What Kind of Credit Inquiry Has No Effect on Credit Score?

Introduction

When it comes to your credit report and credit score, not all inquiries are created equal. Many people worry that every time someone checks their credit, their score drops. The truth is more reassuring: there are types of credit inquiries that do not affect your credit score. Understanding this distinction can empower you to use credit wisely and avoid unnecessary worry. In this article, you’ll learn what kind of credit inquiry has no effect on your credit score, why that is, how inquiries work, and how to manage them intelligently. We’ll also cover FAQs and provide a strong conclusion to help you walk away with actionable knowledge.

The key takeaway: A soft credit inquiry, such as checking your own credit, preapproved offers, or employer background checks, does not affect your credit score at all.

What is a Credit Inquiry?

A credit inquiry (also called a “pull” or “check”) is simply a request by a lender or other party to view your credit report. There are two broad categories:

- Hard inquiry (hard pull): Occurs when a lender checks your credit report because you are applying for new credit (e.g., a new credit card, loan).

- Soft inquiry (soft pull): Happens when you check your own credit, or when a company checks for pre-approval, account review, or promotional reasons.

Do soft inquiries affect credit?

- Soft credit inquiries have no effect on your credit score. They let companies or you look without a hit. No new debt involved. FICO and VantageScore skip them. Your score stays the same.

- Soft pulls happen when you check your own report. Or get a pre-approval. No application. Just a peek. They appear on your report. You see them. Lenders do too. But they don’t count for risk.

- This keeps things easy. Check your score weekly. No drop. Pre-qual for a card. See if you fit. No harm. It’s a safe way to stay informed.

- Hard pulls differ. They come from full applies. Score dips 5 points. Soft? Zero. Use soft ones often. Track habits. Spot errors.

- In 2025, soft pulls grow. More apps use them. Banks for offers. Renters for pre-screens. No stress.

- Soft inquiries give peace. Monitor without fear. Apply smart.

Why Soft Inquiries Don’t Hurt Your Score

Understanding why soft inquiries don’t impact your credit score helps to demystify the process:

- Credit scoring models (such as those from FICO) are designed to reflect risk of new credit being taken on. A soft inquiry usually means that the credit check is not tied to a new application.

- Soft inquiries are often for informational purposes or existing accounts (so the risk is lower). Because you are not requesting new credit or signaling an intent to borrow, the model treats these differently.

- They may still appear on your report (you can usually see them), but they are not visible to most lenders, and they don’t factor into score calculations.

Examples of Credit Inquiries That Have No Effect

Here are practical examples of soft inquiries (i.e., those that won’t impact your credit score):

- Checking your own credit report or using a free credit-score tool.

You initiate this. It’s a soft pull. No impact. - Pre-approved credit offers.

A lender or card issuer checks your report to see if you qualify for a promotion. You did not apply for credit, so it’s a soft inquiry. - Account review by a current creditor.

If a credit card issuer checks your credit to see if you qualify for a credit-limit increase or internal offer—it’s typically a soft inquiry. - Employment or background check (credit report access for non-credit decision).

Many employers or rental agencies check credit for employment/rental screening. These are soft pulls and do not affect your score.

These are the kinds of inquiries you can rest easy about—they will not lower your credit score.

does hard inquiry affect credit score ?

Though our focus is on the no-effect inquiries, it’s helpful to understand when inquiries do affect your score so you can avoid pitfalls.

- Hard inquiries (also known as “hard pulls”) occur when you apply for a new loan, credit card, mortgage, or auto-loan. During the application process, the lender asks for your credit report to assess risk.

- A hard inquiry can cause a small dip (often fewer than five points, depending on your situation).

- Multiple hard inquiries in a short period for different types of credit can signal higher risk and further impact your score.

- Some scoring models allow rate-shopping grace periods: multiple inquiries for the same type of loan (like auto or mortgage) within a short window (14–45 days) may count as a single inquiry.

Knowing the difference helps you avoid unnecessary “hard pulls” that might temporarily impact your credit rating.

How to Protect Your Credit While Managing Inquiries

Here are actionable tips for managing inquiries and protecting your credit score:

- Check your own credit regularly. Since you doing so is a soft inquiry, it won’t hurt your score—and it helps spot errors or unauthorized pulls.

- Ask lenders what type of inquiry they’re doing before you apply. If you’re uncertain whether a credit check is “hard” vs. “soft”, ask the institution.

- Do your rate-shopping within a short window if you’re looking for a large-loan (auto, mortgage) to avoid multiple hard pulls being counted «separately».

- Avoid applying for multiple different kinds of credit in a short period, especially if you already have less than stellar credit. Multiple hard inquiries can increase perceived risk.

- Review your credit report for unauthorized or unfamiliar inquiries. If you find an inquiry you didn’t authorize, you can dispute it.

How to Check Your Credit and Spot Problems

Keeping tabs on your credit inquiries is one of the smartest ways to protect your credit score. You can check your credit inquiries regularly using your free weekly reports from AnnualCreditReport.com.

Steps to Check Your Credit Inquiries

- Get your free report — Visit AnnualCreditReport.com and download your report from all three bureaus: Experian, TransUnion, and Equifax.

- Find the “Inquiries” section — Look for listings showing the dates, company names, and types of inquiries.

- Identify hard vs. soft inquiries —

- Hard inquiries: Usually show lender or creditor names (e.g., a credit card or loan application).

- Soft inquiries: Often show your own checks, employer reviews, or pre-approved offers.

- Watch for patterns — Too many recent hard inquiries may signal you’re applying for too much credit too fast.

- Dispute unauthorized pulls — If you find an inquiry you didn’t authorize, act immediately to dispute it and request deletion.

Steps to Dispute a Wrong Credit Inquiry

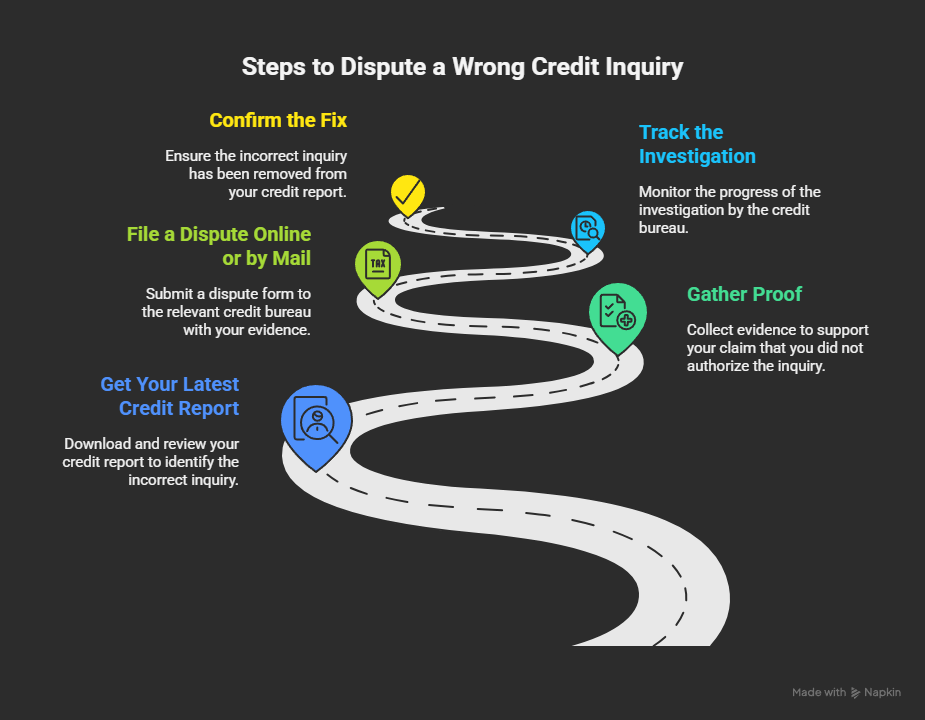

If you find a credit inquiry you don’t recognize, take immediate action. Here’s how to dispute it effectively:

1. Get Your Latest Credit Report

Download an updated report to confirm the incorrect inquiry. Highlight or mark the specific pull that looks wrong.

2. Gather Proof

If you never applied for credit with that company, collect evidence — emails, screenshots, or statements showing no application occurred.

3. File a Dispute Online or by Mail

Use the dispute form from the relevant credit bureau’s website:

- TransUnion: TransUnion Dispute Inquiries

- Equifax: Equifax Dispute Center

- Experian: Experian Dispute Form

Clearly explain the error, attach your proof, and submit the form.

4. Track the Investigation

The bureau has 30 days to investigate and verify the inquiry. You’ll receive updates via email or mail.

5. Confirm the Fix

If the lender cannot prove that you authorized the inquiry, the bureau will delete it from your report. Always confirm that the update appears in your next report.

Quick Recap:

- Report first (get a fresh copy)

- Gather proof (show you didn’t apply)

- Submit online or by mail

- Track progress within 30 days

- Confirm deletion once resolved

By monitoring your reports and disputing unauthorized inquiries quickly, you’ll protect your credit score from unnecessary damage and maintain your financial reputation.

Conclusion

In answering the key question — what kind of credit inquiry has no effect on your credit score? — the answer is clear: soft inquiries. Whether you’re checking your own credit, being pre-approved for a credit offer, or having an existing creditor review your account, these types of inquiries are benign to your credit score.

Understanding the difference between soft and hard inquiries helps you navigate the credit landscape with confidence. By being informed, you can monitor your credit responsibly, apply for new credit strategically, and avoid unnecessary score drops.

In short: don’t fear every single credit check—just be mindful of when it constitutes a hard pull. Use credit wisely, stay alert, and your credit score will reflect your long-term habits, not isolated missteps.

FAQs

Q1: If I apply for a credit card and it gets denied, does the inquiry still affect my score?

Yes — if the card issuer performed a hard inquiry (which is normal when you apply for new credit), then that inquiry counts even if you’re denied. The negative impact is still tied to the inquiry itself, not just approval.

Q2: Does checking my credit score on sites like Credit Karma or my bank hurt my credit?

No. These are usually soft inquiries. As long as you initiated them or they were for informational/pre-approval purposes and not a full credit application, there is no effect on your score.

Q3: I applied for a mortgage and within 30 days applied for an auto loan—will that look like two inquiries?

It depends—but many scoring models allow multiple inquiries for the same type of loan in a short window to be counted as one. But if you apply for different loan types (mortgage and auto) outside those windows, they may count separately and impact your score more.

Q4: Are there credit checks that never even show up on my report?

Some internal account reviews by lenders or promotional checks (soft inquiries) may not show in the section visible to lenders—they may only show you. But regardless of visibility, what matters is whether it was a soft versus hard inquiry, because soft ones don’t affect your score.

Q5: How long do credit inquiries stay on my report and affect my score?

Hard inquiries typically remain on your report for up to two years, but their impact on your score is usually limited to the first 12 months. Soft inquiries may remain listed but don’t affect scores and often aren’t visible to lenders.