How to report positive rent payment to credit bureau ?

Introduction

Rent takes a big chunk of most people’s income. Yet, it often does not help build credit. This changes with positive rent reporting. It lets on-time rent payments show up on credit reports. This helps renters create or boost their credit scores.

Many renters lack credit history. About 45 million Americans are credit invisible. They have no score because they have too few accounts. Rent reporting fixes this. It turns a monthly bill into a credit tool.

Landlords like it too. It cuts late payments and keeps tenants longer. Programs from Fannie Mae and Freddie Mac push this forward. They offer free services to property owners.

This guide explains positive rent reporting. We cover what it is. How it works. Benefits for everyone. And how to start. By the end, you will know if it fits your needs. Let’s break it down.

What Is Positive Rent Reporting?

Positive rent reporting sends records of on-time rent payments to credit bureaus. These include Equifax, Experian, and TransUnion. Only good payments count. Late or missed ones do not show up.

This differs from full-file reporting. That includes all payments, good and bad. Positive reporting protects renters. It avoids credit hits from one bad month.

The goal is simple. Help renters build credit. Rent is the top expense for many. Over 80% of renters want this feature. It makes sense.

A Short History of Positive Rent Reporting

Rent reporting started small. In the early 2010s, startups launched. They charged fees to report payments. Uptake was slow. Few landlords joined.

Things shifted in 2017. The Consumer Financial Protection Bureau pushed for it. They saw how it could help low-income families. Credit Builders Alliance ran pilots. Results showed big gains. Renters with no score got one fast.

By 2022, big players stepped in. Fannie Mae started a pilot. It partners with tech firms to report payments for free. Freddie Mac followed. They give loan perks to landlords who join. Now, in 2025, it’s mainstream. States like California require it for some housing. Over 100,000 units use it through Fannie Mae alone.

Why It Matters in Today’s Market

Housing costs rise. Credit scores decide who gets approved. Renters face barriers. Black and Hispanic households rent at twice the rate of white ones. Positive reporting levels the field.

It also helps during tough times. Post-pandemic, evictions spiked. Reporting cuts that risk. Tenants pay on time to keep building credit. Landlords collect more reliably.

How Does Positive Rent Reporting Work?

The process is straightforward. It links rent data to credit files. No extra work for most people. Tech handles it.

Step-by-Step Process

- First, a landlord signs up. They pick a provider like Axcessrent, Esusu or Jetty. The provider checks if the property qualifies. For Fannie Mae loans, it’s free for a year.

- Next, the system integrates. It pulls data from property software. This tracks payments automatically. No manual entry.

- Then, enrollment happens. Renters often join by default. They can opt out anytime. Providers send emails to explain.

- Each month, on-time payments go out. The provider formats the data. It sends to all three bureaus. Only full, timely payments count. If a renter misses, they pause reporting. No negative mark.

- Renters track progress. Apps show score changes. Some providers offer free credit monitoring.

- Finally, scores update. It takes 30-60 days to see effects. Consistent payments build history over time.

Benefits for Renters

For tenants, this is a game-changer. Rent becomes an asset, not just a bill.

Building Credit History from Scratch

Many young people or immigrants start with no credit. Rent reporting creates a file. In pilots, 100% of credit-invisible renters got scores. They hit near-prime levels quick.

Think of a new grad. They pay $1,500 rent monthly. After six months, they have a score. This opens credit cards or loans.

Improving Existing Credit Scores

Got a score but it’s low? Consistent rent helps. Subprime renters saw 32-point jumps on average. Why? Rent shows reliability.

One study found 40-point average gains in a year. It mixes with other habits. Pay bills on time. Keep debt low.

Long-Term Financial Wins

Better scores mean better deals. Lower rates on car loans. Easier apartment approvals. Even smaller security deposits.

Homeownership gets closer. Mortgages need good credit. Renters save on interest over life. One estimate: $50,000 saved on a home loan.

Plus, it fights inequality. Low-income renters gain most. 60% of under-$25K households rent. This builds wealth.

Benefits for Landlords and Property Managers

Owners see real returns. It’s not just feel-good.

Boosting On-Time Payments

Renters pay up to stay in the program. 73% say reporting motivates them. Delinquencies drop. One property cut lates by 20%.

Cash flow steadies. Less chasing payments. Staff saves time.

Cutting Turnover and Costs

Happy tenants stay. 58% pick properties with reporting. Turnover costs $2,500 per unit. Lower that, NOI rises.

Evictions fall too. Better credit means stable renters.

Gaining a Market Edge

In tight markets, amenities win. List “credit-building rent reporting.” It draws applicants.

Fannie Mae data: 427 properties enrolled by mid-2024. Over 101,000 units. More join in 2025.

Positive-Only vs. Full-File Rent Reporting

Know the difference. Positive-only reports good payments. It pauses on misses. Safe for renters.

- Full-file shows all. Late payments hurt scores. Some providers offer it. But positive wins for motivation.

- Pros of positive: No risk. Builds trust. Cons: Misses full history.

- Full-file pros: Complete view. Helps lenders. Cons: Can drop scores. Deters sign-ups.

- Most programs stick to positive. It fits the goal.

How to Get Started with Positive Rent Reporting

Ready to boost your credit through rent? Here’s how to get started.

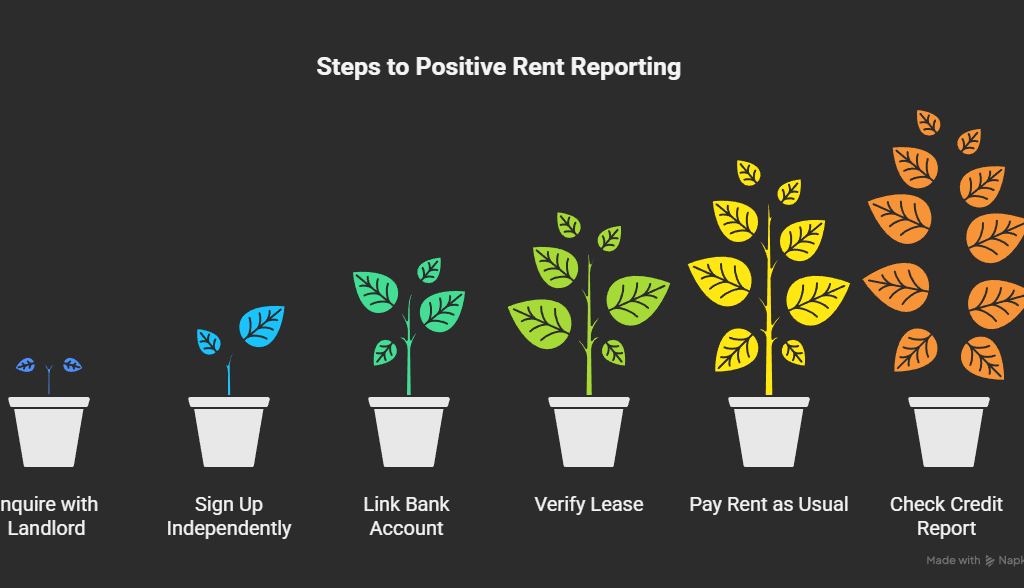

For renters: Start by asking your landlord, “Do you report rent to credit bureaus?” If the answer is yes, opt in immediately and confirm that the reporting is consistent. If not, sign up independently. Download a trusted rent-reporting app like Axcessrent, Boom, Piñata, or CreditMyRent, then link your bank account and verify your lease. Continue paying rent as usual—the service will automatically track your payments. Within 30 to 45 days, check your credit report to see the new tradeline reflecting your payment history.

For owners: Check eligibility first, especially if your property is financed under Fannie Mae. Choose a provider such as Axcessrent, Esusu, Jetty, or LevelCredit, then complete enrollment online and integrate it with your property management software. Notify tenants early, obtain their written consent, and ensure payment data is accurate each month. Start small with one building or a pilot program to test results. Many platforms offer a free year for new participants and take about a week to set up. Consistent monthly reporting strengthens both tenant credit and owner performance metrics over time.

Potential Drawbacks of Positive Rent Reporting

Positive rent reporting offers many benefits, but it’s not perfect—consider these possible drawbacks before enrolling.

Annual or monthly fees can add up, sometimes costing $50–$100 per year, which might strain tight budgets. Additionally, not every reporting service sends data to all three credit bureaus, meaning results can differ between Experian, Equifax, and TransUnion. Landlord cooperation may also be required, and some older property managers may hesitate to adopt new systems.

Back-reporting past rent payments often comes with an additional fee, so consider skipping it unless you’ve been consistently on time. Credit improvement also takes patience—scores typically rise over several months, not weeks. Privacy is another factor; linking a bank account means sharing limited financial data. Finally, full-file reporting can work both ways—one missed payment might hurt your score.

In 2025, rent-reporting scams are rising, so always verify the legitimacy of any service before connecting financial information. Despite the risks, the long-term gains usually outweigh the drawbacks for most renters.

2025 Updates on Positive Rent Reporting

Positive rent reporting is evolving fast in 2025, bringing new opportunities and wider access.

The Fannie Mae pilot program is scheduled to end in June 2025, but it’s expanding to include more participating lenders and multifamily owners. Several states—led by California—now mandate or encourage rent reporting, and others like New York and Illinois are expected to follow. Major credit bureaus are integrating rent data more fully, with VantageScore placing increased emphasis on consistent rent history.

Free and low-cost options are growing, especially for residents in HUD-assisted housing, as the agency promotes rent reporting as a financial inclusion tool. Meanwhile, Freddie Mac is rewarding property owners who adopt rent reporting by offering favorable loan terms. Apps are improving too—many now use AI-powered tracking to detect payments more accurately.

Stay informed by checking updates directly on the Fannie Mae website or your reporting provider’s news section. The landscape is changing fast, and early adopters stand to benefit most.

Conclusion

Positive rent reporting is transforming rent payments into a powerful credit-building tool. When tenants pay on time, it helps improve scores and builds financial stability. For landlords, it reduces late payments and strengthens tenant retention. The process is simple, costs are low, and the rewards can be significant.

If you’re a renter, ask your landlord about rent reporting or sign up with a trusted app like Axcessrent today. Watch your credit score rise month by month. For landlords, enrolling your property not only helps tenants but also improves collection rates and occupancy.

It’s truly a win-win solution. Take action in 2025—better credit and stronger communities start with one reported rent payment at a time.

Frequently Asked Questions (FAQs)

What is positive rent reporting?

It’s a system that reports your on-time rent payments to credit bureaus, helping you build credit history without taking on debt.

How does positive rent reporting affect my score?

On-time payment history can raise your score by 20 to 60 points over time, depending on your existing credit profile.

Is positive rent reporting free?

Some programs are free, especially those through landlords or pilot initiatives. Others cost between $3 to $10 per month.

Can landlords charge for rent reporting?

In certain states, landlords cannot pass on rent-reporting fees. California, for example, has limits. Always check local regulations.

Does it report late payments?

No. Positive-only services report on-time payments, not missed ones—making it a safe and effective credit-building option.