From Renting to Owning: 10 Secrets steps to Knowing You’re Ready

For many people, renting is the default starting point when it comes to finding a place to live — and for good reason. It offers flexibility, fewer long-term obligations, and allows you to sidestep many of the ongoing responsibilities that come with owning a home, like maintenance, property taxes, and homeowner’s insurance. Renting can be especially ideal in the early stages of adulthood or during transitional periods when mobility and low commitment are priorities.

But as time goes on, circumstances change. Maybe your income has stabilized, your career is on track, or you’re starting to crave more permanence and control over your living space. That’s often when the idea of renting to owning starts to take shape — transforming from a vague aspiration into a serious consideration. At some point, the thought of owning a home begins to feel less like a far-off dream and more like a logical, empowering next step in your life journey.

So, how do you know when you’re truly ready to transition from renting to owning? While the timing isn’t the same for everyone, there are clear signs that can help guide your decision. It’s not just about having enough money in the bank or checking off a list of financial tasks. It’s about feeling mentally, emotionally, and financially prepared to take on one of the most meaningful investments of your life.

Let’s dive into 10 major indicators that suggest you’re ready to leave renting behind and step confidently into homeownership — and why each one plays a bigger role than you might expect.

10 Steps to Go from Renting to Owning Like a Pro

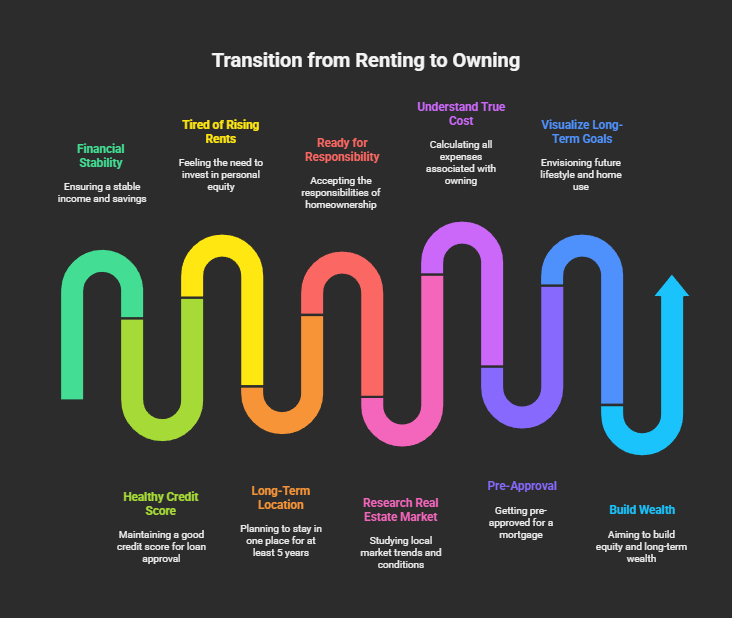

1. You’re Financially Stable — And Not Just Barely

Being able to make your rent every month doesn’t automatically mean you’re ready for a mortgage. Homeownership comes with upfront costs like a down payment, closing fees, and ongoing expenses like property taxes, insurance, repairs, and maintenance.

If you’ve been consistently saving, have a stable income, and can build or maintain an emergency fund (ideally 3–6 months of living expenses), you’re already in a strong financial position.

Pro Tip: Lenders often look at your debt-to-income (DTI) ratio, so keeping your credit card balances and other debts low will help you qualify for better mortgage rates.

2. You Have a Healthy Credit Score

Your credit score can make or break your ability to get approved for a mortgage. A higher score generally means better loan options and lower interest rates, which can save you thousands over the life of your loan.

If your score is in the mid-600s or higher, you’re probably in decent shape. But if you’re in the 700s or above, you may be eligible for the best rates available.

Credit Building Tip: Use rent reporting services like AxcessRent to get credit for on-time rent payments — one of the easiest ways to raise your score while still renting.

3. You’re Tired of Rising Rents and Ready to Invest in Yourself

Let’s be honest — rent prices rarely go down. If your lease renewals feel like a game of roulette, and you’re tired of building your landlord’s equity instead of your own, it may be time to switch gears.

Owning a home allows you to build long-term wealth and stability through home equity. Instead of handing over rent each month, your mortgage payments start building ownership in something that’s actually yours.

4. You Know Where You Want to Be for the Long Haul

Buying a home makes more sense when you plan to stay in one place for a while — ideally at least 5 years. If you’re settled into your city, love your community, or plan to raise a family where you are, owning could offer a deeper sense of stability and connection.

However, if your career might take you elsewhere or you just haven’t found “your spot” yet, it might be worth renting a bit longer.

5. You’re Ready for Responsibility — and Freedom

Being a homeowner means there’s no landlord to call when something breaks. You’ll be the one fixing leaks, maintaining the yard, and paying for unexpected repairs. That can sound overwhelming — but it also means total control.

Paint the walls any color. Upgrade the kitchen. Adopt that big dog. Homeownership gives you the freedom to shape your space however you want.

6. You’ve Researched the Real Estate Market

Timing is everything in real estate. If home prices in your area are stabilizing or interest rates are reasonable, it might be a smart time to buy.

Take time to study trends in your local market — what neighborhoods are growing, how home values are shifting, and whether properties are selling fast or sitting on the market. Knowledge gives you power when negotiating or choosing the right moment to buy.

7. You Understand the True Cost of Homeownership

Owning isn’t just about the mortgage. There are property taxes, homeowners insurance, HOA fees (if applicable), and ongoing upkeep to consider. Not to mention possible repairs or renovations.

Create a “mock budget” based on potential homeownership expenses. If that number feels manageable and still leaves room for savings, you may be more ready than you think.

8. You’ve Been Pre-Approved or Know What You Can Afford

Getting pre-approved for a mortgage doesn’t lock you in — but it gives you a realistic understanding of what you can afford. You’ll also know what kind of loan terms you qualify for, how much you’ll need for a down payment, and what your monthly payments might look like.

This step alone gives you confidence when browsing homes or speaking with agents.

Bonus: Programs like FHA loans or first-time homebuyer assistance can reduce upfront costs and make ownership more accessible than ever.

9. You’ve Started Visualizing Your Long-Term Goals

Homeownership isn’t just about bricks and walls — it’s about your lifestyle. Do you dream of a backyard for your kids or pets? A home office for your business? A garage for your weekend projects?

If you’ve been imagining your “someday home,” there’s a good chance that you’re ready to turn those dreams into plans.

10. You Want to Build Wealth — Not Just Pay for Shelter

One of the biggest benefits of owning a home is equity — the difference between what your home is worth and what you owe on it. Over time, equity grows as your mortgage balance goes down and (ideally) your home’s value goes up.

That equity can be used for other financial goals: funding a business, investing, paying for college, or upgrading to your next home.

Renting may be simpler in the short term, but ownership can offer long-term financial growth — and that’s a powerful reason to make the move.

Final Thoughts: Owning Is a Journey, Not a Race

Making the move from renting to owning is one of the most significant financial and emotional decisions you’ll make — and it’s not just about the numbers. It’s about your mindset, your readiness to take on responsibility, and your motivation to build something long-term. Homeownership isn’t a finish line; it’s a journey that begins when your lifestyle, stability, and financial foundation align. And remember, just because others around you are buying homes doesn’t mean you’re behind. Your path is your own, and it’s okay to take the time to prepare, learn, and grow into this new chapter.

When you’re ready to make that leap, the key is preparation — and that’s exactly where tools like AxcessRent can help. By reporting your rental payments and building credit history with the money you’re already spending on rent, AxcessRent gives renters a powerful head start toward homeownership. It’s a smart, low-risk way to prove creditworthiness and open doors to better loan options and lower interest rates. So even if buying isn’t on your calendar just yet, taking steps now with AxcessRent can set you up for a smoother, more confident transition when the time is right.