5 Ways Rent Reporting Boosts Credit for Low Income Renters and Immigrants

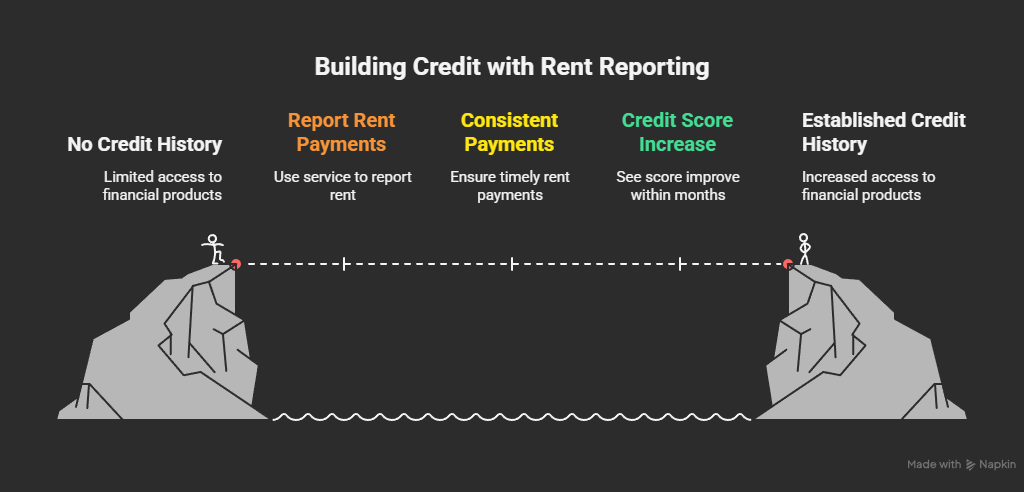

Rent reporting boosts credit for low income renters and immigrants, making it a vital tool for achieving financial stability in the United States. Traditional credit-building options like credit cards or loans often demand an existing credit history, which many low-income individuals and newcomers lack. By transforming monthly rent payments into a credit-building opportunity, rent reporting offers a low-risk, accessible solution. In 2025, with rent prices soaring (national average for a one-bedroom: $1,730, per Apartment List’s National Rent Report) and economic pressures mounting, rent reporting empowers underserved groups to improve their credit scores and unlock better loans, rentals, and financial opportunities.

This guide explores how rent reporting works, why it’s essential for low-income renters and immigrants, and five practical ways to leverage it for credit building.

Why Rent Reporting Matters for Low Income Renters and Immigrants

For low-income renters and immigrants, establishing credit is tough. Many are “credit invisible” (no U.S. credit history) or have thin credit files, affecting 80 million Americans, per PYMNTS research. Without a credit score, securing loans, renting apartments, or even getting utility services becomes challenging. Rent reporting changes this by allowing on-time rent payments to be reported to major credit bureaus—Experian, Equifax, and TransUnion—building a positive payment history, which accounts for 35% of your FICO score.

For low-income renters, who often spend 40–60% of their income on rent (well above the recommended 30%), consistent payments demonstrate financial responsibility. Immigrants, especially those new to the U.S., face similar hurdles, as foreign credit histories typically don’t transfer. Rent reporting, supported by tools like AxcessRent and new legislation like the Credit Access and Inclusion Act (April 2025), empowers these groups to build credit without taking on debt, making it a game-changer for financial inclusion.

This guide answers key questions:

- How does rent reporting help low-income renters build credit?

- What are the best ways for immigrants to use rent reporting?

- What risks should you watch out for?

Let’s explore five effective ways rent reporting can boost your credit score, tailored for low-income renters and immigrants.

5 Ways Rent Reporting Boosts Credit for Low Income Renters and Immigrants

1. Establishes a Credit History Without Debt

Rent reporting allows you to create a credit profile without relying on credit cards or loans, which can be risky for low-income individuals or immigrants with limited financial resources. By reporting your rent payments to credit bureaus, you add positive payment history to your credit file, a key factor in building a score.

- How It Works: Services like AxcessRent or RentReporters submit your rent payments (e.g., $1,200/month) to bureaus, showing consistent financial behavior.

- Impact: A 2019 HUD study found that 49% of renters with no credit score became scorable after rent reporting, with scores often reaching 620+ (qualifying for most loans).

- Example: A low-income renter paying $800/month for a year can establish a credit score of 600–650, opening doors to better rental applications.

Tip: Choose a service that reports to all three bureaus for maximum impact. Confirm with your landlord that they’ll allow rent reporting.

2. Boosts Credit Scores Quickly

Rent reporting can raise your credit score in as little as one month. For those with thin files, adding rent payments can increase scores by 20–50 points, per TransUnion data. This is especially valuable for immigrants who start with no U.S. credit history.

- How It Works: Consistent rent payments (e.g., $1,500/month) reported via platforms like AxcessRent improve your payment history and credit file depth.

- Impact: A CBA pilot showed 100% of unscorable renters became scorable, with an average score increase of 23 points after rent reporting.

- Example: An immigrant paying $1,000/month rent for six months could move from no score to 620, qualifying for a secured credit card.

Mistake to Avoid: Missing rent payments, as late payments reported to bureaus can lower your score by 50+ points.

3. Enhances Financial Inclusion

Low-income renters and immigrants often face barriers to credit access due to systemic issues like limited banking access or no Social Security Number (SSN). Rent reporting levels the playing field by using payments you’re already making to build credit.

- How It Works: Tools like Experian Boost or AxcessRent allow you to report rent without needing an SSN (some accept ITINs). This is crucial for immigrants and low-income households, 5.6 million of whom are unbanked, per the World Economic Forum.

- Impact: The Credit Access and Inclusion Act (2025) mandates bureaus to include rent payments, potentially helping 40 million “credit invisible” Americans.

- Example: A low-income renter without a bank account uses AxcessRent to report $900/month rent, gaining a credit score for loan eligibility.

Tip: Check if your reporting service accepts ITINs or other IDs if you lack an SSN.

4. Improves Loan and Rental Approvals

A stronger credit score from rent reporting increases your chances of getting approved for loans, credit cards, or rentals. Landlords often require a credit score of 580–650, and lenders look for 670+ for favorable terms. Rent reporting helps you meet these thresholds.

- How It Works: Regular rent payments reported to bureaus build a robust credit file, impressing landlords and lenders.

- Impact: A TransUnion study showed 80% of subprime renters saw score increases after one month of rent reporting, with 41% gaining 10+ points.

- Example: An immigrant with a 550 score reports $1,200/month rent for six months, raising their score to 650, securing a car loan at a 5% lower rate.

Mistake to Avoid: Not verifying that your landlord or property manager participates in rent reporting programs.

5. Offers a Low-Risk Credit-Building Option

Unlike credit cards or loans, which carry debt risks, rent reporting uses payments you’re already making, making it ideal for low-income renters and immigrants wary of financial strain.

- How It Works: Services like AxcessRent report only on-time payments, minimizing risk. You don’t need to borrow money or pay interest.

- Impact: CBA’s Rent Reporting Pilot found 100% of participants saw rent reporting as a safe way to build credit without debt.

- Example: A low-income renter paying $700/month avoids high-interest credit cards by using rent reporting to achieve a 600+ score.

Tip: Compare reporting services for fees (e.g., $5–$10/month) to ensure affordability.

How to Start Rent Reporting in 2025

Here’s a step-by-step guide to using rent reporting to build credit, tailored for low-income renters and immigrants:

- Choose a Reporting Service:

- Sign up for AxcessRent, RentReporters, or Experian Boost (rent-specific features). Costs range from free to $10/month.

- Ensure the service reports to all three bureaus for maximum impact.

- Example: An immigrant uses AxcessRent to report $1,000/month rent to TransUnion and Equifax.

- Confirm Landlord Participation:

- Ask your landlord or property manager if they allow rent reporting or partner with services like AxcessRent.

- Some services let you report directly, even without landlord involvement.

- Mistake to Avoid: Assuming all landlords participate—verify first.

- Pay Rent on Time:

- Set up auto-pay or calendar reminders to avoid late payments, which can hurt your score if reported.

- Use budgeting apps like Mint to track rent and other bills.

- Example: Paying $800/month rent consistently for three months adds positive history to your credit file.

- Verify Reporting:

- Check your credit report at AnnualCreditReport.com to confirm rent payments appear correctly.

- Dispute errors with the service or bureau if payments are missing.

- Example: After two months, confirm $1,200/month rent is on your Experian report.

- Monitor Your Credit Score:

- Use free tools like Credit Karma or Experian to track score changes.

- Aim for a score of 670+ for better loan and rental options.

- Example: A low-income renter sees their score rise from 580 to 650 after six months of reported rent.

Benefits of Rent Reporting for Credit Building

- Improves Credit Scores: Adds positive payment history, boosting scores by 20–50 points in months.

- Increases Approval Odds: Helps secure loans, credit cards, or rentals in competitive markets.

- Lowers Interest Rates: Higher scores save thousands on loans (e.g., 5% lower rates on a $20,000 car loan).

- Promotes Financial Inclusion: Empowers credit-invisible groups like immigrants and low-income renters.

- Supports Long-Term Goals: Builds a foundation for major purchases like homes or cars.

For example, a low-income immigrant reporting $1,000/month rent for a year could raise their score from unscorable to 620, qualifying for a secured credit card or better apartment lease.

Challenges and Risks to Watch For

While rent reporting is powerful, consider these challenges:

- Limited Bureau Acceptance: Not all bureaus or lenders accept rent data yet, though adoption is growing in 2025.

- Late Payment Risks: Missed payments reported to bureaus can lower your score by 50+ points.

- Service Fees: Some platforms charge $5–$10/month, which may strain low-income budgets.

- Privacy Concerns: Ensure services comply with regulations like CCPA to protect your data.

- Landlord Cooperation: Some landlords may not participate or may charge for verification.

Mistake to Avoid: Signing up for a service that only reports to one bureau, limiting your credit-building impact.

Tools and Resources for Rent Reporting

- AxcessRent: Reports rent to all three bureaus, ideal for low-income renters and immigrants.

- Experian Boost: Free tool to report rent and utility payments (limited to Experian).

- RentReporters: Reports rent and up to 24 months of past payments for a fee.

- Credit Karma: Free credit score monitoring to track progress.

- AnnualCreditReport.com: Free credit reports to verify reported payments.

- National Low Income Housing Coalition: Resources for affordable housing and tenant rights.

Conclusion

In 2025, rent reporting is a lifeline for low-income renters and immigrants looking to build credit without debt. By turning your rent payments into a credit-building tool, services like AxcessRent help you establish a credit history, boost your score, and unlock better financial opportunities. Whether you’re aiming for a loan, a new apartment, or lower interest rates, rent reporting offers a low-risk, accessible solution. Start by enrolling in a reporting service, paying rent on time, and monitoring your credit at AnnualCreditReport.com. Visit AxcessRent for more tips and tools to take control of your financial future today.

FAQs for Low Income Renters and Immigrants

How Does Rent Reporting Help Low-Income Renters Build Credit?

Rent reporting submits your on-time rent payments to credit bureaus, adding positive payment history to your credit file. This can raise your score by 20–50 points, helping low-income renters qualify for loans or rentals without taking on debt.

What Are the Best Ways for Immigrants to Build Credit with Rent Reporting?

Immigrants can:

- Use services like AxcessRent to report rent payments, even without an SSN (ITINs often accepted).

- Pay rent on time to build a positive payment history.

- Verify reporting with AnnualCreditReport.com.

- Monitor score changes with Credit Karma.

- Combine with utility reporting via Experian Boost for faster results.

What Is Rent Reporting and How Does It Work?

Rent reporting is the process of submitting your rent payments to credit bureaus to build your credit history. Services like AxcessRent or RentReporters verify payments with your landlord and report them, improving your score over time.

Can Rent Reporting Really Improve My Credit Score?

Yes, consistent rent payments reported to bureaus can boost your score by 20–50 points in months, per TransUnion data. A HUD study showed 49% of unscorable renters became scorable after rent reporting.

Are There Risks to Rent Reporting?

Risks include late payments lowering your score, service fees ($5–$10/month), and limited bureau acceptance. Verify that your service reports to all three bureaus and ensure landlord participation.

What Documents Do Immigrants Need for Rent Reporting?

You’ll need:

- Proof of rent payments (bank statements, lease agreement).

- Government ID (passport, ITIN, or SSN if available).

- Landlord verification (some services handle this).

- A reporting service account (e.g., AxcessRent).