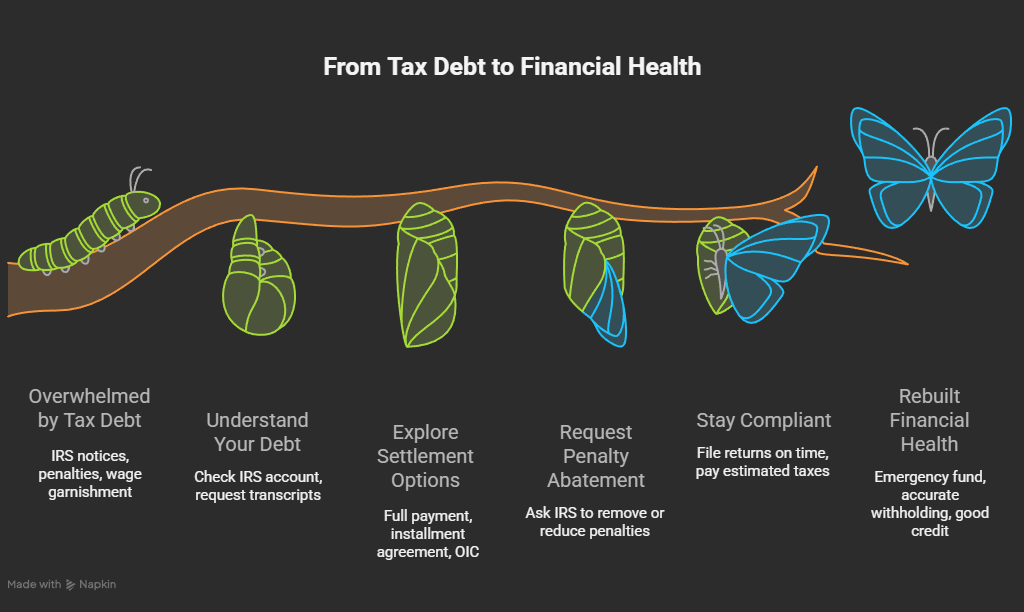

How to Settle Tax Debt with the IRS: A Complete Guide

Owing money to the IRS can feel overwhelming. The letters, the penalties, and the fear of wage garnishment can make anyone anxious. But here’s the truth — the IRS actually wants to work with you to resolve your tax debt. The key is knowing your options and acting fast before the situation grows worse.

Learn how to settle tax debt with the IRS legally and effectively. Explore payment plans, offers in compromise, penalty relief, and other proven ways to reduce or eliminate what you owe.

1. Understand What You Owe

Before you can settle your tax debt, you need to know exactly what you owe — including taxes, penalties, and interest.

Check Your IRS Account

You can create or log in to your account at IRS.gov to see:

- Your total balance

- Payment history

- Notices or penalties

- Tax years affected

If you can’t access it online, you can request a transcript by mail. This helps you confirm whether the balance is accurate and if any penalties were added by mistake.

2. Don’t Ignore IRS Notices

Ignoring IRS letters doesn’t make the debt go away — it only makes things worse. The IRS follows a clear process:

- Sends you a Notice and Demand for Payment.

- If unpaid, issues a Final Notice of Intent to Levy.

- Then, it may seize assets or garnish wages.

Responding early gives you access to flexible repayment options. Wait too long, and those options shrink fast.

3. Ways to Settle Your IRS Tax Debt

There’s no one-size-fits-all solution. The IRS offers several programs depending on your situation — whether you can pay in full, partially, or not at all.

Let’s break down your main options.

Option 1: Full Payment

If you can pay the balance in full, this is the fastest way to end the problem. Once paid, interest stops building, and the IRS releases any liens within 30 days.

You can pay online using:

- IRS Direct Pay (from your bank)

- Debit/credit card (a small fee applies)

- Check or money order

This method clears your record completely and restores your standing.

Option 2: Installment Agreement

If you can’t pay everything right away, you can request an Installment Agreement (IA) — essentially a monthly payment plan.

How It Works

- You apply online or by mail (Form 9465).

- The IRS reviews your income, expenses, and assets.

- They decide how much you can afford each month.

You’ll still pay interest, but as long as you stay current, the IRS won’t levy your assets.

Types of Installment Agreements

- Short-Term (up to 180 days) – No setup fee, ideal for smaller debts.

- Long-Term (over 180 days) – Setup fee applies, but automatic withdrawal reduces it.

If you owe less than $50,000 and have filed all returns, approval is almost automatic.

Option 3: Offer in Compromise (OIC)

An Offer in Compromise lets you settle your tax debt for less than you owe — legally.

When You Qualify

The IRS considers an OIC if:

- You can’t pay the full amount.

- Paying it would create financial hardship.

- The IRS doubts it can collect the full amount.

They evaluate your “reasonable collection potential” — your income, assets, expenses, and future earning ability.

Example

If you owe $50,000 but can only afford $12,000 based on your income and expenses, the IRS may accept that offer and forgive the rest.

However, OICs are strict. Only a small percentage of applications get approved, so documentation and honesty are crucial.

How to Apply

- File Form 656 (Offer in Compromise)

- Submit a financial statement (Form 433-A or 433-B)

- Pay a nonrefundable $205 application fee

- Make an initial payment (20% for lump-sum offers)

If approved, you must stay compliant with all future tax filings and payments for five years.

Option 4: Currently Not Collectible (CNC) Status

If you genuinely can’t pay right now — maybe you lost your job or live on a fixed income — the IRS may mark your account as Currently Not Collectible.

That means they’ll temporarily stop collecting, garnishing, or levying your assets. Interest continues to accrue, but you get breathing room.

You’ll need to show proof of hardship through income and expense documentation.

CNC status is reviewed periodically, so once your financial situation improves, collection may resume.

Option 5: Partial Payment Installment Agreement (PPIA)

If you can pay something but not the full balance, the IRS may approve a Partial Payment Installment Agreement.

You’ll make smaller monthly payments over time, and the IRS will forgive whatever remains after the collection statute expires (usually 10 years).

This program combines flexibility with long-term relief, though you must update your financials every two years.

4. Request Penalty Abatement

Sometimes, your tax debt grows because of penalties — not unpaid taxes. You can ask the IRS to remove or reduce those penalties if you have a valid reason.

Common Reasons for Penalty Relief

- Serious illness or family emergency

- Natural disaster

- Incorrect IRS advice

- First-time error with a good compliance record

If approved, it can cut your balance dramatically. You can call the IRS or use Form 843 to request it.

5. Understand the Statute of Limitations

The IRS can only collect taxes for 10 years from the date of assessment. Once that period ends, they can’t legally pursue the debt.

This doesn’t mean you can ignore the IRS for a decade, though. Filing bankruptcy, requesting an installment plan, or leaving the country pauses that clock.

Still, knowing the expiration date helps you plan your approach.

6. What to Avoid When Settling Tax Debt

Many people make costly mistakes when dealing with the IRS. Avoid these traps:

- Ignoring deadlines: Missing a filing or payment date can void agreements.

- Using shady “tax relief” companies: Many charge high fees and deliver little.

- Lying on financial forms: The IRS verifies your claims. Dishonesty can backfire.

- Paying with borrowed money: Don’t take on high-interest loans to pay taxes — it can worsen your debt.

Work directly with the IRS or a trusted tax professional instead.

7. Should You Hire a Professional?

You can handle most settlements yourself, but complex cases benefit from expert help.

Consider hiring a:

- Certified Public Accountant (CPA)

- Enrolled Agent (EA)

- Tax Attorney

These professionals know how to navigate IRS procedures and can negotiate on your behalf.

If you owe over $25,000, have multiple years of unfiled taxes, or face a lien or levy, professional help is often worth it.

8. Stay Compliant Going Forward

Settling your debt is just step one — staying current is step two.

To prevent future problems:

- File every tax return on time.

- Pay estimated taxes if self-employed.

- Keep updated W-4 forms with your employer.

- Avoid underreporting income or claiming false deductions.

The IRS tracks patterns. Staying compliant shows good faith and protects you from future penalties.

9. How to Rebuild After IRS Debt

Once your debt is resolved, it’s time to repair the damage and rebuild your financial health.

Rebuild Your Credit

IRS debt itself doesn’t appear on your credit report, but liens and late payments can. After resolving your balance:

- Request lien release documentation.

- Check your credit reports for accuracy.

- Dispute any incorrect negative marks.

Start Saving

Use the money you once sent to the IRS to build an emergency fund. Even small, regular deposits help prevent future tax trouble.

Adjust Withholding or Estimated Payments

Make sure the right amount of tax is withheld from your paycheck or quarterly payments. This prevents new balances from forming.

10. FAQs About How to Settle Tax Debt with the IRS

1. Will the IRS forgive my tax debt?

In some cases, yes. The IRS may forgive part of your debt through an Offer in Compromise if paying the full amount would cause financial hardship. You might also get relief if the 10-year collection period expires. However, forgiveness isn’t automatic — you must qualify based on your income, expenses, and ability to pay.

2. Can I negotiate with the IRS myself?

Absolutely. The IRS allows taxpayers to handle negotiations directly without hiring a company or lawyer. You can request a payment plan, offer in compromise, or penalty reduction by submitting the right forms. That said, if your case involves large sums or multiple years of unfiled returns, working with a CPA or enrolled agent can be helpful.

3. What happens if I do nothing?

Ignoring IRS debt is risky. The agency can garnish your wages, freeze bank accounts, seize property, or place a federal tax lien on your assets. Penalties and interest also keep growing. The earlier you respond, the more flexible the IRS will be with payment arrangements.

4. Does settling tax debt hurt my credit?

Not directly. The IRS doesn’t report tax debt to credit bureaus. However, if a federal tax lien was filed before payment, it may appear on your credit report and affect your score. Once your debt is paid or settled, you can request a lien withdrawal to help your credit recover faster.

5. What is an Offer in Compromise (OIC)?

An Offer in Compromise is a formal agreement that allows you to pay less than the total amount you owe. The IRS reviews your income, assets, and expenses to determine what they believe they can realistically collect. If approved, you pay the reduced amount in a lump sum or short-term plan, and the rest is forgiven.

6. How long does it take to settle tax debt with the IRS?

The timeline depends on your chosen method.

- Installment agreements can be approved within a few weeks.

- Offers in Compromise often take several months to review.

- Currently Not Collectible status can take a few weeks after financial verification.

Filing early and providing accurate documents can speed up the process.

7. What if I can’t afford to pay anything right now?

If you have little or no income, you can apply for Currently Not Collectible (CNC) status. This temporarily stops IRS collection efforts. You’ll need to show proof of hardship through income and expense documentation. Interest continues to accrue, but it prevents immediate enforcement.

8. Can the IRS take my home or car?

In extreme cases, yes — but only after multiple notices. The IRS prefers voluntary payment arrangements over seizures. If you communicate early and enter a payment plan or settlement, the IRS won’t seize personal assets like your home or vehicle.

9. How do I know which IRS payment option is best for me?

It depends on your financial situation.

- If you can afford the full balance, pay in full to stop interest.

- If you need time, request an Installment Agreement.

- If you can’t pay much, explore an Offer in Compromise or Partial Payment Plan.

A tax professional can help you choose the right program based on your ability to pay.

10. How can I avoid future tax debt?

Staying current is key.

- File all tax returns on time.

- Adjust your W-4 to withhold the correct amount.

- If self-employed, make quarterly estimated payments.

- Keep good financial records and consult a tax advisor annually.

Preventing new debt saves you from penalties, interest, and future stress.

Conclusion

Tax debt can feel like a mountain, but it’s one you can climb. The IRS provides several paths — payment plans, compromises, and hardship programs — to help you settle what you owe without losing control of your finances.

The most important step is to act early and stay honest. Once you take that first step, you can rebuild your financial stability, protect your income, and move forward without fear of another IRS letter arriving in your mailbox.