Debt Snowball ignore interest rates completely?

Yes, the Debt Snowball methodology specifically excludes the interest rate from the ordering process. It is a purely psychological tool designed to maintain momentum by focusing solely on the balance size.

Why is the Debt Avalanche always mathematically superior?

Because compound interest works against you. By paying off the debt that is accumulating the most interest charges every single day, you immediately stop the most expensive bleeding. This reduces your principal balance faster, thus reducing the total interest you accrue over the life of the plan.

Can I switch between the two methods?

Yes, but it is rarely recommended as it can slow down your momentum. However, if you started the Avalanche but are struggling to stay motivated after six months, switching to the Snowball for one or two quick wins might be necessary to reset your focus.

Should I pay off my mortgage or high-interest credit card debt first?

Always, always, always prioritize the high-interest debt (usually credit cards or personal loans). The 25%+ APR on credit cards is significantly higher than the 6-8% rate on a mortgage. Do not allocate extra money to your mortgage principal until all other high-interest, non-secured debts are eliminated.