DIY Credit Repair: Fix Your Credit Score the Smart Way

If your credit score has taken a hit, you’re not alone. Millions of Americans are rebuilding their credit after facing financial setbacks, whether it’s late payments, high balances, or unexpected life events. The good news? You don’t need to pay thousands to a “credit repair company” to fix it. You can repair your credit yourself — the DIY way — and it can be just as effective (if not more).

In this complete guide, you’ll learn how DIY credit repair really works, what to avoid, and the exact steps to raise your score — confidently and legally.

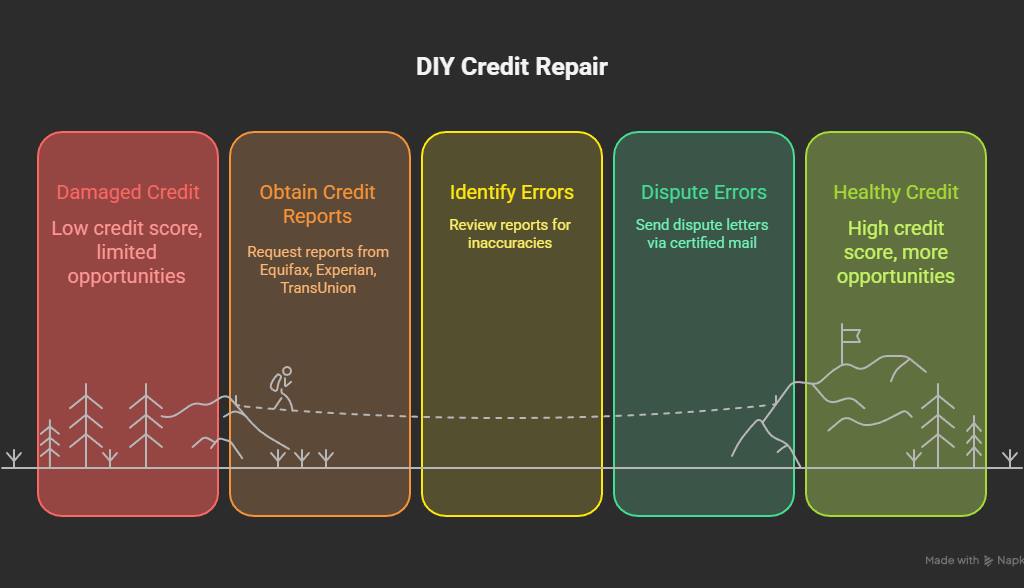

1. Understanding What DIY Credit Repair Really Means

DIY credit repair isn’t about “hacks” or loopholes. It’s about taking charge of your own credit information — reviewing, correcting, and rebuilding responsibly.

When you repair your credit yourself, you’re doing three key things:

- Reviewing your credit reports for errors.

- Disputing inaccurate or outdated information.

- Building positive new credit habits that raise your score over time.

It’s empowering, it’s free (except for your time), and it puts you in full control of your financial life.

2. Why Your Credit Score Matters More Than Ever

Your credit score impacts almost everything now — from getting approved for loans and renting an apartment to setting your car insurance rates.

A higher score can:

- Save you thousands in interest.

- Unlock better credit cards and mortgage rates.

- Even improve your chances when applying for jobs or housing.

So, when you take the DIY route, you’re not just repairing a number — you’re rebuilding financial trust.

3. Start by Getting Your Credit Reports

The first step in DIY credit repair is to know what’s on your report.

You’re entitled to one free credit report per year from each of the three major bureaus:

Go to AnnualCreditReport.com (the official site) and request all three reports. Reviewing all of them is essential — because some errors appear on one but not the others.

Once you have your reports, print or save them as PDFs. You’ll use these as your reference throughout the process.

4. Identify Errors That Are Hurting Your Credit

Now, go line by line through each report and look for inaccuracies or outdated entries. Common credit report errors include:

- Incorrect account balances

- Paid debts listed as unpaid

- Accounts that don’t belong to you

- Wrong late payment dates

- Duplicate entries

- Debts older than seven years still showing

Even a small mistake — like a missed payment date — can drop your score by dozens of points.

Mark each error clearly and make a list of what needs to be disputed.

5. How to Dispute Credit Report Errors

You have the right under the Fair Credit Reporting Act (FCRA) to dispute any information you believe is inaccurate or incomplete. Here’s how:

- Write a detailed dispute letter to each bureau (Equifax, Experian, TransUnion).

- Include:

- Your full name, address, and date of birth

- The specific account or item you’re disputing

- The reason for your dispute (e.g., “This account was paid in full in 2022”)

- Any supporting documents — such as payment receipts or settlement letters

- Send each letter by certified mail and keep copies of everything.

- Credit bureaus typically have 30 days to investigate and respond.

If the information is confirmed inaccurate, it must be corrected or deleted — permanently.

6. Don’t Dispute Online — Here’s Why

While it’s tempting to use online dispute forms, experts recommend sending physical letters.

Why?

Because online forms often include small-print waivers that limit your rights to take legal action later.

When you mail your dispute, you create a paper trail — proof that you exercised your rights properly.

7. Handle Collections Strategically

Collections can drag your score down fast — but there’s a smart way to handle them.

Here’s what to do:

- Validate the debt.

Request a debt validation letter from the collector. They must prove the debt belongs to you and that they’re legally allowed to collect it. - Don’t rush to pay immediately.

If the debt is near its seven-year expiration or invalid, paying may not help your score. - Negotiate in writing.

If you choose to settle, request a “pay-for-delete” agreement — meaning they remove the account from your report once you pay. Not all collectors agree, but it’s worth asking. - Get everything in writing before you send money.

8. Rebuild Positive Credit History

Repairing is only half the job — you also need to rebuild.

Here’s how to start boosting your score again:

- Pay on time — every time. Payment history makes up 35% of your score.

- Keep balances low. Aim to use less than 30% of your available credit limit.

- Avoid closing old accounts. They help maintain your credit age.

- Use secured credit cards or credit-builder loans. These tools report positive activity and can help lift your score faster.

Consistency is key. Even small, steady progress matters more than quick fixes.

9. Use Rent and Utility Reporting Services

Most people don’t realize they can build credit without debt.

Rent, utilities, and even streaming services can now be reported to credit bureaus through services like:

- Experian Boost

- AxcessRent’s Rent Reporting Program

- Self or Credit Strong

Adding these accounts to your report helps show consistent, positive payment history — especially if you’ve struggled with traditional credit lines.

10. Avoid Common DIY Credit Repair Mistakes

While repairing your own credit is straightforward, many people make costly mistakes that slow down progress. Avoid these:

- Disputing everything at once — focus only on real errors.

- Paying for deletion without a written agreement.

- Falling for credit repair scams.

- Not monitoring your score monthly.

Stick with verified information and document every step you take.

11. Monitor Your Progress

Once you start, keep track of changes in your score and report.

Use tools like:

- Axcessrent, Credit Karma or Credit Sesame for free tracking.

- Direct bureau accounts for updates.

- Regular checks every 30–60 days to confirm dispute results.

Improvement often takes a few months, but progress compounds with consistency.

12. How Long Does DIY Credit Repair Take?

There’s no instant fix — but typically:

- Minor errors: 30–60 days

- Collections or charge-offs: 3–6 months

- Full recovery after major issues: 6–12 months

The key is sticking to good habits once the cleanup is done. Over time, your efforts will compound into lasting credit health.

13. Should You Ever Hire a Credit Repair Company?

DIY works for most people. But if you’re overwhelmed or have dozens of disputes, hiring a reputable credit repair company might help.

However, beware of red flags:

- Companies that promise a “quick fix.”

- Asking for upfront payments (illegal under the Credit Repair Organizations Act).

- Guaranteeing score increases.

If you do hire one, make sure they’re transparent, FTC-compliant, and reputable.

14. How to Write a DIY Credit Dispute Letter (Sample)

Here’s a simple template you can use:

[Your Name]

[Your Address]

[City, State, ZIP Code]

[Date]

To: [Credit Bureau Name]

[Address]

Subject: Credit Report Dispute

Dear [Credit Bureau],

I’m writing to dispute inaccurate information on my credit report. The item below is incorrect:

- Account Name: [Insert account name]

- Account Number: [Insert account number]

- Reason for Dispute: [Explain briefly]

Please investigate and remove or correct this information per the Fair Credit Reporting Act (FCRA). I have attached supporting documentation for your review.

Sincerely,

[Your Name]

[Signature]

Keep it short, polite, and factual. Don’t include unnecessary details — just the evidence and reason for dispute.

15. Life After Credit Repair: Building Long-Term Financial Strength

Once your credit is back on track, protect it like gold.

- Set reminders for payments.

- Review your credit report annually.

- Avoid co-signing for others unless you’re sure.

- Build an emergency fund so you never fall behind again.

Credit repair isn’t just about cleaning up the past — it’s about creating a system that keeps your score strong for years to come.

Conclusion

DIY credit repair isn’t magic — it’s methodical. It’s about patience, persistence, and understanding your rights. You don’t need to be a financial expert to fix your credit; you just need a clear plan and consistency.

Every correction, every on-time payment, and every low balance adds up. In six months to a year, your score can transform — and so can your opportunities.

The best part? You did it yourself.

FAQ: DIY Credit Repair

1. Can I really repair my credit myself?

Yes. You have the same rights and access to your credit data as any paid company. With guidance and effort, you can do everything yourself legally and effectively.

2. How fast can I improve my score?

Results vary, but many see improvement within 30–90 days after disputing errors and paying down balances.

3. Will paying off debt raise my credit score?

Yes — especially revolving balances like credit cards. Reducing utilization under 30% helps quickly.

4. Can I remove collections myself?

Yes, by negotiating pay-for-delete or disputing inaccurate entries. Just ensure all agreements are written.

5. Should I close old accounts?

No. Keeping old accounts helps maintain credit history, which benefits your score.

6. Does checking my credit hurt my score?

No. Soft inquiries from checking your own credit don’t affect your score.

7. What laws protect me in this process?

The Fair Credit Reporting Act (FCRA) and Fair Debt Collection Practices Act (FDCPA) give you the right to dispute, correct, and protect your information.

8. Are DIY credit repair templates safe?

Yes — as long as they come from credible sources and you customize them with your real details.

9. Can rent payments help rebuild credit?

Absolutely. Using rent reporting services can add positive history to your report.

10. What’s the best mindset for credit repair?

Think long-term. Focus on steady habits, small wins, and consistent financial discipline — not instant results.