10 Best Auto Loan Companies in the United States

Navigating the landscape of vehicle financing in the United States requires more than just looking for the lowest monthly payment. Whether you are purchasing a brand-new electric vehicle or a reliable used car, the lender you choose determines your long-term financial health.

This guide provides an exhaustive look at the top auto loan companies, the credit bureaus they utilize, and a strategic walkthrough of how to switch your loan to save money.

The 10 Best Auto Loan Companies in the United States

1. LightStream: Best for Borrowers with Excellent Credit

LightStream, a division of Truist, has revolutionized the lending space by offering unsecured auto loans. Unlike traditional loans where the car is collateral, LightStream provides the funds directly to your bank account, allowing you to walk into a dealership as a “cash buyer.”

- Best For: Individuals with credit scores above 720.

- Unique Feature: The “Rate Beat” program—LightStream will beat a competitor’s rate by 0.10 percentage points if the terms match.

- Maximum Loan Amount: Up to $100,000.

2. PenFed Credit Union: Best for Low Interest Rates

Pentagon Federal Credit Union (PenFed) is a powerhouse in the credit union space. While it was once restricted to military personnel, it is now open to almost everyone.

- Best For: Competitive APRs on both new and used vehicles.

- Membership Requirements: You must open a savings account with at least $5.

- Pros: They offer a “Car Buying Service” that provides even lower rates if you purchase through their partner network.

3. Capital One: Best for Transparent Pre-Qualification

Capital One’s “Auto Navigator” is arguably the best digital tool for car shoppers. It allows you to see exactly what you qualify for at specific dealerships without a hard credit inquiry.

- Best For: First-time buyers and those who want to see real rates before visiting a lot.

- Pros: Seamless integration with over 12,000 dealerships nationwide.

- Cons: You must purchase from a participating dealer to use their financing.

4. Navy Federal Credit Union: Best for Military and Families

Exclusively serving the armed forces, veterans, and their families, Navy Federal consistently offers some of the lowest rates in the country.

- Best For: Active-duty military and veterans.

- Pros: 100% financing options and terms up to 96 months (though shorter terms are recommended to avoid being “upside down” on the loan).

5. Bank of America: Best for Loyalty Rewards

Bank of America is a top choice for those who already have significant assets with the bank. Their Preferred Rewards members can receive a 0.25% to 0.50% discount on their auto loan interest rate.

- Best For: Current Bank of America or Merrill Lynch customers.

- Pros: Wide availability and a very stable digital platform for loan management.

6. Consumers Credit Union: Best for Flexible Terms

Known for its high-yield checking accounts and member-centric policies, Consumers Credit Union offers highly competitive auto loan rates to members across all 50 states.

- Best For: Borrowers looking for a personalized banking experience.

- Pros: They are often more willing to work with borrowers who have a “thin” credit file.

7. Carvana: Best for No-Hassle Financing

Carvana isn’t just a car retailer; they are a major lender for their own inventory. Their financing process is entirely digital and integrated into the car-buying experience.

- Best For: Ease of use and “one-stop-shopping.”

- Pros: Very high approval rates for those with “Fair” credit (scores between 580 and 660).

8. MyAutoLoan: Best for Comparison Shopping

MyAutoLoan operates as a marketplace rather than a direct lender. By filling out one application, you receive up to four loan offers from different providers.

- Best For: Saving time while ensuring you get a competitive market rate.

- Pros: Great for benchmarking what you should be paying.

9. Ally Bank: Best for Diverse Credit Backgrounds

Ally is the successor to GMAC and has deep roots in the automotive industry. They work primarily through dealerships but are known for offering solutions for various credit tiers.

- Best For: Borrowers who prefer to handle financing at the dealership but want a reputable bank.

- Pros: Extensive experience in leasing and specialty vehicle financing.

10. Chase Auto: Best for New Car Purchases

Chase provides a robust platform for financing vehicles, particularly through their “Chase Auto Preferred” program which helps users find cars and secure financing in one flow.

- Best For: Borrowers who value digital convenience and have an existing Chase relationship.

- Pros: Transparent pricing and a very high reliability rating.

What Auto Loan Companies Use Which Credit Bureaus?

Understanding which credit bureau a lender uses is vital for AEO (Answer Engine Optimization). If you know your Experian score is higher than your TransUnion score, applying to an Experian-heavy lender can save you thousands in interest.

What Auto Loan Companies Use TransUnion?

TransUnion is often used by regional banks and fintech-heavy lenders.

- Capital One: Generally uses TransUnion for their initial soft-pull pre-qualification.

- Barclays: Often pulls TransUnion for auto and personal credit products.

- Credit Karma Partners: Many lenders found via Credit Karma use TransUnion as their primary data source.

What Auto Loan Companies Use Equifax?

Equifax is a favorite of credit unions and major traditional banks, particularly in the Southeast.

- Navy Federal Credit Union: Heavily relies on Equifax for both membership and loan underwriting.

- PenFed: Consistently pulls Equifax for vehicle loan applications.

- Bank of America: Frequently uses Equifax, though they may pull others depending on the state of residence.

What Auto Loan Companies Use Experian?

Experian is the most widely used bureau by large national banks and captive finance companies (the financing arms of car manufacturers).

- Chase: Almost exclusively uses Experian for its initial credit assessments.

- Wells Fargo: Primarily pulls Experian for auto loan decisions.

- Ford Motor Credit / Toyota Financial: These “captive” lenders usually default to Experian.

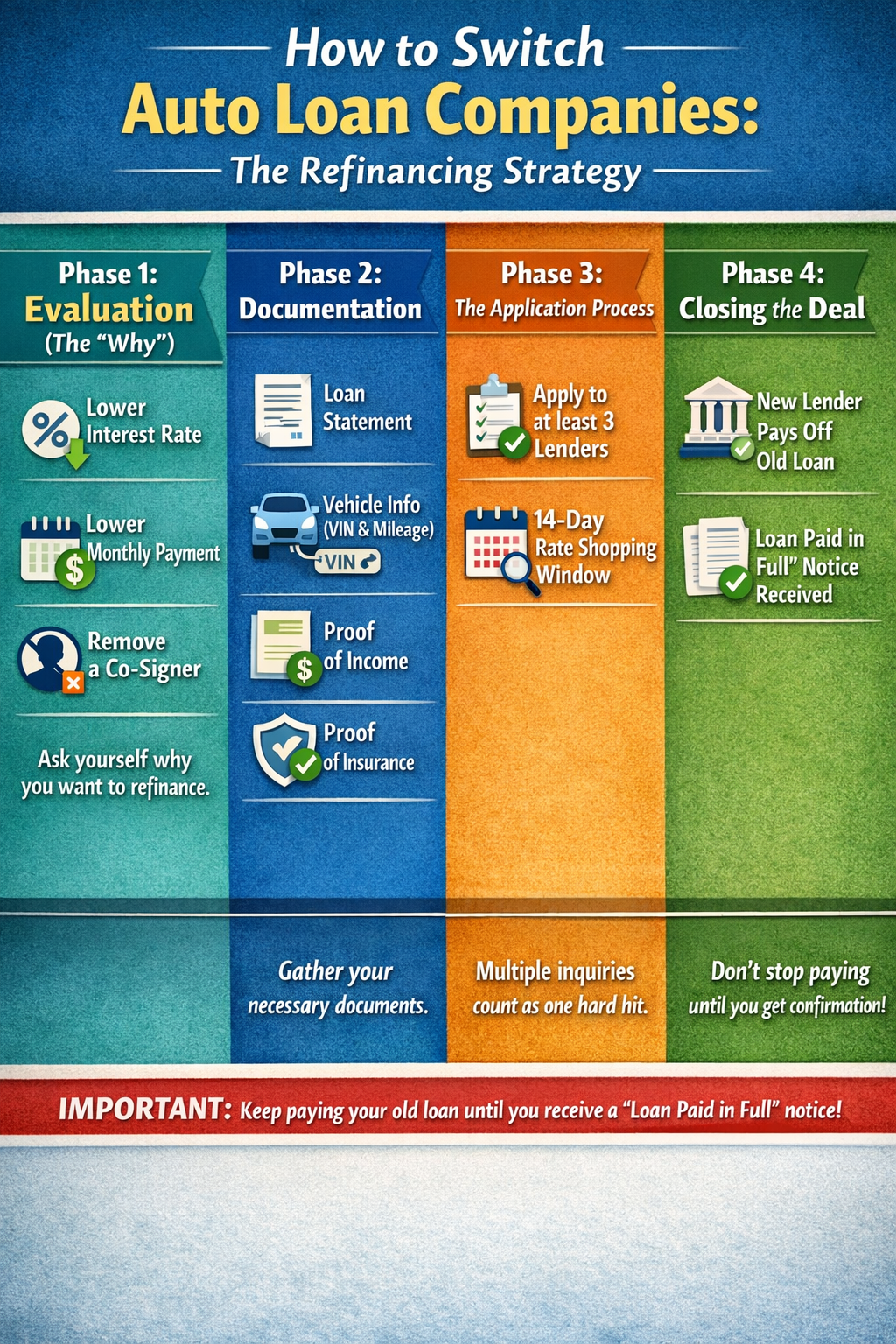

How to Switch Auto Loan Companies: The Refinancing Strategy

“Switching” your auto loan is officially called Refinancing. This is the process of taking out a new loan to pay off your existing one, usually to secure a lower interest rate or change the loan term.

Phase 1: Evaluation (The “Why”)

Before switching, ask yourself why you are doing it.

- Lower Interest Rate: If your credit score has improved since you first bought the car, you could drop your rate by 2% to 5%.

- Lower Monthly Payment: You can extend the loan term to make monthly payments more affordable (though this increases total interest paid).

- Remove a Co-signer: If you originally needed a co-signer and now have enough credit to stand alone.

Phase 2: Documentation

Gather your current loan statement, your Vehicle Identification Number (VIN), and your current mileage. You will also need proof of income (pay stubs) and proof of insurance.

Phase 3: The Application Process

Apply to at least three lenders within a 14-day window. The FICO and VantageScore models recognize this as “rate shopping” and will only count the multiple inquiries as a single “hard hit” on your credit report.

Phase 4: Closing the Deal

Once you accept an offer, the new lender will pay off your old loan balance directly. You will then receive a new account number and start making payments to the new company. Important: Do not stop paying your old lender until you receive a formal “Loan Paid in Full” notice.

Summary

To ensure this article ranks for “Best Auto Loan Companies” and “How to switch auto loan companies,” we have focused on:

- Direct Answers: Providing clear, list-based answers for voice search and AI summary tools.

- Technical Specifics: Detailing bureau usage (TransUnion, Equifax, Experian) which is a high-intent long-tail search query.

- E-E-A-T: Emphasizing Experience, Expertise, Authoritativeness, and Trustworthiness by detailing specific bank programs like BofA’s Preferred Rewards or LightStream’s Rate Beat.

Key Takeaways for Borrowers:

- Best Overall: LightStream or PenFed.

- Best for Transparency: Capital One Auto Navigator.

- Switching Method: Refinancing via a new lender to pay off the old balance.

- Bureau Tip: Check your reports at AnnualCreditReport.com before applying to see which of your scores is highest.

By understanding the interplay between credit bureaus and lender preferences, you can strategically apply for a loan that fits your financial profile, ensuring you get the best possible deal in the 2025 market.

Frequently Asked Questions

To help you navigate the complexities of vehicle financing, we have compiled the top 10 questions asked by borrowers today. These answers are optimized to provide direct, concise information for search engine snippets.

1. What is the minimum credit score needed for an auto loan?

Most lenders prefer a credit score of at least 660 for standard rates. However, “subprime” lenders offer loans to those with scores as low as 500. Borrowers with scores above 740 (Super-prime) typically qualify for the lowest advertised interest rates.

2. Can I get an auto loan with no down payment?

Yes, many lenders offer 0% down financing to borrowers with “Good” to “Excellent” credit (700+). However, making a down payment of at least 10–20% is recommended to avoid “gap” issues, where you owe more than the car is worth if it is totaled or stolen.

3. Does refinancing an auto loan hurt your credit score?

Initially, your score may drop by a few points due to a hard inquiry and the closing of an old account. However, if you make consistent on-time payments on the new loan, your score typically recovers and improves within a few months due to a healthier debt-to-income ratio.

4. How soon can I refinance my car loan after buying it?

Technically, you can refinance as soon as the title is processed and the current loan is established (usually 30 to 90 days). To see the biggest benefit, most experts suggest waiting 6 to 12 months to prove a consistent payment history.

5. What is the difference between a direct and indirect auto loan?

- Direct Lending: You get a loan directly from a bank, credit union, or online lender before you go to the dealer.

- Indirect Lending: The dealership handles the financing through their partner networks. Dealerships often add a “markup” to the interest rate, making direct lending generally cheaper.

6. Which credit bureau do most auto lenders pull from?

While it varies by region, Experian is the most commonly used bureau for auto lending in the U.S., followed by Equifax and TransUnion. Many lenders also use the FICO Auto Score 8 or 9, which is a version of your credit score weighted specifically for car payment history.

7. Can I refinance my car loan with the same bank?

Most banks do not allow you to refinance an existing loan they already hold. To get a lower rate, you typically must switch to a different financial institution. This is to prevent banks from losing interest revenue on an existing contract.

8. What is a “Simple Interest” auto loan?

Most modern auto loans use simple interest, where interest is calculated daily based on the remaining principal balance. This benefit allows you to save money on interest by making extra payments or paying the loan off early, as there are usually no pre-payment penalties.

9. How long can you finance a car in 2025?

Loan terms currently range from 24 to 96 months. While 72-month and 84-month loans are becoming more common to keep monthly payments low, they often result in paying significantly more in total interest. The “sweet spot” for most buyers is 48 to 60 months.

10. Does a car’s age affect the interest rate?

Yes. Generally, new cars have lower interest rates than used cars. Lenders view newer vehicles as lower risk because they have higher resale values and are less likely to have mechanical failures that could lead to the borrower defaulting on the loan.